Investor's Corner

Tesla bull ARK loads up on TSLA shares amid stock slide

Tesla (NASDAQ: TSLA) bull ARK Invest, headed by CEO and CIO Cathie Wood, loaded up on shares of the electric automaker’s stock as it has slid to lower prices over the past few weeks.

According to ARK’s Daily Trade Information, the fund bought 19,272 shares of Tesla, adding onto its massive holdings of the electric automaker’s shares. After the purchase on Friday, ARK now holds 3,566,628 shares of Tesla stock, which makes up 9.99% of its total portfolio. Square Inc. is ARK’s second-largest holding, with 6.28% of the portfolio being made up of the financial company.

ARK’s Tesla holdings are worth $2,132,665,212.60, according to the documents released on Friday.

The purchase of 19,272 additional shares supplements the addition of 130,000 shares in mid-February that were added to several different ARK ETFs. The ARK Innovation ETF bought 89,447 TSLA shares, while the ARK Next Generation Internet ETF added 29,508 Tesla stocks, and the ARK Autonomous Technology and Robotics ETF added 13,173 shares in February.

ARK is one of Tesla’s biggest bulls on Wall Street, holding tremendously high expectations for the electric automaker’s outlook over the next nine years. By 2030, ARK believes that Tesla’s Robotaxi fleet could generate more than $1 trillion in operating revenue, evidently remaining bullish on the automaker despite a recent slide in stock price.

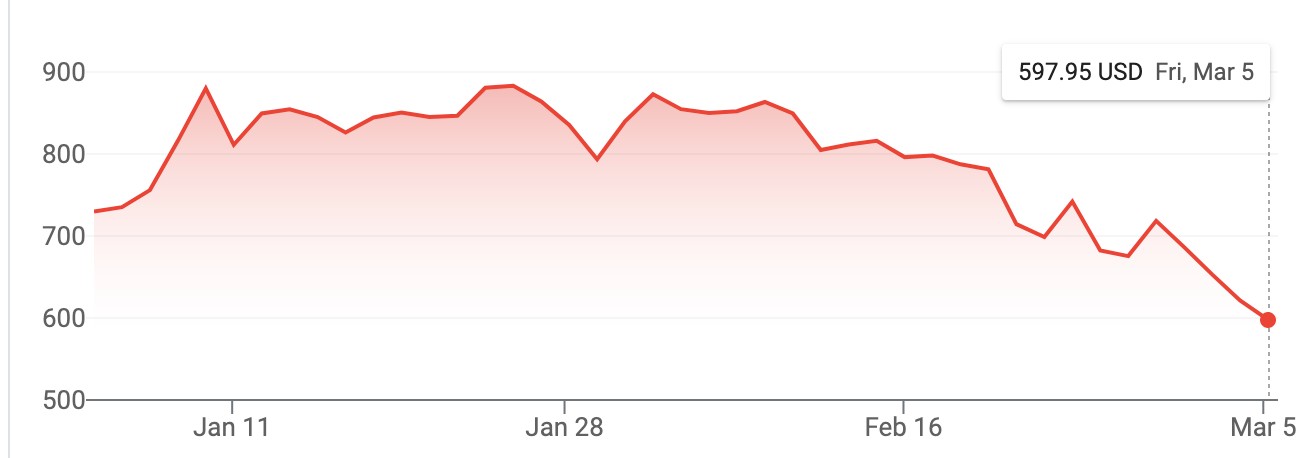

Tesla is down 30.75% over the past month and down 18% on the year. The stock currently sits at $597.95, closing on Friday down 3.78% or $23.49.

Tesla’s 2021 Stock Graph (Google)

After surging to prices as high as $880.02 in January, the stock remained relatively consistent in price until February 8th, when the price began to fall. Some analysts attributed the fall to Tesla’s lack of delivery forecast after the Q4 2020 Earnings Call. While Tesla executives didn’t give a specific figure, they did indicate that they expect 50% growth in deliveries annually, with some years providing more expansion.

A statement during the company’s most recent Earnings Call said that Tesla expects “to achieve 50% average annual growth in vehicle deliveries. In some years, we may grow faster, which we expect to be the case in 2021.” Additionally, it is difficult to give a specific figure as Tesla is expecting both Giga Berlin and Giga Texas to be completed at some point this year. With both facilities moving along quickly in the construction process, there is no specific time frame when they will be completed, which could be why Tesla did not provide specific delivery goals for 2021.

