Investor's Corner

What to look for in Tesla Motors Q1 Financials

Tesla (NASDAQ: TSLA) is set to announce its first quarter earnings report after market close on Wednesday, May 4, 2016.

TSLA reported 4th quarter 2015 earnings of $ -0.87 per share on February 10, 2016. This missed the consensus of $ 0.10 by $ -0.97 of the 16 analysts covering this company. Interestingly that turned out to be the end of a dramatic 42% slide which began on January 1st. Since then TSLA has moved from its lowest point of $141 on that day to roughly $250 per share, a 78% increase in just 3 months. That kind of tells you that TSLA is a stock not for the faint of heart.

Source: WallSt I/O

The consensus of the 14 analysts covering TSLA for 1st quarter 2016 is a per share loss of $ -.57, with range estimates of: 0.080 | -0.569 | -1.000 (High | Mean | Low).

")

$TSLA earnings summary via E-Trade

Based on 20 analysts offering 12-month targets from TSLA, the average price target is $243.95, effectively a zero-move from the current stock price. If you are an “investor” in TSLA stock, the pros tell you that TSLA will not go anywhere in the next 12 months.

$TSLA analysis via TipRanks

So those are the numbers from the pros, but if you still decide that you want to trade TSLA stock, what should you be looking for in the quarterly results and the conference call webcast?

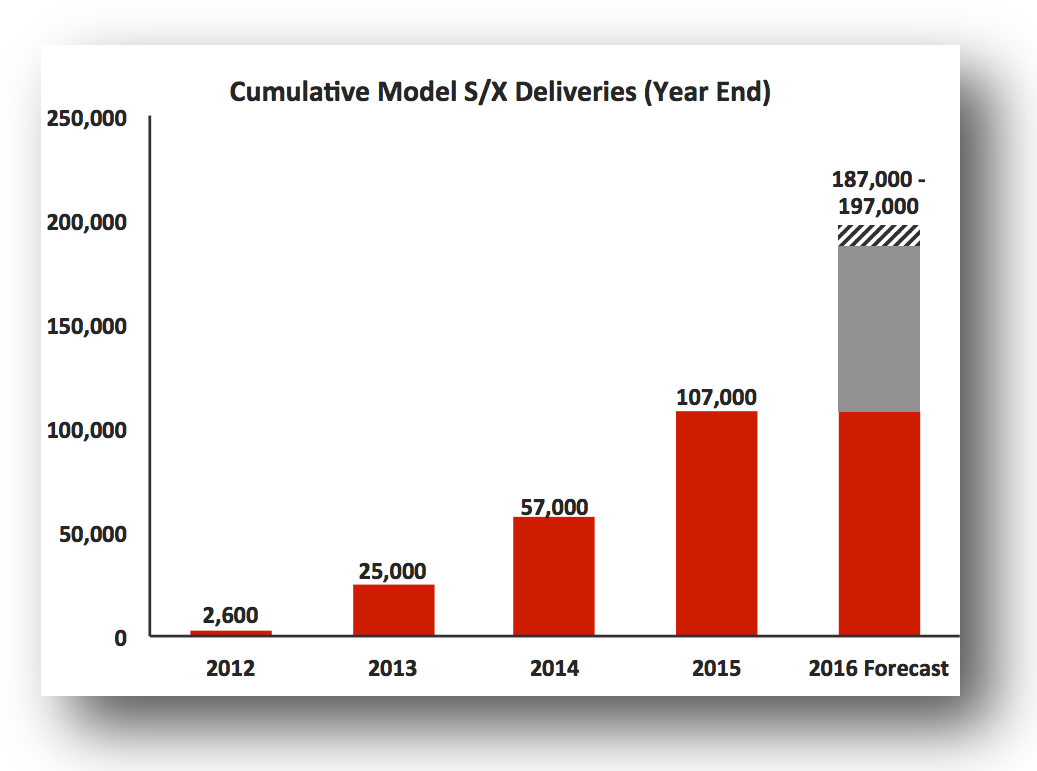

Q1 Vehicle Deliveries

Let’s take a look at a few items from the “Tesla 4th Quarter & Full year 2015 Shareholder Letter”.

In the “Q1 and Full Year 2016 Outlook” section, Tesla states that “we plan to deliver 80,000 to 90,000 new Model S and Model X vehicles in 2016. […] In Q1, we plan to grow deliveries 60% year on year to approximately 16,000 vehicles”.

Source: Tesla Motors

We already know that Q1 deliveries did not meet the promised 16,000 units, as that number was actually 14,820, due to “severe Model X supplier parts shortages in January and February” as provided in a Press Release on April 4, 2016. In the same release, “Tesla reaffirms its full-year delivery guidance [of 80,000 to 90,000 vehicles].”

