Investor's Corner

Tesla wins $508 price target from Stifel as Robotaxi rollout gains speed

The firm cited meaningful progress in Tesla’s robotaxi roadmap, ongoing Full Self-Driving enhancements, and the company’s long-term growth initiatives.

Tesla received another round of bullish analyst updates this week, led by Stifel, raising its price target to $508 from $483 while reaffirming a “Buy” rating. The firm cited meaningful progress in Tesla’s robotaxi roadmap, ongoing Full Self-Driving enhancements, and the company’s long-term growth initiatives.

Robotaxi rollout, FSD updates, and new affordable cars

Stifel expects Tesla’s robotaxi fleet to expand into 8–10 major metropolitan areas by the end of 2025, including Austin, where early deployments without safety drivers are targeted before year-end. Additional markets under evaluation include Nevada, Florida, and Arizona, as noted in an Investing.com report. The firm also highlighted strong early performance for FSD Version 14, with upcoming releases adding new “reasoning capabilities” designed to improve complex decision-making using full 360-degree vision.

Tesla has also taken steps to offset the loss of U.S. EV tax credits by launching the Model Y Standard and Model 3 Standard at $39,990 and $36,990, Stifel noted. Both vehicles deliver more than 300 miles of range and are positioned to sustain demand despite shifting incentives. Stifel raised its EBITDA forecasts to $14.9 billion for 2025 and $19.5 billion for 2026, assigning partial valuation weightings to Tesla’s FSD, robotaxi, and Optimus initiatives.

TD Cowen also places an optimistic price target

TD Cowen reiterated its Buy rating with a $509 price target after a research tour of Giga Texas, citing production scale and operational execution as key strengths. The firm posted its optimistic price target following a recent Mobility Bus tour in Austin. The tour included a visit to Giga Texas, which offered fresh insights into the company’s operations and prospects.

Additional analyst movements include Truist Securities maintaining its Hold rating following shareholder approval of Elon Musk’s compensation plan, viewing the vote as reducing leadership uncertainty.

@teslarati Tesla Full Self-Driving yields for pedestrians while human drivers do not…the future is here! #tesla #teslafsd #fullselfdriving ♬ 2 Little 2 Late – Levi & Mario

Elon Musk

Tesla FSD in Europe vs. US: It’s not what you think

Tesla FSD is approved in the Netherlands, but the European version differs from what US drivers use.

On April 10, 2026, the Dutch vehicle authority RDW granted Tesla the first European type approval for Full Self-Driving Supervised, making the Netherlands the first country on the continent to authorize Tesla’s semi-autonomous system for customer use on public roads.

As Teslarati reported, the RDW approval followed 18 months of testing, more than 1.6 million kilometers driven on EU roads, 13,000 customer ride-alongs, and documentation covering over 400 compliance requirements. Tesla Europe had been running public demo drives through cities like Amsterdam and Eindhoven since early 2026, giving passengers their first experience of the system on European streets.

The European version of FSD is not the same software US drivers use. The RDW’s own statement is direct, noting that the software versions and functionalities in the US and Europe “are therefore not comparable one-to-one.” We’ve compile a table below that captures the most significant differences between US-based Tesla FSD vs. European Tesla FSD that’s based on what regulators and Tesla have publicly confirmed.

| Feature | FSD US | FSD Europe (Netherlands) |

| Regulatory framework | Self-certification, post-market oversight | Pre-market type approval required (UN R-171 + Article 39) |

| Hands requirement | Hands-off permitted on highway | Hands must be available to take over immediately |

| Auto turning from stop lights | Available — navigates intersections, turns, and traffic signals autonomously | Available in EU build — confirmed in Amsterdam demo footage handling unprotected turns and signalized intersections |

| Driving modes | Multiple profiles including a more aggressive “Mad Max” mode | EU build is more conservative by default and errs on the side of restraint when it cannot confirm the limit |

| Summon | Available — Smart Summon navigates parking lots to driver | Status unclear — not confirmed as part of the RDW-approved feature set; urban FSD approval targeted separately for 2027 |

| Driver monitoring | Camera-based eye tracking | Stricter continuous monitoring with more frequent intervention alerts |

| Software version | FSD v14.3 | EU-specific builds that must be separately validated by RDW |

| Geographic restriction | US, Canada, China, Mexico, Australia, NZ, South Korea | Netherlands only; EU-wide vote pending summer 2026 |

| Subscription price | $99/month | €99/month |

| Full urban FSD scope | Available | Partial — separate urban application planned for 2027 |

