Investor's Corner

Wall Street thinks Tesla ($TSLA) is headed into bear territory

In advance of tomorrow’s Q4 earnings call, Tesla investors and Wall Street analysts have seldom held more conflicting views about where the stock is heading. Shares in Tesla have advanced 50% in the past 3 months, setting historic highs along the way. Based on market capitalization, Tesla is now worth just slightly less than auto manufacturers Ford and General Motors.

Some analyst think the stock will go higher still. Morgan Stanley’s Adam Jonas forecasts a price of $305 per share in the near future but many of his colleagues disagree. Bloomberg recently polled 14 analysts and found the majority of them see the stock going lower in the months ahead. The median response was $48 per share below where the stock is today. That is the most pessimistic view among Wall Street traders since Tesla went public 7 years ago and is reflected in Bloomberg’s chart below.

Of the six analysts who have updated their advice on Tesla in the month of February, none has raised the estimate. That is despite the company announcing that it would begin pilot production of the Model 3 this week, news that has been one of the triggers for the latest run up. We “see no fundamental reason for run-up,” said UBS Securities LLC analyst Colin Langan. He sent a note to his clients last week in which he projected the price of Tesla stock to fall back to$160 a share over the next 12 months.

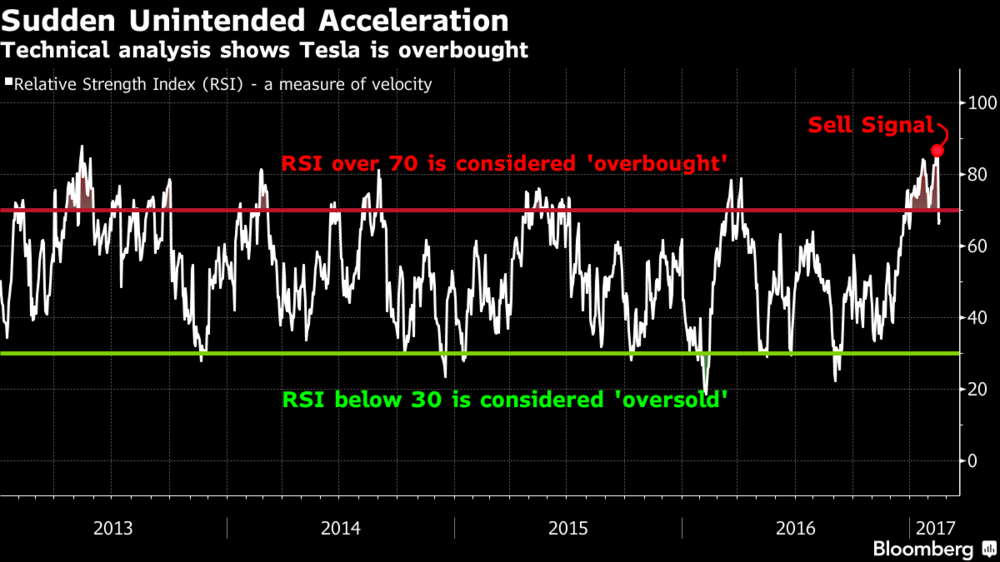

Why the disconnect? Traditionally, market watchers pay attention to something they call the Relative Strength Index, which measures the speed and change of a stock price either up or down. In essence, it is is a tool designed to strip out the emotional component that affects all stock valuations and insulate professionals from getting caught up in the herd mentality.

If the RSI climbs above 70, that indicates a stock is “overbought.” Such a level is widely considered to be a “sell signal.” Conversely, anything below 30 is considered “oversold” and is considered a “buy signal.” Tesla’s RSI soared to 83 last week, the highest level in more than 4 years.

Tesla has a lot on its plate this year. In addition to getting the Model 3 into regular production, it is aggressively pursuing its grid scale battery storage business, expanding the Gigafactory, completing the integration of SolarCity into the business, rolling out its new Solar Roof product line, continuing the expansion of its Supercharger network, opening new stores, and building new service centers. It is also pushing into new markets in Portugal, Dubai, Taiwan, India, and Korea.

In the spring of 2016, Elon Musk predicted Tesla would have a market capitalization equal to Apple by the year 2025, or somewhere around $700 billion. Musk has never been shy about touting his projections for the future and many investors take his pronouncements as articles of faith. They see stock analysts as Luddites who just don’t “get it” when it comes to Musk and Tesla.

-

-

“Tesla is a serial capital raiser,” says Adam Jonas. “As such, its ability to sustain its operations and fundamental value is inextricably linked to the very performance of its share price, creating a self-reinforcing momentum.” Whether that “self-reinforcing momentum” will continue to propel Tesla’s stock price higher is anybody’s guess.

Elon Musk

SpaceX Starship just nailed something it’s never done before

SpaceX’s Starship flew successfully Friday, landing both stages and deploying its first Starlink V3 satellites.

Starship’s thirteenth test flight delivered exactly what SpaceX needed with a clean liftoff, two successful stage recoveries, and the first real payload the vehicle has ever carried to space. Booster 20 and Ship 40 lifted off at 5:51 p.m. CT from Starbase, and by the time the mission wrapped roughly an hour later, both halves of the rocket had done exactly what they were supposed to do.

Booster 20 separated from Ship 40 a few minutes into the flight and stuck a controlled splashdown in the Gulf of Mexico about six minutes after liftoff. That is a meaningful turnaround from Flight 12 in May, when the booster lost several engines during its boostback burn before a hard water landing attempt.

