Investor's Corner

TSLA Extended Hours Action after Q1 Report & Conference Call

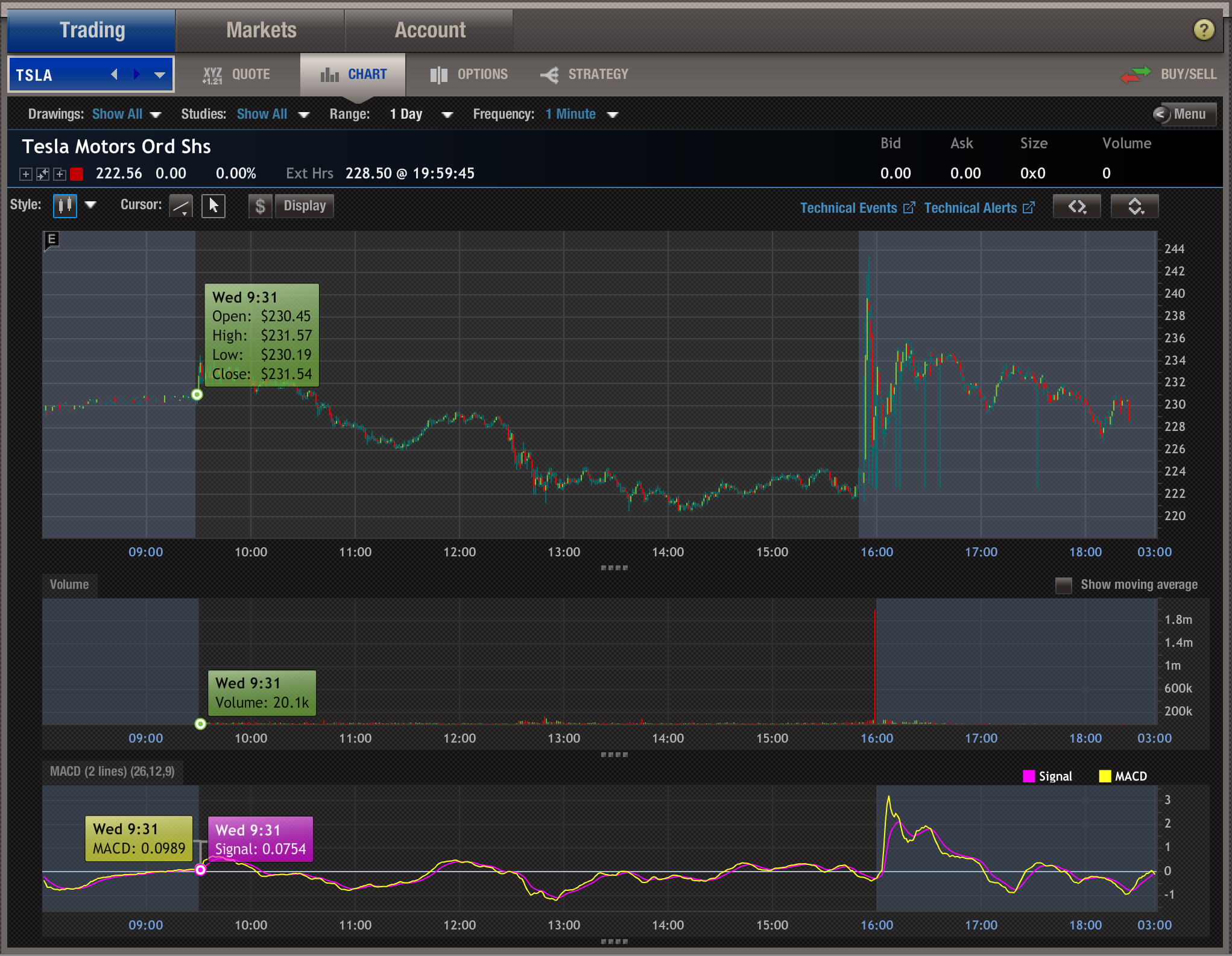

TSLA action on the day of the Q1 Report was effectively a wash: TSLA stock opened at 230.29 and closed the regular trading session down -4.20% at $222.56, but gained almost all of it back during “extended hours”, closing the day at 228.50. Right after the quarterly results were released, it traded as high as $243.43.

Source: OptionsHouse Trading Application

Obviously traders and brokers liked both the results and the subsequent answers that were given in the conference call.