The approval comes as Tesla is under real pressure to grow FSD subscriptions globally. Musk’s 2025 CEO compensation package, approved by shareholders, includes a milestone requiring 10 million active FSD subscriptions as one condition for his stock awards to vest. Tesla hit one million subscriptions during its Q4 2025 earnings call, which is a meaningful start, but still a long way from the target. Opening Europe as a market for subscriptions, rather than just hardware sales, directly accelerates that number.

Tesla has said it anticipates EU-wide recognition of the Dutch approval during summer 2026, which would extend FSD access to Germany, France, and other major markets through a mutual recognition process without each country repeating the full 18-month review. That timeline is Tesla’s projection, not a confirmed regulatory outcome. As Musk acknowledged at Davos in January 2026, “We hope to get Supervised Full Self-Driving approval in Europe, hopefully next month.”

Elon Musk

Tesla Supercharger for Business exposes jaw-dropping ROI gap between best and worst locations

Tesla’s new Supercharger for Business calculator reveals an eye-opening all-in cost and location-based ROI projections.

Tesla has launched an online calculator for its Supercharger for Business program, giving property owners their first transparent look at what it really costs to install Superchargers on site and what kind of return they can expect.

The program itself launched in September 2025, allowing businesses to purchase and operate Supercharger hardware on their own property while Tesla handles installation, maintenance, software, and 24/7 driver support. As Teslarati reported at launch, hosts also get their logo placed on the chargers and their location integrated into Tesla’s in-car navigation, meaning drivers are actively routed there. The stalls are open to all EVs, not just Teslas.

We launched Supercharger for Business in 2025 to help companies get charging right. We found simplicity and transparency to be a problem in this industry.

We’re now sharing pricing and a financial calculator to help make informed decisions. The goal is to accelerate investments,…

