Investor's Corner

Tesla shares company-compiled analyst consensus for Q4 2024 deliveries

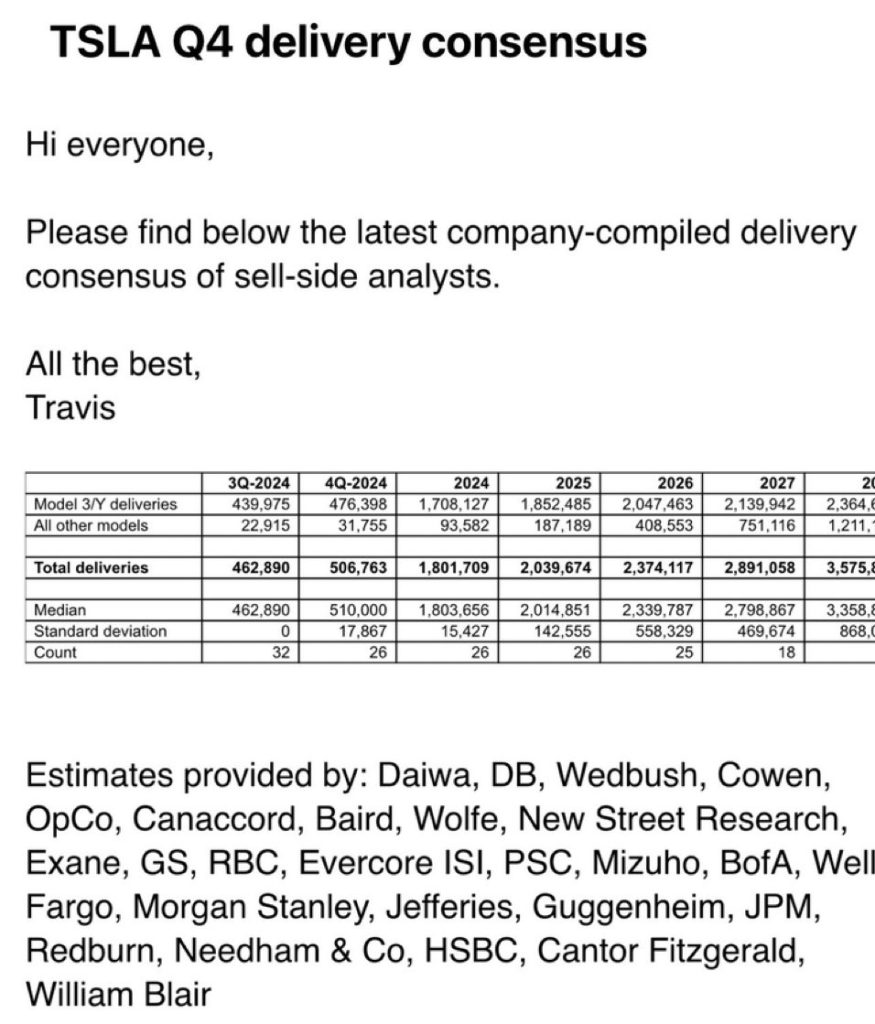

Tesla (NASDAQ:TSLA) has shared its latest company-compiled delivery consensus from sell-side analysts. Based on the consensus, analysts are not expecting Tesla to beat its annual delivery figures from 2023.

The consensus:

- As per Tesla’s company-compiled consensus, analysts are expecting the electric vehicle maker to post 506,763 vehicle deliveries for Q4 2024.

- Analysts expect Tesla to report 476,398 Model 3 and Model Y deliveries, as well as 31,755 deliveries of all other models.

- With these results, Tesla’s company-compiled consensus expects a global total of 1,801,709 vehicle deliveries for 2024.