What items did the traders actually like?

– Beating analysts’ expectations for earnings by 3 cents.

– Revenue of $1.15B, with sales of $1.6B. Net loss of $ -57c a share. A beat on the loss, a meet on sales.

– A decrease in capital expenditures by 47% from Q4 2015, with spending decreases at both Fremont factory and Gigafactory.

– A much more ambitious timeline of delivery of vehicles: 500,0000 vehicles in 2018 (two years ahead of the previous projections), and 1 Million vehicles in 2020.

– Adjusted plans for the Gigafactory to support the new timeline targets in 2018.

-

-

– A mix of 100-150K Model S and X, plus 300-400K Model 3, for 2018 vehicle deliveries.

– A July 1st, 2017 deadline for suppliers of Model 3 parts.

– A combination of capital & debt to support the more ambitious timeline.

– Projections of 20,000 vehicles delivered in Q2, and 50,000 in the rest of the year, maintaining the 80,000 to 90,000 vehicles projection for the year 2016.

– Brushing off the loss of 2 top executives for production and manufacturing, because Tesla is the place top talent in manufacturing would want to be, since at Tesla “innovation in manufacturing is more important than innovation in design” (a subtle swipe at Apple).

Interestingly no new reservation numbers for Model 3 were given, as we stand at “almost 400,000” from a couple of weeks ago.

Will Tesla be able to deliver on the adjusted projections? History tells us probably no. But short-term, Elon & Co. delivered: the pessimism that was evident among brokers and traders before the report and conference call, pretty much evaporated. My expectation for Thursday’s market is an opening between 228 and 230.

-

After 6 sessions that brought the stock from $255 down 9% to $222, we may see momentum start going the other way up again.

Update

While TSLA, as expected, opened at 228.46, it quickly turned red and within an hour was done 4.5%. From the morning broker’s comments, not everybody is buying Elon’s rosy projections. You have now witnessed how “volatile” TSLA stock can be: it went from an after-hours peak of $243 to $212 in a span of a few trading hours, a 13% drop. Not a stock for the faint of heart.

In a new note to investors on Tuesday, Morgan Stanley analyst Andrew Percoco said that Tesla has one big financial question to answer for investors regarding its Robotaxi rollout, Full Self-Driving software, and Optimus.

Percoco said in the note that, for the most part, investors are still very positive about the direction the company is headed. However, there are some things the firm would like to see, and they have to do with financials.

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Tesla bulls are more than convinced that the company’s Full Self-Driving software is proof it can develop physical AI. Financially, however, there are still some questions, especially on elevated spending, which CEO Elon Musk said would occur as the company works to roll out Robotaxi faster and continue developing its Optimus robot.

The latter two are where Tesla will have to prove progress to investors, as Percoco writes that both projects “will require clearer evidence that Robotaxi is scaling and more tangible Optimus proof points to support the ROI on elevated capex.”

Percoco said the second quarter earnings call did not change his long-term thesis of where Tesla is positioned in the AI race, which is out in front. However, there are concerns that weaker gross margins and higher R&D spend will stress financials, and that has “sharpened our (and investors’) focus on measurable progress across Robotaxi and Optimus.”

Additionally, Robotaxi still needs to be proven with more operation in existing cities while maintaining safety but improving how many rides it gives in any given time, he said. For Optimus, Percoco wrote that he is “still looking for evidence beyond commentary around SOP.”

-

Morgan Stanley put Percoco in charge of covering Tesla after long-time analyst Adam Jonas transitioned to the automotive side.

Currently, Morgan Stanley has a $415 price target on Tesla and a ‘Hold’ rating on the stock. It is trading at around $330 at the time of publication, which was 2:30 P.M. on the East Coast.

SpaceX’s massive investment in AI will make it a big winner, Argus Research said after the company’s successful earnings call last week.

The firm also upgraded shares to a Buy from Hold and set a $160 price target.

SpaceX (NASDAQ: SPCX) is currently recovering from its heavy AI infrastructure investments, as it spent nearly $16 billion in Q2 alone. The company did this primarily by monetizing high-demand GPU compute capacity at a much faster pace than traditional data center economics would suggest.

Company CFO Bret Johnsen said that SpaceX would be able to pay back anything on new deployments within a year.

