News

SpaceX’s ultimate ace in the hole is its Starlink satellite internet business

In a 2018 report on the current state of the satellite industry, the rationale behind SpaceX’s decision to expand its business into the construction and operation of a large satellite network – known as Starlink – was brought into sharp contrast, demonstrating just how tiny the market for orbital launches is compared with the markets those same launches create.

First and foremost, it must be acknowledged that SpaceX’s incredible strides in launch vehicles over the last decade or so have been explicitly focused on lowering the cost of access to orbit, the consequences of which basic economics suggests should be a subsequent growth in demand for orbital access. If a sought-after good is somehow sold for less, one would expect that more people would be able and willing to buy it. The launch market is similar, but also very different in the sense that simply reaching orbit has almost no inherent value on its own – what makes it valuable are the payloads, satellites, spacecraft, and humans that are delivered there.

-

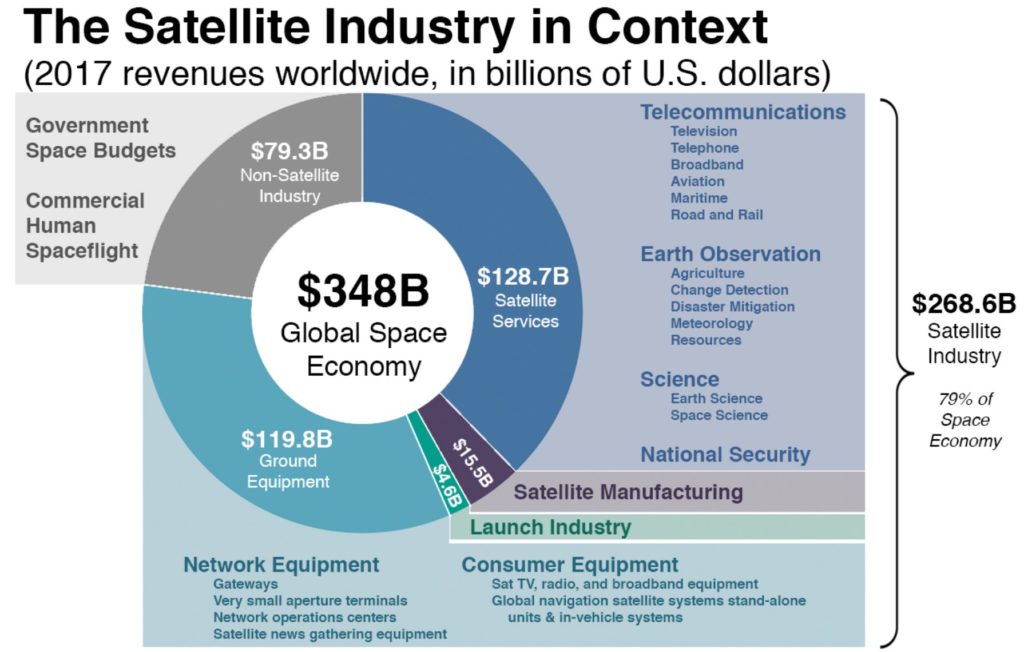

- An overview of space industry in 2017, produced by Bryce Space & Technology for the 2018 State of Satellite Industry Report.

-

- SpaceX’s first two Starlink prototype satellites are pictured here before their inaugural Feb. 2018 launch, showing off a utilitarian design. (SpaceX)

As a consequence, if the cost of access to orbit plummets (as SpaceX hopes to do with reusability) but the cost of the cargo still being placed there does not, there would essentially be no reason at all for demand for launches to increase. For there to be more demand for cheaper launches, the cost of the satellites that predominately fuel the launch market also needs to decrease.

One of the first two prototype Starlink satellites separates from Falcon 9’s upper stage, March 2018. (SpaceX)

Enter Starlink, SpaceX’s internal effort to develop – nearly from scratch – its own highly reliable, cheap, and mass-producible satellite bus, as well as the vast majority of all the hardware and software required to build and operate a vast, orbiting broadband network. Add in comparable companies like OneWeb and an exploding landscape of companies focused on creating a new generation of miniaturized satellites, and the stage has truly begun to be set for a future where the cost of orbital payloads themselves wind up dropping just as dramatically as the cost of launching them.

Just by sheer numbers alone, stepping from launch vehicle and spacecraft production and operations into the satellite manufacturing, services, and connectivity industries is a no-brainer. Bluntly speaking, the market for rocket launches makes up barely more than one-sixtieth – less than 2% – of the entire commercial satellite industry, while services (telecommunications, Earth observation, science, etc.) and equipment (user terminals, GPS receivers, antennae, etc) account for more than 93%. Even the satellite manufacturing industry taken on its own is more than three times as large as the launch industry – $15.5b versus $4.6b in 2017.