Many believe this is a temporary setback for Tesla. With expanding demand for the company’s vehicles and its place as the EV leader, Tesla is primed to dominate an expanding sector in the coming years. Dan Ives of Wedbush believes Tesla’s path to victory ultimately lies in China, where competitors are firing on all cylinders to catch up with Elon Musk’s company.

Tesla stock pullback temporary, China demand paves way to $1T market cap, Wedbush says

Disclosure: Joey Klender is a TSLA Shareholder.

Tesla deliveries got a big boost in expectations from Wall Street firm Goldman Sachs, who believes the company will report some stronger-than-expected numbers when the second quarter comes to an end in the coming weeks.

Goldman Sachs has raised its vehicle delivery forecast for Tesla (NASDAQ: TSLA) in the second quarter of 2026, signaling growing confidence in the electric vehicle leader’s near-term momentum despite mixed market signals. Analyst Mark Delaney lifted the bank’s Q2 estimate to 420,000 units from a previous 405,000, surpassing the Visible Alpha consensus estimate of 400,000.

The upward revision stems from stronger-than-expected sales data across key regions. Europe stands out with projected year-over-year growth of 85-90 percent, driven by robust demand for Tesla’s Model Y and refreshed offerings. China posted high single-digit gains, while markets like South Korea and Australia also contributed positive momentum. These gains help offset mid-teens declines in U.S. deliveries through May, where broader EV market headwinds and competition persist.

Goldman extended its optimism to the full year, increasing its 2026 delivery projection to 1.73 million vehicles from 1.72 million. Longer-term forecasts remain unchanged, with 1.88 million units expected in 2027 and 1.96 million in 2028. The bank also nudged its 2026 earnings-per-share estimate higher to $1.35 from $1.30, reflecting anticipated margin benefits from higher volumes and operational efficiencies.

Despite these positive adjustments, Goldman maintained its Neutral rating and $375 price target on Tesla shares. At current trading levels near $411, the stock sits about 8-9 percent above the target, highlighting ongoing valuation concerns even as delivery momentum builds. Tesla’s Q1 2026 deliveries totaled 358,023 units, setting a baseline for recovery expectations in the current period.

This update arrives as Tesla prepares to report official Q2 figures shortly after June 30. Investors and analysts will closely watch not only headline delivery numbers but also regional breakdowns, average selling prices, and progress on energy storage deployments and autonomous technology initiatives.

The move by Goldman Sachs underscores a broader narrative for Tesla: while legacy auto markets face softening demand and tariff uncertainties, Tesla’s global footprint and product pipeline provide resilience. Europe’s surge reflects pent-up demand and policy support for EVs, while China’s steady growth highlights Tesla’s competitive positioning against local rivals.

Tesla still has its work cut out for it, including U.S. price sensitivity and intensifying competition. Yet Goldman’s revision adds to a series of analyst notes suggesting Q2 could mark a turning point. As Tesla pushes toward higher production rates at facilities in Fremont, Shanghai, and Berlin, sustained execution will be key to validating these higher forecasts.

We have said numerous times that deliveries are becoming a less important metric in the grand scheme of things, as AI truly takes precedence in the company’s thesis.

For Tesla bulls, the Goldman note reinforces faith in underlying demand trends. For skeptics, the unchanged rating serves as a reminder that delivery beats alone may not immediately resolve valuation debates in a high-interest-rate environment. Tesla’s stock reaction will likely hinge on the official numbers and management commentary in the coming weeks.

Renowned investor Ron Baron, founder and CEO of Baron Capital, has once again demonstrated his unwavering faith in Elon Musk’s ventures.

Just after SpaceX’s record-breaking IPO, Baron announced he purchased an additional $1 billion in SpaceX (NASDAQ: SPCX) shares. This move pushes Baron Capital’s total holdings in the company to a staggering $25 billion in market value, underscoring one of the most successful private-to-public investment stories in recent history.

Baron’s relationship with SpaceX dates back to 2017, when his firm began investing approximately $1.75–2 billion through secondary markets and employee tender offers at valuations around $20–22 billion.

By the time of the IPO, which valued SpaceX at over $2 trillion with shares closing near $161, those early stakes had generated more than $13 billion in unrealized gains. Post-IPO, Baron’s position ballooned further, reflecting the company’s meteoric rise driven by reusable rocketry, Starlink’s global satellite internet constellation, Starshield defense applications, and ambitious plans for orbital infrastructure.

In a recent interview, Baron articulated his bullish outlook with characteristic enthusiasm.

