SpaceX

SpaceX & ULA could compete to launch NASA’s Orion spacecraft around the Moon

In barely 48 hours, the future of NASA’s SLS rocket was buffeted relentlessly by a combination of new priorities in the White House’s FY2020 budget request and statements made before Congress by NASA administrator Jim Bridenstine. Contracted by NASA to companies like Boeing, the outright failure of SLS contractors to stem years of launch delays and billions in cost overruns has lead to what can only be described as a possible tipping point, one that could benefit companies like ULA, SpaceX, and Blue Origin.

On March 11th, the White House’s 2020 NASA budget request proposed an aggressive curtail of mission options available for the SLS rocket, preferring instead to save hundreds of millions (and eventually billions) of dollars by prioritizing commercial launch vehicles and indefinitely pausing all upgrade work on SLS. On March 13th, Administrator Bridenstine stated before Congress that he was dead-set on ensuring that NASA sticks to a current 2020 deadline for Orion’s first uncrewed circumlunar voyage (EM-1), even if it required using two commercial rockets (either Falcon Heavy or Delta IV Heavy) to send the spacecraft around the Moon next year. In both cases, it’s safe to say that the political tides have somehow undergone a spectacular 180-degree shift in attitude toward SLS, the first salvo in what is guaranteed to be a major political battle.

“Deferred” upgrades

Of the many potential challenges the ides of March have placed before SLS, the first and potentially most significant involves the rocket’s tentative path to future upgrades over the course of its operation. Those upgrades primarily center around the Exploration Upper Stage (EUS) and a new mobile launcher (ML) platform, as well as a longer-term vision known as SLS Block 2. At least with respect to the EUS, NASA (and politicians) were apparently less and less okay with the extraordinary amount of money and time Boeing suggested it would need to develop the new upper stage, to the extent that cutting (or “deferring”) its development could likely save NASA billions of dollars between now and the distant and unstable completion date. Without the EUS, SLS would be dramatically less useful for extreme deep space exploration, effectively the entire purpose of its existence. Instead, the White House included language that would limit SLS launches to crew transfer missions with the Orion spacecraft and nothing more, cutting out heavy cargo missions for science or station-building. Ultimately, those crew transport launches would probably be more than enough to keep SLS Block 1 and Orion busy.

However, two days later, Administrator Bridenstine stated before Congress that he was dead-set on ensuring that NASA sticks to a current 2020 deadline for Orion’s first uncrewed circumlunar voyage (EM-1), going so far as to suggest that NASA was examining the possibility of launching the ~26 ton (57,000 lb) spacecraft on a commercial rocket, followed by a separate launch of a boost stage to send Orion to the Moon. If this were to occur, the consequences could be far-reaching for SLS, potentially delaying the first crewed launch of Orion on SLS until EM-3 and creating a ready-made, one-to-one replacement for SLS at drastically lower costs. At that point, nothing short of political heroics and aggressive bribery could save the SLS program from outright cancellation.