— Tesla Charging (@TeslaCharging) April 8, 2026

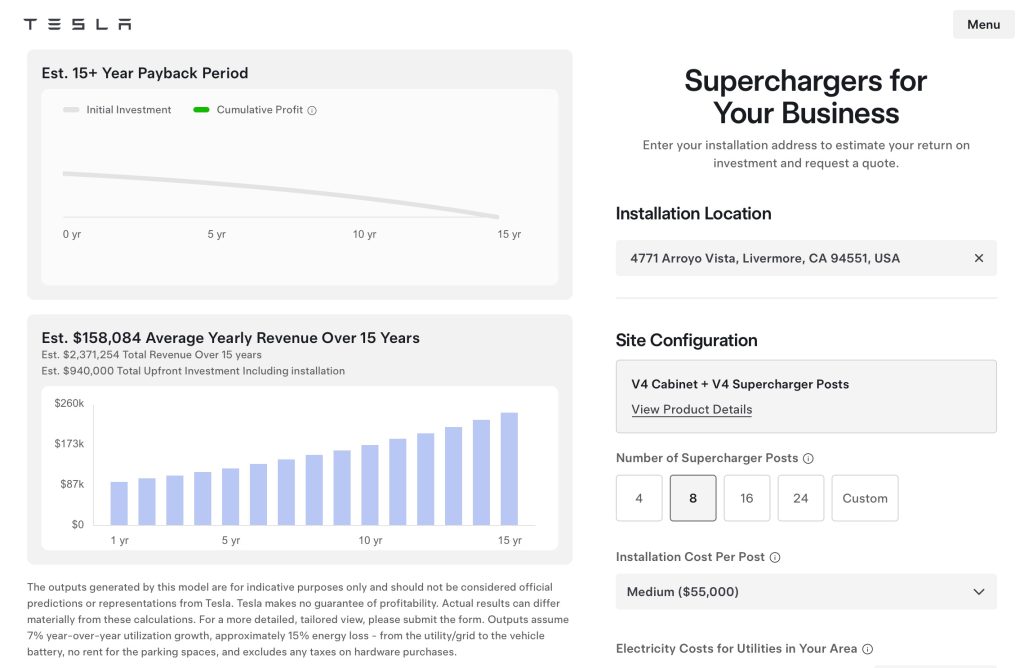

The new online calculator, announced by Tesla on Wednesday with the note that “simplicity and transparency” have been a problem in the industry, lets any business enter a U.S. address and get a real cost and revenue model. A standard 8-stall V4 Supercharger site runs approximately $500,000 in hardware and $55,000 per post for installation, bringing an all-in price just shy of $1 million. Tesla charges a flat $0.10 per kWh fee to cover software, billing, and network operations. Businesses set their own retail price and keep the margin above that fee.

Taking a look at Tesla’s Supercharger for Business online calculator, we can see that ROI is not uniform, and the gap between a strong location and a poor one can stretch the breakeven point by several years.

The biggest driver is foot traffic and how long people stay. A busy rest station, hotel, or outlet mall brings in repeat visitors who need to charge while they’re already stopped, pushing utilization numbers higher and shortening payback time.

Tesla Supercharger for Business ROI calculator

Local electricity rates matter just as much on the cost side. Markets like California carry some of the highest commercial electricity rates in the country, which eats into the margin between what a host pays per kWh and what they charge drivers. At the same time, dense urban areas with high EV adoption tend to support higher retail charging prices, which can offset that cost if demand is strong enough. Weather also plays a role. Cold climates reduce battery efficiency and increase charging frequency, but they can also suppress utilization in winter months if drivers avoid stopping in exposed outdoor locations. Suburban and rural sites face a different problem: lower baseline EV traffic, which means a site with cheaper power and lower operating costs can still take longer to pay back simply because the stalls sit idle more often. Tesla’s calculator uses real fleet data to pre-fill utilization estimates by ZIP code, so businesses can run their specific address against these variables rather than relying on averages.

The program has seen real adoption. Wawa, already the largest host of Tesla Superchargers with over 2,100 stalls across 223 locations, opened its first fully owned and branded site in Alachua, Florida earlier this year. Francis Energy of Oklahoma and the city of Alpharetta, Georgia have also deployed branded stations through the program, as Teslarati covered in January.

Tesla now exceeds 80,000 Supercharger stalls worldwide, and the calculator makes the economic case for accelerating that number through private investment rather than company-owned sites alone.

Investor's Corner

Tesla stock gets hit with shock move from Wall Street analysts

Despite Tesla not being an automotive company exclusively, the Wall Street firms and analysts covering its shares are widely dialed in on its performance regarding quarterly deliveries. While it holds some importance, Tesla, from an internal perspective, is more focused on end-to-end AI, Robotaxi, self-driving, and its Optimus robot.

Tesla price targets (NASDAQ: TSLA) have received several cuts over the past few days as Wall Street firms are adjusting their forecast for the company’s stock following a miss in quarterly delivery figures for the first quarter.

Despite Tesla not being an automotive company exclusively, the Wall Street firms and analysts covering its shares are widely dialed in on its performance regarding quarterly deliveries. While it holds some importance, Tesla, from an internal perspective, is more focused on end-to-end AI, Robotaxi, self-driving, and its Optimus robot.

In a notable shift underscoring mounting caution on Wall Street, three prominent investment banks slashed their price targets on Tesla Inc. shares over the past two weeks following the electric-vehicle giant’s disappointing first-quarter 2026 delivery numbers. The revisions highlight softening EV sales figures and, according to some, execution challenges.