Ron Baron said today that he bought $1 billion of @SpaceX IPO shares last Friday, and said that all of Baron Capital’s $SPCX holdings are now worth $25 billion.

“I think we’re going to make hundreds of billions of dollars; If you read the prospectus, you realize what they… pic.twitter.com/U8F471KtJS

— Sawyer Merritt (@SawyerMerritt) June 15, 2026

“I think we’re going to make hundreds of billions of dollars,” he stated, emphasizing that SpaceX’s achievements in rocketry and satellite technology are “not possible for anyone else to accomplish.” He envisions the company as a cornerstone of humanity’s multi-planetary future, potentially reaching valuations of $10–30 trillion within 10–15 years.

Baron has repeatedly affirmed he has no plans to sell, viewing SpaceX as a “lifetime investment” alongside Tesla.

Tesla bull Ron Baron reveals $100M SpaceX investment, sees 3-5x return on TSLA

This conviction stems from SpaceX’s unparalleled execution. The company has revolutionized access to space with Falcon 9 reusability, deployed thousands of Starlink satellites, and is advancing Starship for Mars missions and point-to-point Earth transport.

Baron highlights emerging opportunities like space-based AI data centers and direct-to-cell satellite connectivity, positioning SpaceX at the forefront of a new space economy projected to generate trillions in value.

Critics may question the lofty projections amid high valuations and execution risks, but Baron’s track record speaks volumes. His Tesla holdings, initiated in the mid-2010s, have also delivered outsized returns. As one of the largest institutional holders of SpaceX pre-IPO, Baron Capital’s funds, such as Baron Partners, benefited immensely from valuation markups.

Baron’s $1 billion IPO purchase signals deep confidence in SpaceX’s post-IPO trajectory. In an era of short-term market noise, his strategy exemplifies patient capital: backing visionary leadership and transformative technology.

For investors watching the space sector, it serves as a powerful endorsement that the final frontier may indeed yield the next great wealth-creation engine. As Baron puts it, SpaceX isn’t just building rockets—it’s trying to “save humanity” by expanding our horizons beyond Earth.

Elon Musk

SpaceX (SPCX) IPO is live today at $135: Here’s exactly what you need to know

SpaceX priced its historic IPO at $135 per share today, raising a record $75 billion.

SpaceX officially priced its initial public offering at $135 per share, offering 555,555,555 shares of Class A common stock and raising $75 billion in what is the largest IPO in stock market history. Shares are set to begin trading on the Nasdaq Global Select Market on Friday, June 12, under the ticker symbol SPCX. The previous record holder was Saudi Aramco’s 2019 offering at $29 billion, followed by Alibaba’s $22 billion offering in 2014.

At $135 per share and roughly 555.6 million shares, the implied valuation sits near $1.75 trillion, which would make SpaceX roughly the seventh largest company in the United States, just above Tesla’s current market cap. Regular investors can request shares at the IPO price through Robinhood, Fidelity, Charles Schwab, SoFi, and E*TRADE, though the deal is heavily oversubscribed and most retail allocations will be partial or unfilled. Once trading opens June 12, anyone with a brokerage account can buy SPCX on the open market.

SpaceX’s amended S-1 is sparking a major Tesla merger conversation

The valuation is anchored primarily by Starlink. Starlink crossed 10 million subscribers as of February 2026 and is adding 750,000 to 1.5 million new users per month, with the connectivity segment already posting a $1.19 billion profit last quarter. The offering also bundles in xAI following SpaceX’s all-stock merger earlier this year, adding Grok and the Colossus supercomputer to the investment thesis. As Teslarati reported, Starlink ended 2025 with $10 billion in revenue, a figure analysts project could reach $24 billion by end of 2026.

Wedbush analyst Dan Ives has been vocal in his support. “I think the time is right,” Ives said, adding that the offering expands the Elon Musk ecosystem rather than competing with Tesla. An average 12-month price target of $165 per share represents roughly 22% upside from the IPO price. Not everyone agrees – Motley Fool noted xAI is spending $1 billion per month playing catch-up to OpenAI and Anthropic.

Musk founded SpaceX in 2002 with a single stated purpose. “Elon founded SpaceX with a goal to change humanity, to make us a multi-planet species,” CFO Bret Johnsen said in the company’s retail roadshow video this week. Musk himself has been more direct: “We are building the systems and technologies necessary to provide global connectivity on Earth and beyond, to understand the true nature of the universe, and to extend the light of consciousness to the stars.”

Tesla patent aims to improve common on-road complaint

Tesla Cybercab gets huge nod of support from Texas DOT official