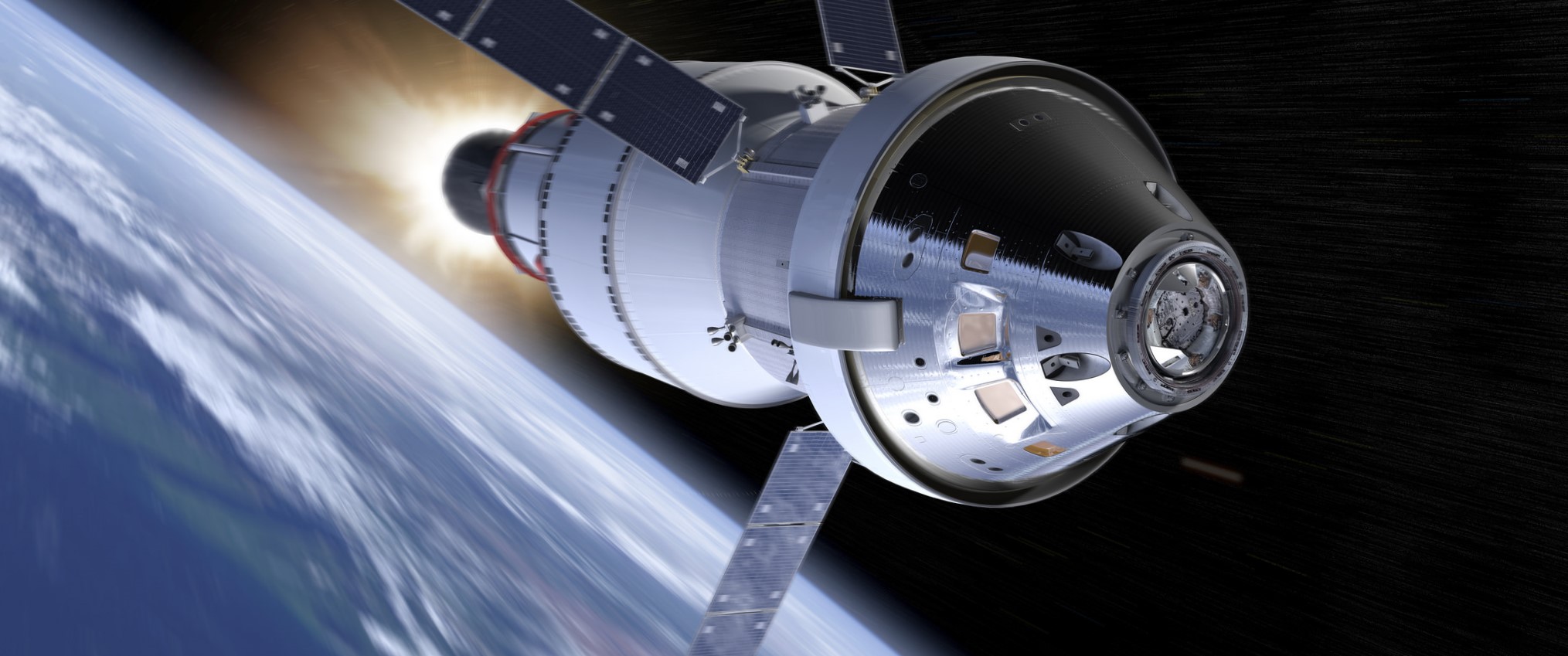

As it stands, the only rockets capable of conceivably supporting a 2020 launch of the 26-ton Orion are ULA’s Delta IV Heavy and SpaceX’s Falcon Heavy, both of which are certified by NASA for (uncrewed) launches. In fact, Falcon 9 was very recently certified by NASA’s Launch Services Program (LSP) to launch the highest priority NASA payloads, signifying the space agency’s growing confidence in SpaceX’s reliability and mission assurance. While the process of certifying Falcon Heavy for an uncrewed Orion launch would be far more complicated than simply grouping Falcon 9’s readiness with Heavy, it would no doubt help that Falcon Heavy is based on hardware (aside from the center core) almost identical to that found on Falcon 9.

The fact that Bridenstine indicated that the primary goal of these potential changes was to speed up EM-1 – an uncrewed demonstrated of Orion functionally similar to Crew Dragon’s recent DM-1 mission – is also significant, as is the fact that such a commercial SLS stand-in would require two separate launches to complete the mission. One launch would place Orion and its service module (ESM) into Low Earth Orbit (LEO), while a second launch would place a partially or fully-fueled upper stage into orbit to propel Orion on a trajectory that would take it around the Moon and back to Earth, similar to the milestone Apollo 8 mission. The need for two launches and the fact that Orion would be uncrewed means that both SpaceX and ULA would be possible candidates for either or both launches, potentially allowing NASA to exploit a competitive procurement process that could lower costs further still.

If Europa Clipper is anything to go off of, launching Orion EM-1 on a commercial rocket could save NASA and the US taxpayer at least $700M (before any potential development costs), aided further by potential competition between ULA and SpaceX. On the other hand, a system that can launch Orion and support EM-1 could fundamentally support all Orion EM missions, of which many are planned. Whether or not Bridenstine and the White House have considered the ramifications, what that translates into is a direct and pressing threat to the continued existence of SLS, with the White House recommending that the rocket be barred from launching large science missions or space station segments as the NASA administrator proposes making it redundant for Orion launches. As Ars Technica’s Eric Berger rightly notes in the tweet at the top of this article, those are the only three conceivable projects where SLS would have any value at all.