In other words, even if SpaceX was to drop the cost of Falcon 9, Heavy, and BFR launches by a factor of 10 and the market for launches expanded exponentially as a result (say 50-100x), the market for launches would still be a tiny fraction of the stagnant, unchanged, unimproved satellite services and production industries. Put simply, there is scarcely any money to be made in rocket launches when compared with literally any other space-related industry.

-

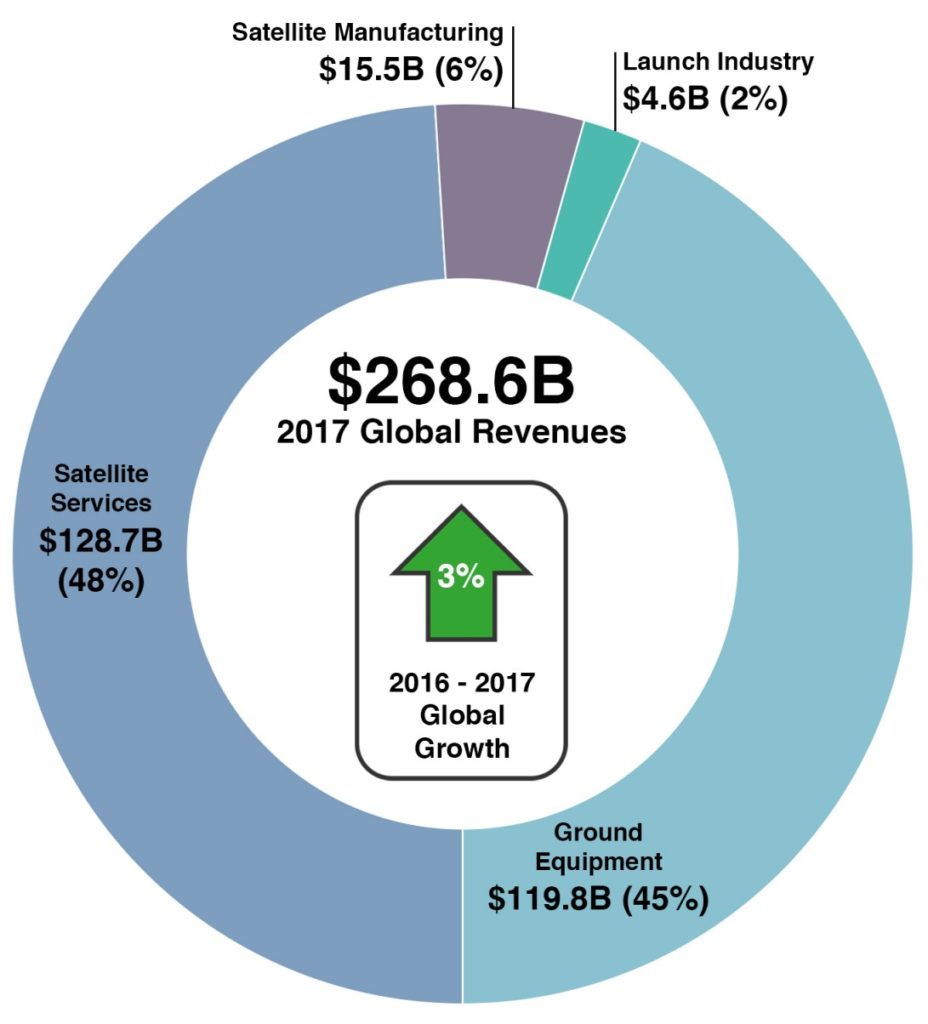

- An overview of just the commercial aspects of the satellite industry. (SIA)

-

- Falcon Heavy’s inaugural launch, February 2018. (Tom Cross)

While far from a done deal, Starlink is thus without a doubt the most promising established method for SpaceX to dramatically increase its profitable income, income which could thus be invested directly in launch vehicles, space resource utilization, sustainable interplanetary colonies, and more, all while potentially revolutionizing global freedom of connectivity.

Elon Musk said today on X that Teslas will start to learn your individual preferences. This is something that he seemed to hint toward earlier this month when he said parking was by far the biggest reason drivers intervene with Full Self-Driving.

Musk made the comment in response to notable Tesla influencer Whole Mars, who said that his vehicle will sometimes disobey the settings he has enabled for his car. He responded to the post, stating that “The car will start to remember your specific interventions and match each person’s individual preferences.”

