Investor's Corner

Tesla (TSLA) stock listed as May’s most-shorted large-cap stock by Hazeltree

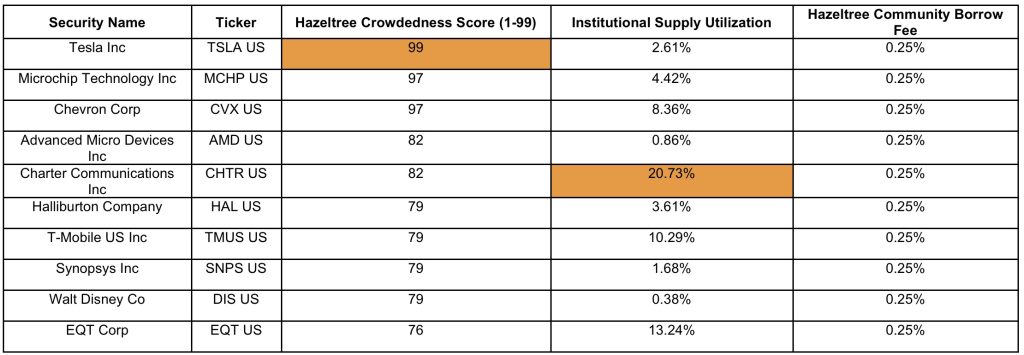

Tesla has been listed by data and tech firm Hazeltree as the most-shorted large-cap stock in the United States in May 2024. As per the data firm, Tesla has a grade of 99 on its Hazeltree Crowdedness Score. The firm outlined its findings in its May 2024 Hazeltree Shortside Crowdedness Report.

Hazeltree’s Crowdedness Score represents securities that are being shorted by the highest percentage of funds in the firm’s community in a pre-defined category. The securities are graded on a scale of 1-99, with 99 representing the security that the highest percentage of funds are shorting. As of May 2024, TSLA shares are at the top of Hazeltree’s list.

Hazeltree describes the source of its data as follows: “The data sourced in this report comes from Hazeltree’s proprietary securities finance platform data, which tracks approximately 15,000 global equities across the Americas, EMEA, and APAC. The data is aggregated and anonymized from the contributing Hazeltree community, which includes approximately 700 asset manager funds.”

Following Tesla in the list of the US’ most shorted large-cap securities are Microchip Technology Inc., which has a crowdedness score of 97; Chevron Corp., which has a crowdedness score of 97; Advanced Micro Devices Inc. (AMD), which has a crowdedness score of 82; and Charter Communications Inc., which has a crowdedness score of 82.

Tesla shares are currently facing headwinds amidst the impending 2024 Annual Stockholders’ Meeting on June 13, 2024. Tesla investors are poised to vote on several proposals at the upcoming event, the most notable of which are the ratification of Elon Musk’s 2018 CEO Performance Award and the proposed redomestication of Tesla from Delaware to Texas. Tesla currently trades at $169.32 per share as of writing, giving the EV maker a market cap of $539 billion.

The May 2024 Hazeltree Shortside Crowdedness Report can be viewed below.

Hazeltree May Shortside Report_Final by Simon Alvarez on Scribd

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Elon Musk

SpaceX’s newest Starmind will make earth data centers obsolete

Elon Musk confirmed Starmind as SpaceX’s AI satellite constellation name, targeting one million orbital compute nodes.

Elon Musk confirmed that Starmind will be the official name of SpaceX’s planned AI satellite constellation, following a trademark filing by xAI that surfaced earlier this week. Starmind is what’s being described to the FCC as a constellation of up to one million AI satellites

It’s worth noting that SpaceX’s Starlink communication satellite and Starmind are built on the same orbital infrastructure concept but serve entirely different purposes. Starlink is a connectivity network, with satellites receiving and relaying data between points on Earth, and functioning as a high-speed internet backbone in space. The satellites themselves do not process or think, and move information from one place to another, the same function a fiber cable performs underground.

SpaceX just forced Verizon, AT&T and T-Mobile to team up for the first time in history

Starmind, on the other hand, is something completely different, and tather than moving data, its satellites would compute data through artificial intelligence and directly in orbit using onboard processors powered by large solar arrays. Where a Starlink satellite is essentially a very fast pipe, a Starmind satellite is a server. The practical implication is that Starmind would allow AI models to run inference, process queries, and generate outputs from space, then beam results down to users anywhere on Earth within milliseconds, and without the data ever needing to travel to a terrestrial data center.

Starship will be able to carry 30 to 50 AI1 satellites per launch, delivering the equivalent of dozens of server racks per flight, with no land acquisition, no power grid approval, and no cooling infrastructure required on the ground.

SpaceX is pursuing this new technology as terrestrial data centers are running into hard limits such as lack of physical space, community opposition, and power and water consumption at a scale that is increasingly difficult to permit. Space has unlimited solar power, natural vacuum cooling, and no zoning boards. Musk said in a June 8 video presentation that he expects space to become the lowest-cost location to deploy AI compute within two to three years. Two AI1 prototypes are scheduled to launch in early 2027, with volume production targeted for the end of that year at a new facility called Gigasat.

The real world applications Starmind enables extend well beyond powering Grok. A constellation of orbiting AI processors could run inference workloads for any paying customer, anywhere on Earth, with latency measured in milliseconds rather than the seconds associated with ground-based cloud routing across continents. Starmind, if it scales as described, would make SpaceX the landlord of AI compute the same way Starlink made it the landlord of satellite internet.

SpaceX announced today that it commenced its first-ever public bond offering, marking a significant step in the newly public company’s capital markets strategy.

The company announced an offering of senior unsecured notes expected to raise at least $20 billion.

