Investor's Corner

Tesla’s (TSLA) Q2 2019 earnings call: Here are Wall Street’s estimates

Tesla (NASDAQ:TSLA) is poised to hold its second-quarter earnings call after the markets close on Wednesday. With the electric car maker exceeding expectations on its vehicle production and deliveries, all eyes are now on the company as it tries to return to profitability, which it was able to achieve in the third and fourth quarter of 2018.

Bill Selesky, an analyst with Argus Research, stated that the story of Tesla’s second-quarter immediately changed when it reported its production and delivery figures, which exceeded expectations. “We are still hearing that demand trends bode well for Tesla. What remains to be seen is whether Tesla will rein in its costs and expenses and improve its margins,” he said.

Garrett Nelson, an analyst with CFRA Research, noted that investors would likely be focused on whether the company will keep its initial forecast of selling 360,000-400,000 vehicles in 2019. “The ability of the stock to move higher will really depend on the (sales) guidance. We are still skeptical that they will hit that goal,” the CFRA analyst stated.

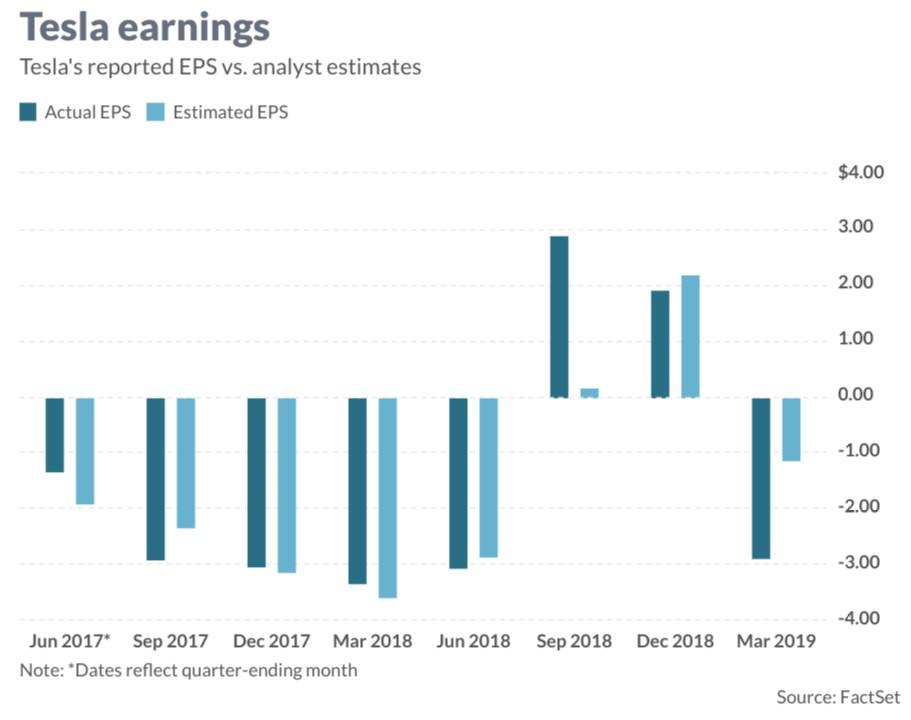

Overall, analysts polled by FactSet expect Tesla to report an adjusted quarterly loss of $0.39 per share, a notable improvement over the $3.06 loss the company reported in Q2 2018. Wall Street also expects Tesla to return to non-GAAP profitability by the fourth quarter.

Estimize, a crowdsourcing platform that aggregates estimates from Wall Street analysts, buy-side analysts, company executives, fund managers, academics and others, has noted that it expects Tesla to report an adjusted loss of $0.25 per share.

As for revenue, FactSet expects Tesla to report sales of $6.5 billion in the second quarter, an improvement over the $4 billion the company reported in Q2 2018 and the $4.5 billion in the first quarter. Estimize, for its part, expects Tesla to report sales of $6.6 billion.

Tesla has been on what appears to be a path towards recovery in July. TSLA shares have recovered 14% this month, following a 21% recovery in June. Due to the steep drop in the electric car maker’s shares following the first quarter, Tesla remains down 23% for 2019. This compares unfavorably with the S&P 500 index and the Dow Jones Industrial Average, which have gained 19% and 17%, respectively.

Selesky’s statement about the Tesla story changing with the results of the second-quarter vehicle production and delivery report mirrors the sentiments of some of the company’s supporters in Wall Street. In a recent note, for example, Baird analyst Ben Kallo stated that Tesla’s further execution, starting with its second-quarter earnings report, will “help restore credibility and create a challenging short environment” despite the “overly negative” narrative surrounding the company.

-

-

Even Barclays analyst Brian Johnson, a Tesla bear, has issued a note stating that he sees the electric car maker heading to a nearly profitable Q2 earnings report. “Increasing 2Q estimates as TSLA did indeed ‘move the metal,’” Johnson wrote.

As of writing, Tesla stock is trading +0.84% at $260.36 per share.

Disclosure: I have no ownership in shares of TSLA and have no plans to initiate any positions within 72 hours.