If NASA actually went through with this preliminary plan to launch Orion around the Moon on a commercial rocket, they agency would have also fundamentally created a packaged replacement for SLS with a price tag likely 2-5 times cheaper. If Congress had the option to choose between two offerings with similar end-results where one of the two could save the US hundreds of millions of dollars at minimum, it would be almost impossible to argue for the more expensive solution.

Battle of the Heavies

Despite the potential competitive procurement opportunity for a commercial Orion launch, things could get significantly more complicated depending on the political motivations behind the White House and NASA administrator. While Bridenstine explicitly avoided saying as much, the options available to NASA would be ULA’s Boeing-built Delta IV Heavy (DIVH) rocket and SpaceX’s brand new Falcon Heavy. DIVH holds a present-day advantage with active NASA LSP certification for uncrewed spacecraft launches, something Falcon Heavy has yet to achieve.

Nevertheless, it could be the case that NASA, Bridenstine, and/or the White House have a vested interested in potentially replacing SLS for crewed Orion launches entirely. Either way, it’s incredibly unlikely that NASA would launch SLS for the first time ever with astronauts aboard, a massive risk that would also patently contradict the agency’s posture on Commercial Crew launch safety, which has resulted in one uncrewed demo for both Boeing and SpaceX before either be allowed to launch astronauts. NASA also demanded that SpaceX launch Falcon 9 Block 5 seven times in the same configuration meant to launch crew. If NASA is actually interested in at least preserving the option for future crewed launches using the same commercial arrangement, Falcon Heavy is by far the most plausible option Orion’s first uncrewed launch. NASA and SpaceX are deep into the process of human-rating Falcon 9 for imminent Crew Dragon launches with NASA astronauts aboard, meaning that NASA’s human spaceflight certification engineers are about as intimately familiar with Falcon 9 as they possibly can be.

Given that much of Falcon Heavy has direct heritage to Falcon 9, particularly so for the family’s newest Block 5 variant, SpaceX has a huge leg up over ULA’s Delta IV Heavy if it ever came time to certify either heavy-lift rocket for crewed launches. In a third-party study commissioned by NASA and completed in 2009, The Aerospace Corporation concluded that Delta IV Heavy could be human-rated but would require far-reaching modifications to almost every aspect of the rocket’s hardware and software. Most notably, Aerospace found – in a truly ironic twist of fate – that Boeing would likely need to develop a wholly new upper stage for a human-rated Delta IV Heavy, increasing redundancy by increasing the number of RL-10 engines from two to four. As proposed by Boeing, the Exploration Upper Stage – under threat of deferment due to high cost and slow progress – would also feature four RL-10 engines and much of the same upgrades Boeing would need to develop for EUS. Aside from an entirely new upper stage, ULA would also need to develop and qualify an entirely new variant of the RS-68A engine that powers each DIVH booster. Ultimately, TAC believed it would take “5.5 to 7 years” and major funding to human-rate Delta IV Heavy.

Meanwhile, Falcon Heavy already offers multiple-engine-out capabilities, uses the same M1D and MVac engines – as well as an entire upper stage – that are on a direct path to be human-rated later this year, and two side boosters with minimal changes from Falcon 9’s nearly human-rated booster. NASA would still need to analyze the center core variant and stage separation mechanisms, as well as Falcon Heavy as an integrated and distinct system, but the odds of needing major hardware changes would be far smaller than Delta IV Heavy.

Regardless, it will be truly fascinating to see how this wholly unexpected series of events ultimately plays out as Congress and its several SLS stakeholders begin to analyze the options at hand and (most likely) formulate a battle plan to combat the threats now facing the NASA rocket. According to Administrator Bridenstine, NASA will have come to a final decision on how to proceed with Orion EM-1 as soon as a few weeks from now.

Check out Teslarati’s Marketplace! We offer Tesla accessories, including for the Tesla Cybertruck and Tesla Model 3.

SpaceX announced today that it commenced its first-ever public bond offering, marking a significant step in the newly public company’s capital markets strategy.

The company announced an offering of senior unsecured notes expected to raise at least $20 billion.

