Investor's Corner

Tesla (TSLA) releases Q3 2023 delivery and production results: 435k delivered and 430k produced

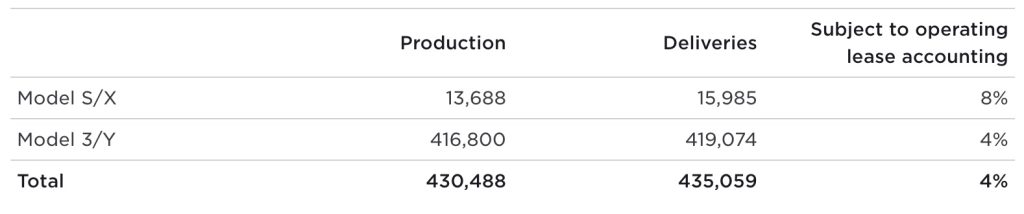

Tesla (NASDAQ:TSLA) has released its Q3 2023 delivery and production report. As per the electric vehicle maker, it was able to deliver 435,059 and produce 430,488 vehicles in the third quarter.

Specifically, Tesla delivered a total of 419,074 Model 3 and Model Y and 15,985 Model S and Model X in Q3 2023. Production-wise, Tesla produced 416,800 Model 3 and Model Y and 13,688 Model S and Model X during the quarter.

Despite falling short of the Street’s expectations, Tesla maintained that it remains on track to hit 1.8 million vehicles in 2023.

“In the third quarter, we produced over 430,000 vehicles and delivered over 435,000 vehicles. A sequential decline in volumes was caused by planned downtimes for factory upgrades, as discussed on the most recent earnings call. Our 2023 volume target of around 1.8 million vehicles remains unchanged,” the company wrote.

With these results, Tesla has now delivered 1,324,074 cars in the first three quarters of 2023. This number already exceeds the company’s 2022 results, which totaled 1,313,851 vehicles.

Tesla reports production of 430,488 and deliveries of 435,059 for 23Q3. The decline in deliveries is -7% QoQ and growth of 27% YoY. The Tesla fleet reaches 5m cars. $TSLA

Tesla reached whole 2022 sales within 3 quarters. pic.twitter.com/XZ8PsGqVfm— Roland Pircher (@piloly) October 2, 2023

Tesla’s Investor Relations team has shared a compiled analyst consensus for the company’s Q3 2023 vehicle deliveries. Tesla’s IR-compiled analyst consensus stood at 455,000 vehicles, which was very optimistic considering that Tesla’s production in Q3 was slowed down by Giga Shanghai’s transition to the Model 3 Highland, which was launched in the third quarter.

Tesla’s IR-compiled delivery consensus was comprised of estimates from Baird, Barclays, Bernstein, Bank of America, Canaccord, Citibank, Cowen, Daiwa, Deutsche Bank, Evercore ISI, Exane BNP, Goldman Sachs, Guggenheim, Jefferies, Mizuho, Morgan Stanley, New Street Research, Oppenheimer, Piper Sandler, RBC, Truist, Tudor, UBS, Wedbush, and Wolfe.

$TSLA IR-compiled 3Q consensus is for 455K deliveries. This compares to Bloomberg’s 3Q consensus of 457K. My 3Q est is 445K. We continue to expect investors to overlook any reasonable miss (445K-455K) given the well-documented M-3 Highland transition (likely cost 15K-20K) and… pic.twitter.com/RJsqPCruq0— Gary Black (@garyblack00) September 29, 2023

During the Q2 2023 earnings call, Elon Musk also spoke of factory upgrades that would affect vehicle production in the third quarter. “We continue to target 1.8 million vehicle deliveries this year, although we expect that Q3 production will be a little bit down because we’ve got some shutdowns to for — a lot of factory upgrades. So, just probably a slight decrease in production in Q3 for sort of global factory upgrades,” Musk said.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Elon Musk

California snubs Tesla in its newly passed EV incentive that favors Rivian and Lucid

California passed a $135 million EV incentive that rewards Rivian and Lucid while sidelining Tesla

California just drew a line in the EV incentive sand to put Tesla on the wrong side of it. The state recently passed a $135 million program offering first-time electric vehicle buyers a direct incentive with no application required, but the rules were written in a way that leaves Tesla at a structural disadvantage compared to Rivian and Lucid.

The program caps eligible vehicles at $50,000 for new EVs and $25,000 for used ones. That pricing threshold rules out a significant portion of Tesla’s lineup, though some lower-priced Model 3 and Model Y configurations would still qualify. California-based automakers are exempt from the price cap entirely, regardless of what their vehicles cost. Rivian, headquartered in Irvine, and Lucid, based in the San Francisco Bay Area, both benefit from that exemption. Rivian’s R2 starts at roughly $45,000 but has versions above the cap. Lucid’s Air and Gravity start at $70,990 and $79,990 respectively, well above any threshold a non-California company would face.

California hits Tesla Cybercab and Robotaxi driverless cars with new law

Tesla built its reputation and a significant portion of its early market share in California, where EV adoption has consistently led the nation. The company operates its original factory in Fremont, California, and the state was home to Tesla’s headquarters for most of its existence. That changed in 2021 when Tesla moved its corporate headquarters to Austin, Texas. Since then, the relationship between the company and California Governor Gavin Newsom has been openly adversarial, with Musk and Newsom trading public criticism on multiple occasions.