Tesla’s sources:

- The analyst consensus for Tesla’s Q4 2024 vehicle delivery results was provided by the following firms:

- Daiwa, DB, Wedbush, Cowen, OpCo, Canaccord, Baird, Wolfe, New Street Research, Exane, GS, RBC, Evercore ISI, PSC, Mizuho, BofA, Well Fargo, Morgan Stanley, Jefferies, Guggenheim, JPM, Redburn, Needham & Co, HSBC, Cantor Fitzgerald, and William Blair

Tesla’s Q4 consensus vs 2023’s deliveries:

- For comparison, Tesla reported a total of 484,507 vehicle deliveries for Q4 2023.

- These were comprised of 461,538 Model 3 and Model Y, as well as 22,969 units of Tesla’s other models.

- With these results, Tesla delivered a total of 1,808,581 vehicles globally in Full Year 2023.

Tesla’s FY 2024 deliveries in context:

- For Tesla to match its 2023 delivery numbers, the company would have to deliver about 515,000 vehicles this fourth quarter.

- This, however, would require Tesla to deliver the most vehicles it has ever delivered in a quarter.

- Even if Tesla does not meet its 2023 figures this year, the company’s overall performance is not as grim as what skeptics may believe.

- Tesla’s business, after all, is no longer just focused on its automotive division. Tesla Energy is growing rapidly, and the company’s work on its FSD system could pave the way for a software licensing business in the long run.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Elon Musk

Tesla Semi finally has an FSD timeline and it’s waiting on the Cybercab

Elon Musk told investors Semi self-driving should start working by early 2027, per today’s earnings.

During Wednesday’s’ Tesla Q2 earnings call, an analyst asked Elon Musk when Tesla would look at autonomy for the Semi. His answer set a real timeline for the first time, noting that self-driving on the Tesla Semi is expected to start working “around the end of this year or early next year”.

Musk framed the delay as a matter of priority, not capability. Tesla’s self-driving team is currently focused on Model 3, Model Y, and Cybercab, the vehicles that make up the overwhelming majority of Tesla’s fleet. Since Semi trucks on the road remain a small fraction of that total even after the recent Nevada factory ramp, Musk said it made more sense to keep the software team’s attention on what he called “the march of nines of safety” for the higher volume vehicles first. Autonomous Semi development is “taking a bit of a backseat for the next six months or so,” he said, before adding that it “will definitely be working next year and in time for the scale-up to high production of the Tesla Semi.”

Tesla Semi’s official battery capacity leaked by California regulators

The timeline lines up with what’s already been showing up on public roads. In June, a Tesla Semi was spotted in Sunnyvale wearing a full validation rig, the same rooftop sensor array Tesla mounts on vehicles ahead of an FSD milestone.

A second unit was seen near Fremont days later with a matching camera suite and lens washers. Separately, Tesla analyst Nic Cruz Patane posted video this month of the production Semi’s exterior camera array, ten AI4 based units built directly into the truck rather than added later.

Tesla Semi AI4 cameras. The production version has 10 cameras on its exterior.

These trucks are designed to be autonomous. pic.twitter.com/GH3BamxIBQ

— Nic Cruz Patane (@niccruzpatane) April 14, 2026

Musk also gave the reason autonomy on the Semi matters in the first place, a persistent shortage of qualified truck drivers. “There is a really serious shortage of truckers,” he said on the call, framing a self-driving Semi as important both for addressing that shortage and for improving safety and comfort for the drivers running the truck today.

The timing also tracks with the Semi’s production reality. Tesla’s Q2 shareholder letter, dropped language promising the Semi would reach volume production this year. Musk pointed to 4680 battery cell output as the near-term constraint on Semi and Cybercab production. A software timeline landing in early 2027 gives Tesla’s autonomy team room to work while the hardware ramp catches up behind it.

It’s worth nothing that this isn’t necessarily a promise the Semi ships driverless next year. Musk’s own language, self-driving “working” by early 2027, describes internal validation catching up to hardware already riding on every production truck, not a public unsupervised rollout.

Tesla (NASDAQ: TSLA) reported its earnings for the first quarter of 2026 on Wednesday afternoon. Here’s what the company reported compared to what Wall Street analysts expected.

The earnings results come after Tesla reported a massive beat on vehicle deliveries for the second quarter, delivering 489,126 vehicles and building 451,758 cars during the three-month span.

