Tesla (NASDAQ:TSLA) is poised to release its Q4 and FY 2023 Update Letter later today. With this in mind, Tesla VP of Investor Relations Martin Viecha has shared a unified consensus for the company’s fourth quarter 2023 results, as well as expectations for key metrics in full year 2024.

As noted in a document shared by the Tesla executive, the Q4 2023 consensus includes estimates from 28 analysts that are covering the electric vehicle maker. These include Baird, Barclays, Bernstein, BNP, Bank of America, CGF, Citi, Cowen, Daiwa, Deutsche Bank, Evercore ISI, Goldman Sachs, Guggenheim, HSBC, JPM, Jefferies, Mizuho, Morgan Stanley, Needham, New Street Research, OpCo, Piper Sandler, RBC, Tudor, Truist, UBS, Wells Fargo, and Wolfe.

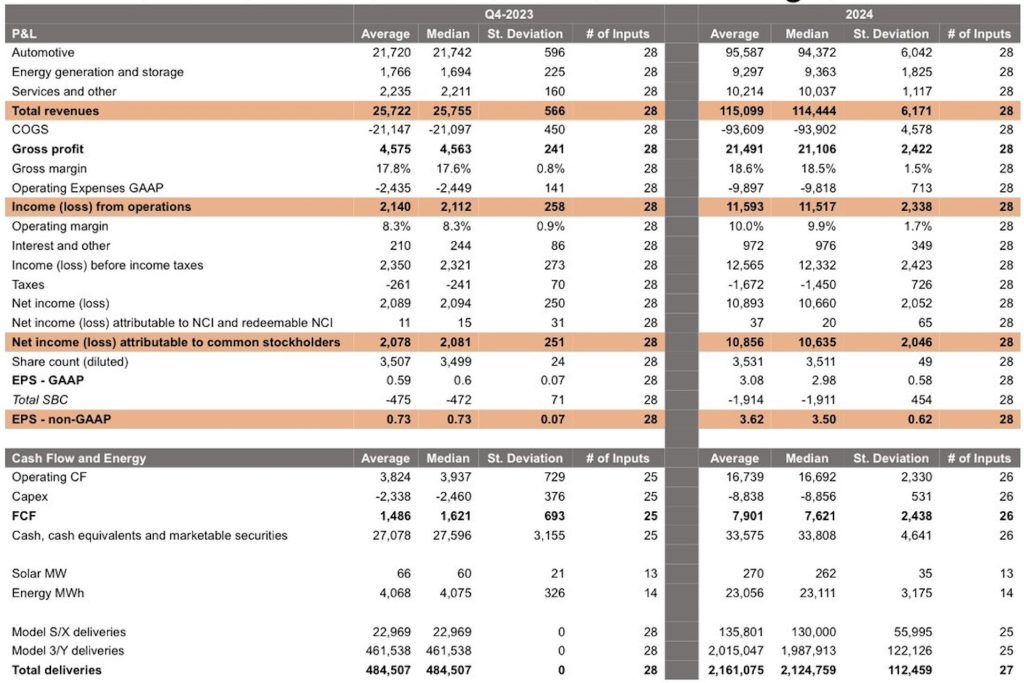

As per Tesla’s unified consensus for Q4, analysts are expecting the electric vehicle maker to post non-GAAP earnings per share of $0.73. Analysts are also expecting total revenues of $25.7 billion, as well as automotive revenues of $21.7 billion. Gross profit as per Tesla’s unified consensus is expected at $4.5 billion, and gross margin is estimated to be 17.8%.

For full year 2024, analysts are expecting Tesla to post non-GAAP earnings per share of $3.62. Analysts are also expecting total revenues of $115.1 billion, as well as automotive revenues of $95.5 billion. FY 2024 gross profit as per Tesla’s unified consensus is expected at $21.5 billion, and gross margin is estimated to be 18.6%. The analysts’ unified consensus for Tesla’s full year 2024 vehicle deliveries is also listed at 2,161,075 units.

For context, Tesla’s vehicle deliveries were 484,507 units in the fourth quarter, including 461,538 Model 3 and Model Y, and 22,969 Model S and Model X.

Here is the $TSLA IR-compiled sell-side survey of 4Q ests ($.73 Adj EPS) and FY’24 (delivs 2,161K, Adj EPS $3.62). 4Q auto gross margin ex-RC (WS 16.7%E vs 3Q 16.3%) and the FY’24 deliveries guide are the two key metrics to watch, and any comments about FY’24 auto gross margins… pic.twitter.com/AqhGxB2Wgo— Gary Black (@garyblack00) January 23, 2024

Wall Street veteran and The Future Fund LLC Managing Partner Gary Black, a Tesla bull, noted that metrics to watch for Q4 2023 would be the electric vehicle maker’s auto gross margins excluding regulatory credits, which Wall Street expects to be 16.7%, as well as the the company’s full year delivery estimate for 2024. Black also noted that any comments about auto gross margins excluding regulatory credits for FY 2024 would be pivotal information.

“4Q auto gross margin ex-RC (WS 16.7%E vs 3Q 16.3%) and the FY’24 deliveries guide are the two key metrics to watch, and any comments about FY’24 auto gross margins ex-RC (WS 17.8%E). TSLA mgmt has not surveyed analysts on auto gross margins in recent quarters in favor of the broader but less useful consolidated operating margin (WS 8.3%E),” Black wrote on X.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

-

-

-

-

Elon Musk’s space exploration company, SpaceX (NASDAQ: SPCX), is set to report its earnings for the second quarter today in what will be its first-ever earnings call since going public in July.

SpaceX is trading down roughly 25 percent from its IPO. These early stock signals are usually a bit tumultuous, and considering this is the first company actively launching rockets that is available on the stock exchange, investors might have a tendency to be a bit skittish.