The car will start to remember your specific interventions and match each person’s individual preferences

— Elon Musk (@elonmusk) July 18, 2026

This is something that could be perhaps one of the biggest ways Tesla could minimize or even work closer toward eliminating interventions altogether. While FSD does a lot of things really well, many people intervene a vast majority of the time not due to major or critical safety errors.

Instead, many take over because the car is doing something that they do not like as a preference; it might park in a parking spot that is not preferred by the driver, it might linger too long in the left lane on the highway (a personal favorite), or it could even take a route that the driver does not like.

These all lead to interventions, but they are not triggered by a major safety issue. Instead, it’s just preference.

READ OUR REVIEW OF TESLA’S LATEST FSD VERSION:

Tesla Full Self-Driving v14.3.5 Early Impressions: new features and early performance

If Teslas could start to learn the personal preferences of the person who owns them, interventions will truly begin to be less frequent. Some of this is already pretty evident, in my opinion. Teslas use a neural network to learn behaviors and accumulate data to improve performance.

For months now, we’ve tracked FSD’s performance at “Except Right Turn” stop signs, something that is very common in Pennsylvania, but many of our readers located in other parts of the U.S. have never heard of. FSD handles one Except Right Turn stop sign very well, one that I travel past frequently. Others that I do not navigate through as often do not have as confident a performance. It seems like the cars might already be doing this to an extent.

🚨 Tesla Full Self-Driving v14.3 proceeds through an Except Right Turn Stop Sign pic.twitter.com/YemRSlens7

— TESLARATI (@Teslarati) April 8, 2026

That example is also for something that is a street sign and not necessarily a driver preference; however, I still feel it is worth mentioning because it only handles that commonly passed Except Right Turn stop sign with true confidence. Others it still seems to struggle with.

This could be one of Tesla’s big moves toward full autonomy, and it could be a pathway to truly unsupervised driving. Every day, millions of cars on the road travel at a human driver’s personal preferences with no incident. Why can’t autonomous vehicles still cater to a passenger’s preferences while being autonomous? Tesla seems to have the idea that it would be possible.

Florida Governor Ron DeSantis has sharply criticized legacy media outlets for what he describes as selective and biased reporting on vehicle accidents involving Tesla. In a recent X post, DeSantis questioned why headlines routinely spotlight the Tesla brand in crash stories, even when human error is the clear cause, while similar incidents with other automakers often receive generic treatment.

A prime example is the June 19, 2026, fatal crash in Katy, Texas. A Tesla Model 3 driven by Michael Butler struck a brick home at high speed, killing 76-year-old Martha Avila inside. Initial reports and headlines prominently featured “Tesla crash” and referenced the driver’s claim that an automated driving-assistance system was engaged.

Many outlets quickly speculated that Full Self-Driving or Autopilot were the cause of the crash, immediately blaming the suites for the accident shortly after it happened.

However, Tesla responded shortly after the accident with vehicle data that showed Butler manually overrode the system by pressing the accelerator to 100 percent, reaching 73 MPH in a residential area, more than double the speed limit. The accelerator remained floored after impact.

Tesla finally clarifies fatal Texas crash, confirms driver manually overrode acceleration

The National Transportation Safety Board (NTSB) later confirmed these findings, and Butler now faces manslaughter charges. His phone searches also included queries like “Tesla FSD too timid,” suggesting he may have intervened aggressively. Despite this, many headlines continued to center Tesla’s technology rather than the driver’s actions.

DeSantis highlighted a Washington Post headline, which was labeled, “Newly released photo shows wreckage of Tesla crash that killed grandmother.”

Do legacy media outlets typically use headlines involving the make of a car in a crash or is that only for Tesla?

It would be one thing if the self-driving malfunctioned but the crash was purely human-induced.

Seems like these outlets want to associate Tesla with crashes as… pic.twitter.com/EmfyeYiuv6

— Ron DeSantis (@RonDeSantis) July 17, 2026

The subheadline noted the driver overrode assistance and floored the accelerator, yet the brand name dominated the framing. He asked whether legacy outlets typically name the make of a car in routine crashes or reserve that treatment for Tesla to push a narrative.

This pattern appears widespread. Crashes involving Ford, Chevrolet, or Toyota vehicles frequently appear as “pickup truck slams into home” or “fatal car crash kills pedestrian” without brand specifics, especially absent new technology angles.