This was a major shock for those on Wall Street as they anticipated somewhere around 400,000 deliveries for the quarter, and showed Tesla still has plenty of demand for its vehicles around the world and in the U.S. despite losing the $7,500 EV Tax Credit last year.

Tesla Q2 2026 Earnings Results

- Non-GAAP EPS – $0.33 reported vs. $0.53 expected

- Revenues – $28.236 billion reported vs. $26.4 billion expected

- Free Cash Flow- -$1.092B

- Profit -$ 4.751B

Tesla (beat/missed) analyst expectations, so the market response to the company’s quarter is what we will look for next.

Tesla shares closed today down just over 1 percent, trading at $374.01.

In the past, it has been anyone’s guess with what Tesla shares will do after they report earnings. Strong quarters have resulted in sharp drops, while lackluster quarters have seen the stock shoot up considerably.

Tesla will hold its Q2 2026 Earnings Call in about 90 minutes at 5:30 p.m. on the East Coast. Remarks will be made by CEO Elon Musk and other executives, who will shed some light on the investor questions that we covered earlier this week.

You can stream it below. Additionally, we will be doing our Live Blog on X and Facebook.

Q2 2026 Earnings Call https://t.co/zZS6ii2TWK

— Tesla (@Tesla) July 22, 2026

Tesla (NASDAQ: TSLA) will report its earnings for the second quarter of 2026 this evening after market close, and investors and analysts are waiting anxiously to see what the company will report for the second three-month span of the year.

Analysts have already put out their expectations from a financial standpoint for the company’s second quarter, but what’s unknown is what Tesla plans to discuss during the call.

Financial Expectations

Wall Street consensus expectations put Tesla’s Earnings Per Share (EPS) at $0.53, while revenues are expected to come in around $26.4 billion.

This would compare to an EPS of $0.39 and $22.19 billion compared to Tesla’s Q2 2025. Last quarter, EPS came in at $0.41 on $22.387 billion of revenue. Additionally in Q1, Tesla beat analyst expectations, but shares dropped over 3 percent the following trading day.

What We Expect

In terms of discussions, Tesla earnings are pretty sporadic and depend on a handful of things, including current events, investor questions, and more.

Tesla uses a platform called Say to field questions from investors and analysts. These questions are what will be used during the call. Here are the top 5 from the Retail side and top 3 from the Institutional side:

Retail:

“Tesla has missed short-term guidance on robotaxi 3 earnings reports in a row, from 50% coverage of USA by end of 2025 to most recently 7 new cities in 1H26. What is keeping Tesla back from accomplishing these short term goals that they’ve set for themselves?”

“What are the main constraints to expanding robotaxi operations faster, and how do you see that lining up with Cybercab production?”

“What’s the current status of Optimus Gen 3 production ramp, initial deployment in factories, and external sales timeline/volume for 2027? What tasks can we expect the Optimus to perform by end of 2027?”

“To reward long-term Tesla retail shareholders for their loyalty, can you commit to achieving at least half of the goals outlined in your 2025 compensation plan before considering any offers to acquire or merge Tesla?”

“Why has growth of robotaxi vehicles stalled? When will we see cybercab start customer rides?”

Institutional

“Previously, you’ve said Tesla would lead the R&D while SpaceX would lead production for Terafab. Can you provide an update on how that division of responsibilities is evolving, and any additional clarity on the expected capital contributions from Tesla and SpaceX?”

“For autonomous driving, Tesla’s fleet created a huge data advantage by collecting billions of real-world miles. That advantage doesn’t yet exist for Optimus. How should we think about data availability and its impact on Optimus development?”

“Why is it necessary to limit robotaxi operations within specific zones within cities to start? Will every city have to be rolled out this way?”

Tesla will report earnings for Q2 this evening with the Shareholder Deck at 4 p.m. ET, with the call starting around 5:30 p.m. ET.

Tesla’s switch-up on selling Full Self-Driving has paid off big time

Tesla Robotaxi’s slow rollout gets explanation from Elon Musk