Elon Musk

The real reason Elon Musk wants every car connected to space

Elon Musk says all cars will eventually need Starlink to handle massive AI bandwidth demand.

Elon Musk is making the case that satellite internet, not fiber or cellular towers, will end up wired into every car on the road. In a string of posts on X, the SpaceX CEO wrote that all cars will have Starlink in the future and called satellite connectivity the only way to get super high bandwidth to billions of vehicles.

The posts started with Musk endorsing a Cloudflare forecast that traffic generated by autonomous AI agents will soon dwarf traffic generated by humans browsing the internet, a shift he described as not a close call at all. From there he narrowed the argument to infrastructure, writing that the only system that can support the insanely fast bandwidth growth needed by AI is Starlink, before extending the logic to cars specifically.

AI agentic Internet traffic will obviously VASTLY exceed human usage. Not a close call at all.

Cloudflare’s forecast is accurate. https://t.co/VztgrinN5k pic.twitter.com/Wo4FiRKjPU

— Elon Musk (@elonmusk) August 9, 2026

The timing lines up with Tesla’s own hardware decisions. On July 20, Tesla confirmed the Cybercab would ship with a Starlink V5 terminal built into its roof, the first time the company had put satellite hardware in a production vehicle. A day later, Tesla’s head of AI, Ashok Elluswamy, explained the connection wasn’t there for safety and that Cybercab’s driving stack runs entirely on onboard cameras and compute, while the satellite link exists for navigation, customer service, and fleet management instead. Musk followed with his own post about the feature, saying riders would be able to watch 4K streaming video during rides.

By July 22, Musk had already said Starlink would extend beyond Cybercab to Tesla’s full lineup. Sunday’s posts push that same logic outward again, this time framed as a requirement across the industry rather than a feature specific to Tesla, and tied directly to the bandwidth AI systems are expected to consume.

SpaceX’s newest Starmind will make earth data centers obsolete

The AI argument has been building on SpaceX’s side for months. The company has an FCC filing pending for a third generation Starlink constellation, and it has separately proposed Starmind, a constellation of up to a million satellites designed to run AI computation directly in orbit rather than just relay data. Musk has said he expects space to become the cheapest place to deploy AI compute within two to three years. Starlink and Starmind serve different jobs inside that vision, one moving data and the other processing it, but Sunday’s posts treat vehicles as one more category of hardware that will eventually need both.

None of this changes anything for Tesla owners today. Cars already on the road keep running on LTE and Wi-Fi, and Tesla hasn’t outlined a retrofit path for existing vehicles. The July 22 commitment applies to future production, not the fleet already delivered. What Musk added on Sunday is the reasoning: satellite connectivity isn’t a Cybercab novelty, it’s a bet that ground based networks won’t keep up with how much data cars, robots, and AI systems are about to generate.

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

Cybertruck

Tesla Cybertruck production snaps back after ugly supplier fight

Cybertrucks are piling up again at Giga Texas after Tesla’s court win against a parts supplier.

Cybertruck production at Giga Texas is showing its first visible recovery since Tesla sued a supplier last month over withheld manufacturing tooling.

Aerial observer Joe Tegtmeyer flew over the Austin factory Wednesday morning and counted roughly 100 or more Cybertrucks filling the outbound lot, a sharp jump from the thin numbers seen in recent weeks. The flyover came a day after a judge granted Tesla a temporary restraining order against Angstrom Automotive Group, the parts supplier at the center of the dispute.

Tesla filed an emergency lawsuit in late July after Angstrom told the automaker it planned to close the Troy, Texas facility where Tesla’s die-cast tools, trim dies and other Cybertruck stamping equipment were housed. According to Tesla’s complaint, a shipment of 700 finished parts never left the building, and when Tesla sent representatives to retrieve its equipment, accompanied by law enforcement, they were turned away. Angstrom allegedly then asked for an extra $250,000 a week to keep operating, which Tesla’s filing described as holding its own property for ransom.

TESLA: U.S. District Judge Christopher R. Wolfe of the U.S. District Court for the Western District of Texas, Waco Division granted Tesla a Temporary Restraining Order and Writ of Replevin in its dispute with Angstrom Automotive (Case No. 6:26-cv-00477).

The order authorizes… https://t.co/E1DKcQSxMn pic.twitter.com/LR8aAiV2Og

— S.E. Robinson, Jr. (@SERobinsonJr) August 5, 2026

The restraining order gives Tesla immediate right of entry to Angstrom’s facility to recover the tooling. It is temporary, with a fuller hearing still to come, but the speed of Wednesday’s rebound suggests the Angstrom shortage was indeed the main bottleneck limiting Cybertruck output. Outbound lot counts are an imperfect measure of actual production, since finished trucks can sit for days before shipping, but a lot that full after a lean stretch is a meaningful signal.

Cybertruck output at Giga Texas has fluctuated all year as Tesla worked through supply issues and introduced new trims, including a cheaper Dual Motor AWD version that drew strong early demand.

The real reason Elon Musk wants every car connected to space

Inside Tesla’s secretive $10 Billion “Project Crystal Sun” filing