The missing income due to the delayed Model X vehicles delivery will be partially offset by the initial Model 3 “reservations”. It is quite interesting that reservations opened on March 31, 2016, the last day in the quarter, and at least 125,000 of them may be counted as an additional $125M income in Q1. In the end, guidance on vehicle deliveries for Q2 2016 will be one of the deciding factors on where TSLA stock moves post the Q1 report.

Cash Flow and Margins

In the same Q4 Shareholder Letter, Tesla states that “we expect to generate positive net cash flow and achieve non-GAAP profitability for the full-year 2016”, and “we plan to fund about $1.5 billion in capital expenditures without accessing any outside capital.” These are both very aggressive goals, especially in light of the 400,000+ Model 3 reservations, as of the latest disclosed counts. Elon Musk has already tweeted that he is “definitely going to need to rethink production plans”, which likely means that another factory will be needed to produce the Model 3 in a reasonable timeline that will allow delivery to the majority of the current reservation holders. This more aggressive delivery of Model 3 vehicles as originally envisioned will likely require outside capital for building such factory.

Definitely going to need to rethink production planning…

— Elon Musk (@elonmusk) April 1, 2016

Since missing the mark on Model X will impact cash flow for Q1, I would expect questions in the conference call asking if the issues have been resolved, and if the missing Model X numbers can be made up in Q2. While cash flow reversed action to the positive for the first time during Q4 2015, with a strong $179M cash flow from core operations, Tesla needs to prove that this behavior will continue in 2016.

Again in the Q1 Shareholder Letter, Tesla states that “Throughout the rest of 2016, Automotive gross margins should continue to increase. […] Model S gross margins should begin to approach 30% and Model X gross margins should be about 25%.” In Q4 gross margins were 20.9% for the Tesla Model S and even a slight increase in margins will be viewed positively by the market. This is a number that will be greatly watched as Tesla needs to prove that it can eventually deliver 500K+ vehicles / year at a profit. Much of the current valuation of Tesla stock is built on this assumption. Accordingly, a drop in margins for Q1 would be viewed very negatively by the market, at least for the short term.

Summarizing, besides vehicle delivery, cash flow and margins will be the other two drivers of the TSLA stock short-term market action after the Q1 report numbers are released.

Live Q&A Webcast

Tesla management will hold a live question & answer webcast on May 4 at 2:30pm Pacific Time to discuss the Company’s financial and business results and outlook. Live and replay webcast will be available at http://ir.teslamotors.com/eventdetail.cfm?EventID=171952 .

Tip of the Week

Starting with today’s posting I’ll be including a “tip of the week.” This may involve covering a trading concept, or recommending a website with tools or information useful to investors and traders of TSLA.

For this week, I am recommending signing up for the free Basic Membership of TipRanks. With it you can receive free alerts for 1 stock and 1 expert, which is enough for the ones just interested in TSLA stock. Happy trading.

Disclosure: I currently have no positions in any stocks mentioned, but I may plan to initiate positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Teslarati). I have no business relationship with any company whose stock is mentioned in this article.

Elon Musk

SpaceX Starship just nailed something it’s never done before

SpaceX’s Starship flew successfully Friday, landing both stages and deploying its first Starlink V3 satellites.

Starship’s thirteenth test flight delivered exactly what SpaceX needed with a clean liftoff, two successful stage recoveries, and the first real payload the vehicle has ever carried to space. Booster 20 and Ship 40 lifted off at 5:51 p.m. CT from Starbase, and by the time the mission wrapped roughly an hour later, both halves of the rocket had done exactly what they were supposed to do.

Booster 20 separated from Ship 40 a few minutes into the flight and stuck a controlled splashdown in the Gulf of Mexico about six minutes after liftoff. That is a meaningful turnaround from Flight 12 in May, when the booster lost several engines during its boostback burn before a hard water landing attempt.

Starship as seen from Starlink satellites pic.twitter.com/e2hvfmnewh

— Elon Musk (@elonmusk) July 25, 2026

Starship 40’s performance was arguably the bigger win. The vehicle deployed the first 20 operational Starlink V3 satellites Starship has ever carried, then flew a suborbital arc to a landing in the Indian Ocean that SpaceX commentator Dan Huot called the company’s softest splashdown yet. “This is a dream scenario for this team that’s trying to get this heat shield data,” Huot said on the live broadcast, according to Space.com’s live coverage. “I’m a little over the moon right now. Wow. Lucky number 13.”

Unlike the mass simulators SpaceX flew on Flight 12, these were production Starlink V3 satellites, meant to extend solar arrays and antennas and attempt to link with the broader constellation before reentering minutes later. Getting real hardware through a full deploy sequence on only the second flight of the V3 generation keeps Starship on schedule for the payload work NASA is counting on for future Artemis lunar landings.