Starship as seen from Starlink satellites pic.twitter.com/e2hvfmnewh

— Elon Musk (@elonmusk) July 25, 2026

Starship 40’s performance was arguably the bigger win. The vehicle deployed the first 20 operational Starlink V3 satellites Starship has ever carried, then flew a suborbital arc to a landing in the Indian Ocean that SpaceX commentator Dan Huot called the company’s softest splashdown yet. “This is a dream scenario for this team that’s trying to get this heat shield data,” Huot said on the live broadcast, according to Space.com’s live coverage. “I’m a little over the moon right now. Wow. Lucky number 13.”

Unlike the mass simulators SpaceX flew on Flight 12, these were production Starlink V3 satellites, meant to extend solar arrays and antennas and attempt to link with the broader constellation before reentering minutes later. Getting real hardware through a full deploy sequence on only the second flight of the V3 generation keeps Starship on schedule for the payload work NASA is counting on for future Artemis lunar landings.

What an awesome launch, really seems like everything went super well and it was all incredibly smooth.

SpaceX is awesome. Very interested to see how the market will respond on Monday pic.twitter.com/KSHmyBfV55

— TESLARATI (@Teslarati) July 25, 2026

-

— TESLARATI (@Teslarati) July 25, 2026

The flight also arrives at a moment when SpaceX needed a win. SPCX has traded below its $135 IPO price since mid-July, as Teslarati reported when the mission slipped to Friday, and short interest has climbed to roughly a third of the tradable float. A clean flight will not fix a balance sheet, but it does answer the one question SpaceX absolutely needed answered this week: whether the fixes made after the July 16 abort would hold up under real flight conditions. They did, on both stages, on the first try after the redesign.

SpaceX has not set a target date for Flight 14, though the company has said it wants to push toward an orbital attempt on the next mission. After Friday, that goal looks a lot more within reach.

Tesla short sellers won big following the company’s massive fall on Wall Street after it reported subpar Earnings on Wednesday.

Tesla short sellers collected about $4.12 billion in single-day profits on Thursday, according to Bloomberg. Shares fell as much as 15 percent during Thursday’s session. It closed as one of the worst days for Tesla on Wall Street in the past three years.

Investors sold off the stock after Tesla said it would aggressively direct its spending toward AI and its Optimus robot project. The company had record revenues, which were driven by one of the strongest quarters in terms of vehicle deliveries in company history.

However, it missed EPS estimates by reporting just $0.33, a far cry from the $0.53 analysts expected.

S3 Partners reported that about 3 percent of Tesla’s outstanding stock is sold short. Managing Director at S3, Ihor Dusaniwsky, provided the short seller’s potential profit, as well as another figure: shorts have likely had paper gains of $8.92 billion this year, as Tesla shares are down 30 percent in 2026.

-

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Tesla has burned short sellers many times in the past, but the company’s latest Earnings Call was a chance for those skeptics to taste some payback. Although the company gave some very transparent information regarding future projects, the rollout of Robotaxi, Optimus, and Semi, many investors took their profits on Thursday.

Notable short sellers like Michael Burry have been transparent about their skepticism around Tesla shares. Burry just revealed three weeks ago that he had opened up a new short on the stock, stating he shorted Tesla shares at $416.22. “Happy it jumped back to this level,” he said in a blog post.

At the time of publication, Tesla shares were down about 3 percent and the stock was trading at $309.92.

Tesla stock (NASDAQ: TSLA) endured one of its sharpest single-day declines in years on July 23, tumbling approximately 14.5 percent and closing near $320 after opening the session around $374. The drop erased more than $140 billion in market value amid heavy trading volume and left the shares at multi-week lows.

The sell-off followed the company’s second-quarter 2026 results, released the previous evening. Tesla reported record revenue of $28.2 billion, up 26 percent year over year, driven by a Q2-record 480,126 vehicle deliveries. Energy storage deployments also rose strongly.

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Yet profitability disappointed sharply. Operating income fell 57 percent to $398 million, compressing the operating margin to just 1.4 percent. Non-GAAP earnings per share came in at $0.33, well below the roughly $0.53 analysts had expected. Free cash flow turned negative by $1.1 billion as capital expenditures surged 142 percent to $5.8 billion, largely tied to accelerated spending on artificial intelligence, robotics, and autonomous systems.

The losses on capex were expected, as Tesla said it would be spending heavily in 2026.

Investors also reacted to lingering uncertainty surrounding key product timelines. During the Earnings Call, management reiterated ambitions for Robotaxi deployment and the Optimus humanoid robot, but offered limited new concrete milestones, renewing questions about execution pace that have long accompanied Tesla’s ambitious roadmap.

The magnitude of the decline places it among Tesla’s more severe one-day percentage losses since its 2010 initial public offering. Historically, the two largest single-day drops (split-adjusted) remain September 8, 2020, when shares fell 21.1 percent amid broader market volatility and valuation concerns, and January 13, 2012, with a 19.3 percent plunge during the company’s early growth struggles.

-

Other notable declines include an 18.6 percent drop on March 16, 2020, at the onset of pandemic-related market turmoil. Thursday’s move ranks roughly ninth on the all-time list but stands out as the steepest in more than a year.

Despite the short-term pain, Tesla’s long-term trajectory has repeatedly recovered from such volatility. The latest results underscore both the strength of its core automotive and energy businesses and the near-term costs of heavy investment in next-generation technologies.

Tesla Full Self-Driving v14.3.6 review: a rare regression, but some bright spots

Musk’s massive Terafab project will get final location soon