The move comes just a short time after SpaceX completed one of the largest initial public offerings in history. In mid-June, the company priced shares at $135 and raised more than $85 billion, propelling founder Elon Musk’s net worth past the trillion-dollar mark and giving the firm substantial liquidity.

🚨 SpaceX has announced its inaugural offering of senior unsecured notes.

The net proceeds will be used to repay outstanding loans under its bridge loan facility in full.

This inaugural debt offering represents a financing milestone for SpaceX, which previously depended… pic.twitter.com/pcOZuVbTRv

— TESLARATI (@Teslarati) June 22, 2026

According to the company’s SEC filing, the net proceeds from the notes will be used primarily to repay in full the outstanding borrowings under its existing bridge loan facility, cover related fees and expenses, and fund general corporate purposes. The offering is being conducted under Rule 144A, as well as Regulation S, targeting qualified institutional buyers and non-U.S. investors. Notes will be unsecured obligations ranking equally with other unsubordinated debt.

The $20 billion bridge loan was used to refinance approximately $17.5 billion in higher-cost “junk” debt tied to X and xAI. SpaceX had merged with xAI in February 2026 in an all-stock deal. The bridge facility, which matures in September 2027, had represented the bulk of SpaceX’s long-term debt.

SpaceX officially acquires xAI, merging rockets with AI expertise

In connection with the bond launch, SpaceX disclosed it held approximately $100.8 billion in cash and cash equivalents as of June 19. Investor calls began on the announcement date, with pricing and launch expected shortly thereafter. Rating agencies have assigned investment-grade ratings to the proposed bonds, reflecting confidence in SpaceX’s dominant position in commercial launches and the growth trajectory of its Starlink internet offering.

The debt raise also allows SpaceX to optimize its balance sheet by replacing short-term, higher-cost bridge financing with longer-date, lower-cost fixed-income securities. This provides greater financial flexibility to support capital-intensive initiatives, including the development of Starship, the expansion of the Starlink constellation, and the integration of AI capabilities following the xAI combination.

SpaceX shares (NASDAQ: SPCX) fell sharply on the news, dropping over 16 percent overall on the market on Monday. The stock had surged initially after debuting but pulled back amid profit-taking and broader market dynamics.

Overall, the bond offering underscores SpaceX’s transition to a mature public company with access to diverse funding sources. It positions the firm to pursue its long-term vision of multiplanetary expansion and AI infrastructure, while maintaining a disciplined approach to its capital structure in a high-growth but capital-heavy industry.

Investor's Corner

SpaceX is launching a secret spacecraft that could change how things are made in space

SpaceX’s secret disk-shaped Starfall capsule is targeting a market no reentry vehicle has cracked.

SpaceX is targeting Tuesday, June 23 for the first flight of Starfall, a reentry capsule the company has developed almost entirely in private. The Falcon 9 launch window opens at 6:43 a.m. ET from Space Launch Complex 40 at Cape Canaveral Space Force Station, with a backup window available the same time on June 24. SpaceX has made no public announcement about the vehicle, only providing launch details. Everything known about it has come through FAA and FCC regulatory filings.

What makes Starfall different starts with its shape. Rather than the traditional cone used by Dragon and every other cargo return capsule in operation, Starfall is a flat disk that measures roughly 10.2 feet (3.1 meters) wide and just 2.5 feet (0.75 meters) tall, and weighing 4,630 pounds (2,100 kg) and capable of returning up to 2,200 pounds (1,000 kilograms) of payload from orbit. The disk geometry maximizes structural efficiency and payload volume relative to mass, and the heat shield mechanically jettisons just before splashdown, allowing recovery teams to retrieve both the capsule and the shield separately from the Pacific Ocean.

The difference with Starfall from existing competitors, such as Varda Space Industries, which has largely built the orbital manufacturing market and returns heavy payloads per flight is that Starfall’s specification is roughly 30 times more per mission, and is designed to be mass-produced and launched on either Falcon 9 or Starship. That combination of volume and launch access is something no standalone startup can replicate, and it puts SpaceX in direct competition with the companies that currently pay it to reach orbit.

SpaceX to launch military missile tracking satellites through new Space Force contract

The intended market is orbital manufacturing: pharmaceuticals, protein crystals, semiconductors, and advanced optical fiber that physically cannot be produced in the presence of gravity. FAA documents describe Starfall’s long-term purpose as building a “self-sustaining commercial in-space manufacturing market” and as a potential successor to the industrial capabilities of the International Space Station, which is set to retire in the late 2020s. Military rapid global cargo delivery is a parallel application under active discussion with the Pentagon.

The reason some industries seek manufacturing in space comes down to gravity. On Earth, gravity causes materials to settle, separate, and deform during production. In microgravity, those constraints disappear.

SpaceX’s already controls launch access, which means it currently functions as the landlord for every competitor in the orbital manufacturing return space. Starfall converts that landlord position into vertical ownership, and it would no longer just carry other companies’ capsules to orbit, but rather operate the capsule, own the return logistics, and capture the service revenue directly. Viewed alongside Starlink, Colossus, and the xAI merger, Starfall fits a consistent pattern: SpaceX identifying infrastructure layers that others depend on and moving to own them outright. Orbital manufacturing return is the next layer on that list.

If Tuesday’s reentry, parachute sequence, and recovery demonstration goes as planned, the second FAA-approved test flight follows. A successful pair of demos would position SpaceX to begin offering Starfall as a commercial service, likely first to pharmaceutical and materials science customers before scaling toward the military and broader manufacturing segments.

Tesla Q2 delivery consensus confirms this long-standing theory

Tesla looks keen to bring larger Model Y L to the U.S.