What an awesome launch, really seems like everything went super well and it was all incredibly smooth.

SpaceX is awesome. Very interested to see how the market will respond on Monday pic.twitter.com/KSHmyBfV55

— TESLARATI (@Teslarati) July 25, 2026

— TESLARATI (@Teslarati) July 25, 2026

The flight also arrives at a moment when SpaceX needed a win. SPCX has traded below its $135 IPO price since mid-July, as Teslarati reported when the mission slipped to Friday, and short interest has climbed to roughly a third of the tradable float. A clean flight will not fix a balance sheet, but it does answer the one question SpaceX absolutely needed answered this week: whether the fixes made after the July 16 abort would hold up under real flight conditions. They did, on both stages, on the first try after the redesign.

SpaceX has not set a target date for Flight 14, though the company has said it wants to push toward an orbital attempt on the next mission. After Friday, that goal looks a lot more within reach.

Tesla short sellers won big following the company’s massive fall on Wall Street after it reported subpar Earnings on Wednesday.

Tesla short sellers collected about $4.12 billion in single-day profits on Thursday, according to Bloomberg. Shares fell as much as 15 percent during Thursday’s session. It closed as one of the worst days for Tesla on Wall Street in the past three years.

Investors sold off the stock after Tesla said it would aggressively direct its spending toward AI and its Optimus robot project. The company had record revenues, which were driven by one of the strongest quarters in terms of vehicle deliveries in company history.

However, it missed EPS estimates by reporting just $0.33, a far cry from the $0.53 analysts expected.

S3 Partners reported that about 3 percent of Tesla’s outstanding stock is sold short. Managing Director at S3, Ihor Dusaniwsky, provided the short seller’s potential profit, as well as another figure: shorts have likely had paper gains of $8.92 billion this year, as Tesla shares are down 30 percent in 2026.

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Tesla has burned short sellers many times in the past, but the company’s latest Earnings Call was a chance for those skeptics to taste some payback. Although the company gave some very transparent information regarding future projects, the rollout of Robotaxi, Optimus, and Semi, many investors took their profits on Thursday.

Notable short sellers like Michael Burry have been transparent about their skepticism around Tesla shares. Burry just revealed three weeks ago that he had opened up a new short on the stock, stating he shorted Tesla shares at $416.22. “Happy it jumped back to this level,” he said in a blog post.

At the time of publication, Tesla shares were down about 3 percent and the stock was trading at $309.92.

Tesla stock (NASDAQ: TSLA) endured one of its sharpest single-day declines in years on July 23, tumbling approximately 14.5 percent and closing near $320 after opening the session around $374. The drop erased more than $140 billion in market value amid heavy trading volume and left the shares at multi-week lows.

The sell-off followed the company’s second-quarter 2026 results, released the previous evening. Tesla reported record revenue of $28.2 billion, up 26 percent year over year, driven by a Q2-record 480,126 vehicle deliveries. Energy storage deployments also rose strongly.

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Yet profitability disappointed sharply. Operating income fell 57 percent to $398 million, compressing the operating margin to just 1.4 percent. Non-GAAP earnings per share came in at $0.33, well below the roughly $0.53 analysts had expected. Free cash flow turned negative by $1.1 billion as capital expenditures surged 142 percent to $5.8 billion, largely tied to accelerated spending on artificial intelligence, robotics, and autonomous systems.

The losses on capex were expected, as Tesla said it would be spending heavily in 2026.

Investors also reacted to lingering uncertainty surrounding key product timelines. During the Earnings Call, management reiterated ambitions for Robotaxi deployment and the Optimus humanoid robot, but offered limited new concrete milestones, renewing questions about execution pace that have long accompanied Tesla’s ambitious roadmap.

The magnitude of the decline places it among Tesla’s more severe one-day percentage losses since its 2010 initial public offering. Historically, the two largest single-day drops (split-adjusted) remain September 8, 2020, when shares fell 21.1 percent amid broader market volatility and valuation concerns, and January 13, 2012, with a 19.3 percent plunge during the company’s early growth struggles.

Other notable declines include an 18.6 percent drop on March 16, 2020, at the onset of pandemic-related market turmoil. Thursday’s move ranks roughly ninth on the all-time list but stands out as the steepest in more than a year.

Despite the short-term pain, Tesla’s long-term trajectory has repeatedly recovered from such volatility. The latest results underscore both the strength of its core automotive and energy businesses and the near-term costs of heavy investment in next-generation technologies.

Tesla flexes incredible Robotaxi metric that skeptics will hate

SpaceX Starship just nailed something it’s never done before