High-profile Ford F-150 or Chevy Silverado incidents tied to large sales volumes often escape brand-callout scrutiny. In contrast, Tesla stories consistently lead with the manufacturer, amplifying perceptions of risk despite data showing strong overall safety performance:

🚨 Why do Tesla Owners get so defensive over the narrative of crashes involving Teslas? https://t.co/aX7ogtjTCR pic.twitter.com/KO4QWaLOKl

— TESLARATI (@Teslarati) June 24, 2026

Tesla’s own 2025 Impact Report indicates vehicles using FSD logged 0.19 major incidents per million miles, roughly eight times fewer than the U.S. average. Models like the Model Y also rank among the safest in IIHS and NHTSA testing for occupant protection. Critics argue disproportionate coverage ignores these statistics and driver behavior factors, such as younger or more aggressive Tesla owners in some studies.

DeSantis frames this as part of a broader political agenda against innovative American companies like Tesla. By consistently naming Tesla while downplaying others, media outlets risk eroding public trust and shaping perceptions detached from the evidence of human error in most cases.

As autonomous technology evolves across the industry, consistent and factual reporting will be essential to separate real safety concerns from narrative-driven coverage.

Tesla entered two new markets this week by advancing its presence in Latvia (Europe) and officially launching operations in Uruguay (South America), marking a rapid dual-continent expansion.

These moves underscore the company’s strategy to tap into emerging EV markets with supportive policies, renewable energy grids, and growing demand for sustainable transport.

Latvia: Strengthening the Baltic Footprint

In Latvia, Tesla has built on its earlier registration of Tesla Latvia SIA in late 2025 with recent steps toward full operations, including job postings for a service center and representation in Riga. This aligns with broader Baltic expansion following Lithuania’s model of pop-up stores and service centers.

Coming to Latvia https://t.co/XNkQQJ2O6a pic.twitter.com/yS9kpcNky1

— Tesla Europe, Middle East & Africa (@teslaeurope) July 17, 2026

EV penetration in Latvia stands at around 7 percent for BEVs in new passenger car registrations. 2025 data showed 1,602 BEVs out of about 22,500 total, or 7.1 percent, with combined plug-ins nearing 19 percent. Growth has been steady but below the European average, supported by government subsidies and infrastructure development. Tesla models like the Model 3 lead local EV registrations.

Vehicles for the Latvian market will likely be sourced from Gigafactory Berlin or Gigafactory Shanghai. Charging infrastructure is robust for the region as well, with over 400- 2,000 public points, with Tesla Superchargers in Riga, Jūrmala, and along Via Baltica routes offering up to 250 kW.

Uruguay: Third South American Country

Tesla teased its Uruguay arrival with “Estamos llegando,” or, “We are arriving,” on social media, followed by an official presentation scheduled for mid-July.

Hola Uruguay 🇺🇾

Nuestros Model 3 y Model Y están cada vez mas cerca! pic.twitter.com/FR41fsA7um

— Tesla Latinoamérica (@Tesla_LatAm) June 30, 2026

The company established Tesla Uruguay SAS, homologated Model 3 and Model Y (three versions each), and appointed local leadership. This makes Uruguay Tesla’s third official South American market after Chile and Colombia.

Uruguay boasts one of Latin America’s highest EV penetrations, with battery-electric vehicles exceeding 20 percent market share recently, driven by tax incentives, high fuel prices, and a nearly 95-100 percent renewable electricity grid. Hundreds of Teslas already operate via grey imports, but official sales bring warranties, service, and support.

Vehicles will be imported from Gigafactory Shanghai, enabling competitive pricing for Model 3 and Model Y. Charging plans include Supercharger development alongside existing infrastructure, leveraging the country’s green energy advantage for affordable operation.

Tesla Superchargers follow Model 3 and Model Y to South American country

Tesla’s Dual Continent Expansion

Tesla’s simultaneous push into Latvia and Uruguay demonstrates efficient scaling: prioritizing service and infrastructure first, then direct sales in high-potential niches. In Europe, it fills Baltic gaps; in Latin America, it counters Chinese dominance while leveraging renewables.

This dual move signals Tesla’s ambition to accelerate global EV adoption amid varying regional paces. By addressing local needs, like subsidies in Latvia or incentives and green grids in Uruguay, Tesla not only boosts volumes but advances its mission of sustainable energy.

For investors and consumers, it highlights resilience and opportunity in diverse markets, potentially paving the way for further growth in underserved regions. With strong fundamentals in both, these entries could yield long-term gains as EV transitions mature worldwide.

Elon Musk says your Tesla will start to learn your individual preferences

Ron DeSantis calls out media bias in Tesla crash coverage