The move comes just a short time after SpaceX completed one of the largest initial public offerings in history. In mid-June, the company priced shares at $135 and raised more than $85 billion, propelling founder Elon Musk’s net worth past the trillion-dollar mark and giving the firm substantial liquidity.

🚨 SpaceX has announced its inaugural offering of senior unsecured notes.

The net proceeds will be used to repay outstanding loans under its bridge loan facility in full.

This inaugural debt offering represents a financing milestone for SpaceX, which previously depended… pic.twitter.com/pcOZuVbTRv

— TESLARATI (@Teslarati) June 22, 2026

According to the company’s SEC filing, the net proceeds from the notes will be used primarily to repay in full the outstanding borrowings under its existing bridge loan facility, cover related fees and expenses, and fund general corporate purposes. The offering is being conducted under Rule 144A, as well as Regulation S, targeting qualified institutional buyers and non-U.S. investors. Notes will be unsecured obligations ranking equally with other unsubordinated debt.

The $20 billion bridge loan was used to refinance approximately $17.5 billion in higher-cost “junk” debt tied to X and xAI. SpaceX had merged with xAI in February 2026 in an all-stock deal. The bridge facility, which matures in September 2027, had represented the bulk of SpaceX’s long-term debt.

SpaceX officially acquires xAI, merging rockets with AI expertise

In connection with the bond launch, SpaceX disclosed it held approximately $100.8 billion in cash and cash equivalents as of June 19. Investor calls began on the announcement date, with pricing and launch expected shortly thereafter. Rating agencies have assigned investment-grade ratings to the proposed bonds, reflecting confidence in SpaceX’s dominant position in commercial launches and the growth trajectory of its Starlink internet offering.

The debt raise also allows SpaceX to optimize its balance sheet by replacing short-term, higher-cost bridge financing with longer-date, lower-cost fixed-income securities. This provides greater financial flexibility to support capital-intensive initiatives, including the development of Starship, the expansion of the Starlink constellation, and the integration of AI capabilities following the xAI combination.

SpaceX shares (NASDAQ: SPCX) fell sharply on the news, dropping over 16 percent overall on the market on Monday. The stock had surged initially after debuting but pulled back amid profit-taking and broader market dynamics.

Overall, the bond offering underscores SpaceX’s transition to a mature public company with access to diverse funding sources. It positions the firm to pursue its long-term vision of multiplanetary expansion and AI infrastructure, while maintaining a disciplined approach to its capital structure in a high-growth but capital-heavy industry.

SpaceX confirmed today that it has officially signed its third massive compute deal, providing compute at its Colossus data center in Southaven, Mississippi.

Reflection AI will gain immediate access to NVIDIA GB300 chips at SpaceX’s Colossus 2 data center. In return, Reflection will pay SpaceX $150 million per month starting on July 1, with total payments reaching approximately $6.3 billion if the contract runs through its duration, which is until 2029. Either party can terminate the agreement with 90 days’ notice after the initial three-month period.

CNBC first reported the deal.

🚨 SpaceXAI has agreed to a new compute deal with Reflection AI.

Reflection gets access to NIVIDIA GB300s, and will pay $150M per month to SpaceXAI for the compute. pic.twitter.com/bNPare8U5u

— TESLARATI (@Teslarati) June 22, 2026

This latest partnership highlights SpaceX’s strategy of commercializing its massive Colossus supercomputing infrastructure, originally developed to power Elon Musk’s Grok AI models. The company has rapidly expanded its customer base in the AI sector following its February 2026 merger with xAI, a transaction that valued the combined entity at $1.25 trillion.

SpaceX has previously signed significant compute deals with other major players.

It granted Anthropic exclusive access to the full capacity of its Colossus 1 data center, which exceeds 300 megawatts and includes over 220,000 NVIDIA GPUs. Details from SpaceX’s IPO filings indicate Anthropic will pay $1.25 billion per month through May 2029, potentially generating around $45 billion over the term of the deal.

Additionally, Google agreed to pay SpaceX $920 million per month for compute capacity from October 2026 through June 2029. This 32-month period will provide Google access to roughly 110,000 NVIDIA GPUs, along with supporting processors and memory. Capacity ramps up through September at a reduced fee, with termination options after the first year.

SpaceXA also established arrangements for computing power with Cursor, an AI coding startup. SpaceX acquired them in a $60 billion all-stock deal.