There are plenty of ways the company can do this:

Leasing excess compute capacity through contracts

SpaceX has already built Colossus and Colossus II, largely for its own model training. However, much of that capacity is already rented out to third parties. It already has major deals with Anthropic, Google, and Reflection AI. These partnerships are adding billions per month to SpaceX’s spreadsheet.

-

High utilization driven by industry-wide scarcity

The demand for advanced AI training and inference capacity continues to exceed what is available for use. SpaceX can fill new racks quickly after they come online, so the capital deployed converts into revenue with minimal idle time.

Additionally, management and outside observers have described the new compute capital as behaving more like a cost-of-goods-sold than traditional multi-year capex, especially because of this rapid monetization pattern.

Capacity has already scaled from ~0.4 GW a year to 1.4 GW annually by the end of Q2. There are targets of more than 2 GW by year-end.

High incremental margins on the rental business once capacity is online

GPU cloud providers often operate at strong gross margins. SpaceX can monetize capacity that was already partially built or can be added efficiently. This means that incremental EBITDA margins on the rental revenue are usually high. This accelerates cash recovery relative to the gross capital outlay.

Parallel monetization of its own AI software and applications

Beyond pure infrastructure rental, SpaceX also generates revenue from Grok through subscriptions and usage, from X through ads, data, and other related services, enterprise APIs, and the planned integration of the Cursor coding tools acquisition.

These application layers ride on the same compute infrastructure and provide additional high-margin streams that could offset build-out costs. AI-segment revenue overall rose sharply to about $2.6 billion in Q2, according to Motley Fool. This was driven primarily by the infrastructure contracts, but the software side is also partially responsible.

Efficient, large-scale deployment and vertical integration advantages

SpaceX has emphasized the rapid construction of power and cooling infrastructure and favorable cost-per-megawatt economics relative to industry benchmarks in some disclosures.

-

Combined with its ability to scale capacity aggressively and the fact that many contracts start generating revenue within months of capacity coming online, the effective payback compresses dramatically compared with more conventional multi-year data-center projects.

SpaceX’s dominant near-term recovery path will turn the AI clusters into a hyperscale-style compute rental business for other leading AI companies while still using a portion for internal models.

Elon Musk

Another Tesla SpaceX merger prediction by ARK Invest has Elon Musk talking

Elon Musk again denies a Tesla China split as new SpaceX merger speculation resurfaces quickly.

Elon Musk restated that Tesla has no plans to separate its China business from the rest of the company, responding to a new round of merger speculation from ARK Invest.

On the firm’s “Brainstorm” podcast, Cathie Wood’s team, including chief futurist Brett Winton and research director Nick Grous, argued a Tesla and SpaceX combination remains likely, with an announcement possible before the end of the year even if the deal itself would not close that quickly. Winton called Tesla’s Shanghai operations a “small ish wrinkle” for a merger rather than a real obstacle, since SpaceX’s national security work with the U.S. government sits uneasily next to Tesla’s manufacturing base in China.

Musk pushed back on the framing directly. “China is awesome. I strongly encourage people to visit,” he wrote on X. He also repeated language he first used in late July, when the Wall Street Journal reported that Tesla executives had been told to prepare for a possible spinoff, sale, or closure of the China business ahead of a SpaceX tie up. Musk called that report “absurdly fake news” at the time, adding that a separation had “never even come up in a discussion ever,” a line he echoed again this week.

The repeated denial has not settled the underlying question, because Shanghai’s role in Tesla’s business is exactly what makes a merger complicated. Gigafactory Shanghai still ships more than half of Tesla’s global deliveries and functions as the company’s main export hub for Europe and Asia. Teslarati previously reported on Musk’s initial denial, and the merger conversation itself has been building since SpaceX’s IPO gave it public shares to use as acquisition currency.

Wedbush’s Dan Ives has pegged the odds of a Tesla SpaceX merger at 80 to 90 percent by early 2027, and ARK’s prediction of a year end announcement adds another data point to that timeline, even as Musk keeps rejecting the specific mechanics reporters have described. Neither position rules out the other. Musk can deny a China spinoff was ever discussed while analysts still expect some form of combination to move forward, since ARK and Ives are both describing convergence at the corporate level, not necessarily the internal restructuring the Journal described in July.

For now, Tesla’s China business remains intact, and Musk’s comments this week make clear he has no interest in publicly walking that position back, no matter how often the merger question resurfaces.

-

Tesla has one big financial question to answer for investors: Morgan Stanley

SpaceX AI investment gamble will make it a big winner, firm says