However, there are going to be some details that investors will hear for the first time today on the earnings call. Here’s what to look for:

Wall Street Expectations

Revenue is expected to fall somewhere around $6.8 billion, and will be heavily driven by Starlink, which is SpaceX’s widely popular satellite internet platform that has been adopted by numerous airlines, cruise ships, and other maritime operations. It is also available for consumers at home or in their cars.

Earnings Per Share (EPS) expectations fall at a net loss of $0.23 per share. Wall Street sees this as a total net loss of roughly $1.9 billion.

EBITDA is expected to come in between $2 billion and $2.1 billion.

What Investors Want to Know

Tesla uses the Say platform to help work with both retail and institutional investors to answer relevant and quality questions that address concerns or questions that they might have.

However, SpaceX is doing things differently, as the company launched its own Investor Relations website where these questions are being fielded. Just like the Tesla questions, they seem to be less focused on the operational tasks and overall progress of the company, and more novelty.

Here are the top five:

- Has the team thought about what possibilities there are with your mascot Asteroid? Whether it’s starting additional foundations for kids in its name, helping kids learn about space, etc. Kids are our future, and Asteroid would be a fun and easy way to help.

- Baby Asteroid is already making a difference through charity around the world. Could SpaceX take it even further with programs that inspire kids to explore space?

- SpaceX has some legendary vehicle names. Would you ever allow the public to name a Starship, even knowing there is a 99% chance it becomes Shipy McShipface?

- When can we expect to see more footage of the Human Landing System?

- Will Asteroid (your mascot) go to Mars?

SpaceX will report its earnings today, August 4, at 4:30 P.M. EDT.

SpaceX will report second quarter results after the market closes on Tuesday, August 4, marking the first time the company has opened its books to the public since its record IPO in June. Management will host a live audio only webcast at 4:30 p.m. ET, streamed on X, with no dial in option.

The debut carries more weight than a typical first quarter as a public company. Two trading days after the release, on August 6, the first tranche of SpaceX’s lockup expires, freeing roughly 911.5 million insider and employee shares, worth well over $100 billion at current prices and the largest such release in Wall Street history. A second, larger tranche tied to the stock trading 30 percent above its $135 IPO price never triggered, since shares have spent most of July trading below that price.

Wall Street’s models point to revenue near $6.9 billion for the quarter, up sharply from the $4.69 billion SpaceX reported in the first quarter, with a narrower per share loss than the $1.27 posted three months earlier, according to estimates compiled by Motley Fool. Those numbers will be the first look at how SpaceX’s three segments, Starlink, launch and AI, are performing independently.

SpaceX scores another massive Pentagon deal to support military satellites

Investors heading into the call have a specific list of questions. How many net new Starlink subscribers did SpaceX add after ending March with 10.3 million, and is average revenue per user holding up as the service expands into lower income markets. How much of the AI segment’s revenue reflects contract signings with Anthropic, Google and Reflection AI this year, deals that combined could annualize to nearly $28 billion if fully ramped. Whether capital expenditures, which nearly doubled in the AI segment alone between 2024 and 2025, are still accelerating or starting to plateau. And whether management offers any forward guidance at all, something SpaceX has never done publicly.

The report will also land days after Elon Musk publicly denied a Wall Street Journal report describing internal planning to separate Tesla’s China business ahead of a potential Tesla-SpaceX merger. Whether Musk or SpaceX executives address that speculation on the call, even indirectly, maybe something investors will be listening for on Tuesday.

As Teslarati reported after Musk’s own warning to short sellers last week, the CEO has made clear he expects skeptics to be proven wrong over time. Tuesday will be the first chance for the numbers themselves to make that case.

Elon Musk

Tesla AI boss reveals how big Optimus is going to get

Tesla’s Optimus chief corrected himself on X, confirming a staggering 10 million robot production target.

![Tesla Optimus Gen 3 [Credit: Tesla]](https://www.teslarati.com/wp-content/uploads/2026/03/tesla-optimus-gen3-diner.jpg)

Tesla’s Optimus program has a new number attached to it, after Ashok Elluswamy, the executive who has run the humanoid robot program since June 2025, posted a three word correction on X Thursday, “Correction, 10 million robots.”

The line clarifies the long term annual capacity Tesla is building toward its planned second Optimus production line at Gigafactory Texas, a figure Musk has cited repeatedly since last year’s shareholder meeting.

The scale is worth noting, because ten million robots a year would mean Tesla building more units annually than most countries sell in new cars. Tesla has framed this as a second line, not the first. The buildout is happening in two phases: a roughly one million unit per year line inside Tesla’s Fremont factory, installed on the floor space vacated when Model S and Model X production ended earlier this year, and a much larger dedicated facility under construction at Giga Texas that broke ground on its first steel structure in May. That Texas facility is the one Elluswamy’s correction refers to, and is expected to reach volume production sometime in 2027.

Correction, 10 million robots https://t.co/0z4nyQNTzp

— Ashok Elluswamy (@aelluswamy) July 30, 2026

Tesla Optimus project fires up as Musk sees production line progress

Elluswamy took over Optimus from Milan Kovac last summer and has spent the months since talking up the program’s trajectory. Elon Musk has also floated the ten million figure at Tesla’s 2025 shareholder meeting.

Ending Model S and Model X production to make room for the first Optimus line was one of the more consequential manufacturing decisions in the company’s recent history, retiring two flagship vehicles in favor of a robot that has yet to enter mass production. Musk has previously estimated per unit production costs at $20,000 to $25,000 once Tesla reaches a million units a year, though he hasn’t said what that cost looks like at ten times the volume.

SpaceX to report first-ever earnings today: here’s what to expect

Tesla Full Self-Driving insurance program with heavy discount expands