These arrangements position SpaceX’s collective position as an AI infrastructure powerhouse with high-margin revenue potential. The Google deal alone could generate nearly $29.5 billion over its term, while the Reflection contract adds another $6.3 billion.

Combined with the Anthropic arrangement, SpaceX stands to realize tens of billions in revenue from compute leasing in the coming years, which diversifies beyond SpaceX’s traditional rocket launches and Starlink operation.

The deals underscore growing demand for advanced AI training and inference capacity amid chip shortages and surging model development needs. Reflection, valued at $25 billion and focused on “American open intelligence” with government and national security ties, cited recent restrictions on closed models as validation for open-source approaches.

For SpaceX, the partnerships transform capital-intensive data centers into flexible revenue sources while supporting its broader AI ambitions after the company has gone public.

It is safe to say SpaceX won’t be going for electric rockets anytime soon.

In a characteristically blunt reply on X, SpaceX frontman Elon Musk stated, “Unfortunately, electric rockets are impossible,” following reports that MSCI had assigned SpaceX its lowest possible ESG rating of CCC.

The assessment, issued just this past week, coinciding closely with SpaceX’s public market debut, placed the company on par with nations like Russia in sustainability scoring and cited significant risks in environmental, social, and governance areas.

MSCI flagged SpaceX’s exposure to rocket emissions and other operational impacts, alongside governance concerns such as concentrated control by Musk and limited shareholder protections. Musk’s terse comment directly addressed the environmental pillar, underscoring a core physical constraint that ESG frameworks often overlook when evaluating high-thrust industries.

Unfortunately, electric rockets are impossible

— Elon Musk (@elonmusk) June 21, 2026

Electric propulsion systems do exist and are widely used in space. Ion thrusters and Hall-effect thrusters accelerate ionized propellant, typically xenon or krypton, using electric fields, achieving very high specific impulse, often exceeding 3,000 seconds compared to roughly 300–450 seconds for chemical rockets.

This efficiency makes them ideal for satellite station-keeping, orbit raising, and deep-space missions where low thrust over long durations is sufficient. SpaceX’s own Starlink satellites employ electric propulsion for these purposes.

However, launching from Earth’s surface demands something entirely different: enormous thrust delivered rapidly to overcome gravity and atmospheric drag. A typical orbital-class booster must generate thrust far exceeding its weight, often in the millions of Newtons within seconds.

Chemical rockets achieve this through exothermic combustion of dense propellants, producing high-mass-flow, high-velocity exhaust. Electric systems, by contrast, expel very small amounts of mass at extremely high speeds. Generating equivalent thrust would require impractical onboard power levels, massive energy storage or generation systems, and prohibitive added mass, rendering the approach infeasible with current or near-term technology.

Musk has previously expressed a similar sentiment, noting a desire for electric orbital rockets while acknowledging the inescapable requirements of Newton’s third law and energy delivery. The distinction is clear: electric propulsion excels once a vehicle is already in space; it cannot replace the high-thrust chemical phase required to reach orbit from the ground.

The episode illustrates broader critiques of ESG ratings. Proponents argue they incentivize better risk management and long-term sustainability. Detractors, including Musk—who has previously called ESG a “scam”—contend that such metrics can penalize essential activities when no practical alternative exists, potentially discouraging innovation in sectors like space access.

Elon Musk dubs the S&P 500 ESG as “outrageous scam” after Tesla gets booted from index

SpaceX has sought to mitigate launch-related impacts through reusability: Falcon 9 boosters have flown more than 30 times in some cases, dramatically lowering the manufacturing and emissions burden per kilogram delivered to orbit. Starship’s design further emphasizes rapid reusability and methane propellant, which can theoretically be produced via sustainable pathways.

Ultimately, Musk’s remark serves as a reminder that certain engineering realities persist regardless of scoring systems. As humanity expands its presence in space for communications, science, and exploration, balancing genuine environmental progress with technological necessity remains a central challenge.

ESG frameworks may evolve, but the fundamental limits of electric launch propulsion are unlikely to change soon.

Tesla finally clarifies fatal Texas crash, confirms driver manually overrode acceleration

SpaceX makes $20 billion move to optimize its balance sheet