Tesla delivered 358,023 vehicles in the January-to-March period, a 14 percent sequential decline and a miss versus consensus forecasts of roughly 365,000 to 370,000 units.

Production hit 408,000 vehicles, yet the delivery shortfall, paired with limited updates on autonomous-driving progress and new-model timelines, rattled investors. Shares fell about 8.7 percent since April 1.

Wall Street analysts are now adjusting their forecasts accordingly, as several firms have made adjustments to price targets.

Goldman Sachs

Goldman Sachs cut its target from $405 to $375 while maintaining a Hold rating. Analyst Mark Delaney pointed to soft EV sales trends and margin pressures.

Truist Financial followed on April 2, lowering its target from $438 to $400 (Hold unchanged), with analyst William Stein citing misses in both auto deliveries and energy-storage deployments, plus a lack of fresh details on AI initiatives and upcoming vehicles.

It is a strange drop if using AI initiatives and upcoming vehicles as a justification is the primary focus here. Tesla has one of the most optimistic outlooks in terms of AI, and CEO Elon Musk recently hinted that the company is developing something for the U.S. market that will be good for families.

Baird

Baird’s Ben Kallo made a very modest trim, reducing its target from $548 to $538, keeping and maintaining the ‘Outperform’ rating it holds on shares. Kallo said the price target adjustment was a prudent recalibration tied to near-term risks.

Truist

Truist analyst William Stein pointed to deliveries and energy storage missing expectations, and cut his price target to $400 from $438. He maintained the ‘Hold’ rating the firm held on the stock previously.

JPMorgan

Adding to the bearish tone on Monday, April 6, JPMorgan’s Ryan Brinkman reiterated an Underweight (Sell) rating and $145 price target, implying roughly 60 percent downside from recent levels.

Brinkman highlighted a “record surge in unsold vehicles” that adds to free-cash-flow woes, with inventory swelling to an estimated 164,000 units.

Tesla’s comfort level taking risks makes the stock a ‘must own,’ firm says

He lowered his Q1 2026 EPS estimate to $0.30 from $0.43 and full-year 2026 EPS to $1.80 from $2.00, both below consensus. Brinkman noted that expectations for Tesla’s performance have “collapsed” across financial and operating metrics through the end of the decade, yet the stock has risen 50 percent, and average price targets have increased 32 percent.

This disconnect, he argued, prices in an unrealistic sharp pivot to stronger results beyond the decade, while near-term realities remain materially weaker.

He advised investors to approach TSLA shares with a “high degree of caution,” citing elevated execution risk, competition, and valuation concerns in lower-price, higher-volume segments.

The revisions have pulled the overall consensus lower. Aggregators show the average 12-month price target now ranging from approximately $394 to $416 across roughly 32 analysts, with a prevailing Hold rating and a mixed split of Buy, Hold, and Sell recommendations.

Brinkman’s $145 target stands as a notable outlier on the bearish side.

Not Everyone Has Turned Bearish on Tesla Shares

Not all firms turned more pessimistic. Wedbush Securities held its bullish $600 target, stressing that AI and full self-driving technology represent the core value drivers, with current delivery softness viewed as temporary.

These moves reflect a broader Wall Street recalibration: near-term EV demand faces pressure from high interest rates, intensifying competition, especially from lower-cost Chinese rivals, and slower adoption.

At the same time, many analysts continue to see Tesla’s technology leadership in software-defined vehicles, autonomy, robotaxis, and energy storage as pathways to outsized long-term gains once macro conditions ease and new models launch.

With Tesla’s first-quarter earnings report due later this month, upcoming details on cost discipline, Cybertruck ramp-up, and AI roadmaps will likely shape whether these target adjustments prove prescient or overly cautious. Investors remain divided between immediate delivery realities and the company’s ambitious vision.

Tesla shares are trading at $348.82 at the time of publishing.

Tesla launches 200mph Model S “Gold” Signature in invite-only purchase

Tesla FSD in Europe vs. US: It’s not what you think