California’s EV incentive landscape has shifted repeatedly in recent years, and Tesla has previously lost eligibility for state-level programs as its vehicles exceeded income-adjusted price thresholds. The federal $7,500 EV tax credit, which Tesla models have qualified for and lost depending on policy cycles, is no longer available after it expired without renewal, making state-level programs more meaningful to buyers than they have been in years.

The practical impact for buyers is more nuanced than the headline suggests. California residents purchasing a Tesla under $50,000 for the first time can still access the incentive. But the exemption written for California-based manufacturers is a structural advantage that rewards where a company plants its headquarters flag rather than where it builds its products, and Tesla moved that flag to Texas.

Elon Musk

SpaceX’s newest logo confirms everything about what it’s become

SpaceX officially absorbed xAI under the SpaceXAI brand, completing the largest private merger in history.

SpaceX made its corporate transformation official in May 2026 when Elon Musk posted on X that xAI would cease to exist as a standalone company. “xAI will be dissolved as a separate company, so it will just be SpaceXAI, the AI products from SpaceX,” he wrote.

A new SpaceXAI logo was announced today, visually embedding the xAI letters inside the SpaceX identity, which can be seen as a deliberate design choice that signals the merger is not a partnership but a full absorption and XAi a core function of the same company. The same way Starlink is not a separate brand but a SpaceX product. The announcement closed the loop on a process that began February 2, 2026, when SpaceX acquired xAI in the largest private merger in history, valued at $1.25 trillion. SpaceX at $1 trillion and xAI at $250 billion.

We are now @SpaceXAI. pic.twitter.com/ema66xDWC9

— SpaceXAI (@SpaceXAI) July 6, 2026

The reason SpaceX bought xAI was stated plainly by Musk at the time of the deal: to build orbital data centers. SpaceX had simultaneously filed with the FCC to launch up to one million satellites designed to function as AI compute nodes in low Earth orbit, escaping what Musk described as the energy constraints limiting AI development on Earth.

xAI provided the AI software stack, with Grok, the X platform, and the Colossus supercomputer infrastructure in Memphis with over 220,000 NVIDIA GPUs, while SpaceX provided the rockets, Starlink, and the capital base to fund it. The two companies needed each other. xAI was burning $2.5 billion in losses on $250 million in revenue. SpaceX was generating an estimated $8 billion in profit on $15 billion in revenue and needed an AI narrative to command the valuation it was targeting for its IPO.

What SpaceX has done, regardless of how the orbital AI vision ultimately plays out, is walk into a public market as something no company has been before: a rocket manufacturer, satellite internet provider, AI software company, social media platform, and supercomputer operator under one ticker. Whether that combination is worth $2 trillion depends entirely on which of those businesses you believe in most.

Investor's Corner

Tesla challenges startups to score a gig inside its most advanced European factory

Tesla is challenging startups to bring their best battery tech directly to Gigafactory Berlin.

Tesla has issued an open challenge to startups across Europe, inviting them to bring their best battery technology directly to the floor of Gigafactory Berlin. The program, called the JUNI x Tesla Battery Cell Giga Challenge, opened applications this month with a deadline of July 24, 2026, and is targeting startups with solutions that can make battery cell manufacturing faster, cheaper, safer, and more scalable at an industrial level.

The timing of the challenge is directly tied to Tesla’s most aggressive European battery investment yet. On May 12, 2026, Giga Berlin plant manager André Thierig announced a $250 million investment to scale the factory’s annual 4680 cell production capacity from 8 GWh to 18 GWh, more than doubling the previous target set just months earlier in December 2025. Thierig confirmed the expansion on X, saying the investment “will enable 18 GWh of annual 4680 cell production and create more than 1,500 new jobs.” Combined with a previously announced battery investment at the Grunheide site now approaches $1.2 billion.

Today, we announced a $ 250m investment for our Giga Berlin Cell factory. This will enable 18GWh of annual 4680 cell production and create more than 1500 new jobs. Good news during challenging times for the German industry. pic.twitter.com/ou4SWMfWh9

— André Thierig (@AndrThie) May 12, 2026

The challenge is looking specifically for startups with proven solutions across five categories: materials, equipment, operations, automation, and artificial intelligence. Applications are screened directly by Tesla’s cell manufacturing team in Grunheide, and the strongest submissions move through technical discussions, a pitch day in front of Tesla stakeholders, and potentially a paid pilot project with the cell team. Tesla is not looking for ideas at concept stage. The program requires applicants to demonstrate working prototypes, test data, or prior pilots before being considered.

The historical context matters here. Elon Musk first announced plans for what he called the world’s largest battery cell production facility alongside the Giga Berlin car factory back in 2020, targeting up to 250 GWh of annual capacity. Those plans were shelved in 2022 when Tesla shifted its battery investment focus to the United States to take advantage of Inflation Reduction Act incentives. The revival of cell production at Giga Berlin, now backed by over $1 billion in committed capital, represents a return to an ambition that was set aside for three years. As Teslarati has reported, the 4680 format is central to Tesla’s long-term cost reduction strategy across vehicles, energy storage, including the Tesla Semi and Cybercab.

By opening the challenge to outside startups, Tesla is acknowledging that reaching 18 GWh at Grunheide will require technology it does not currently have in-house, and it is willing to pay for the right solutions. For a startup in the battery supply chain, a paid pilot with Tesla’s European cell team is as close to a direct commercial path as the industry offers.

Tesla FSD is about to know your specific house and neighborhood better than any map

The secret behind Tesla’s Cybercab Gold goes well beyond just the color