Investor's Corner

Elon Musk closes in on $11B options payout amid Tesla’s 7th consecutive profitable quarter

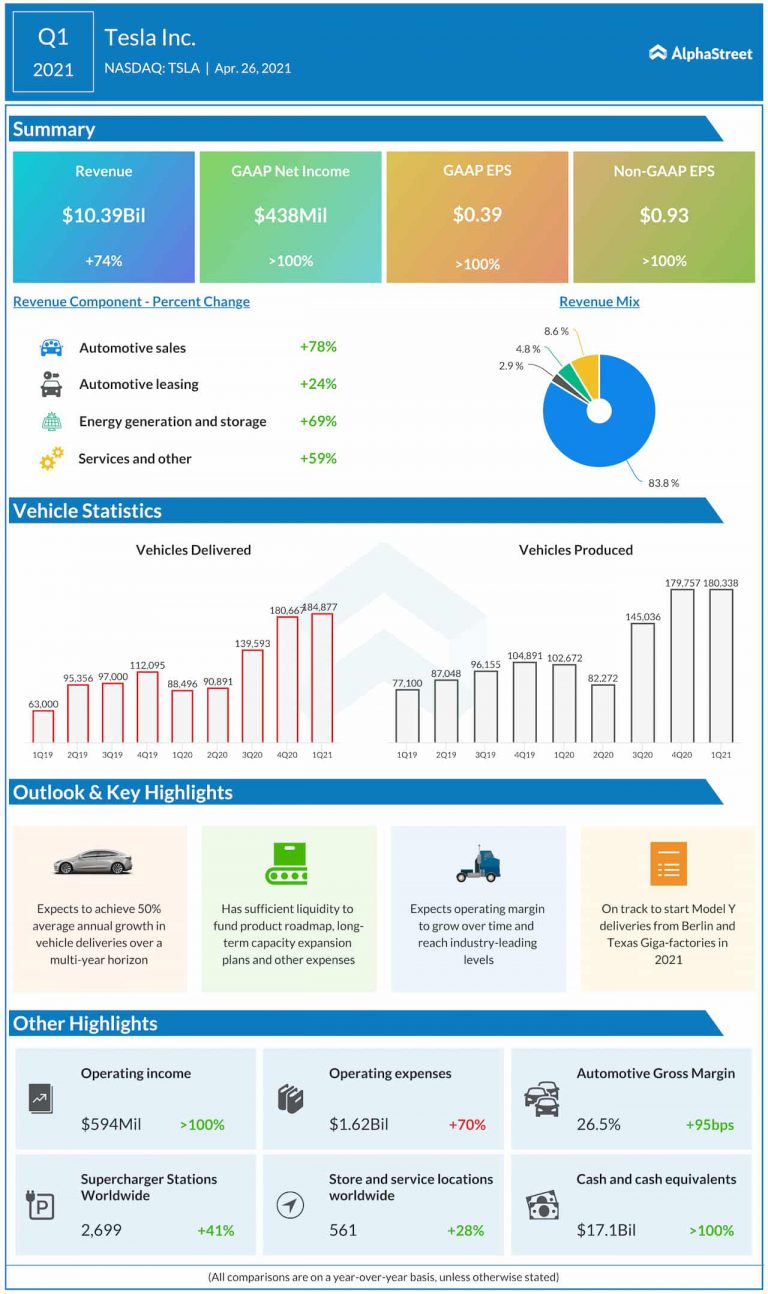

Tesla’s first quarter of 2021 would be one for the books, with the company beating Wall Street’s expectations for Q1 revenue and profit, boosted by record deliveries, some robust demand for its locally-produced vehicles in China, and some healthy environmental credit sales. Thanks to these blockbuster numbers, Tesla has now sustained its profitability for seven consecutive quarters.

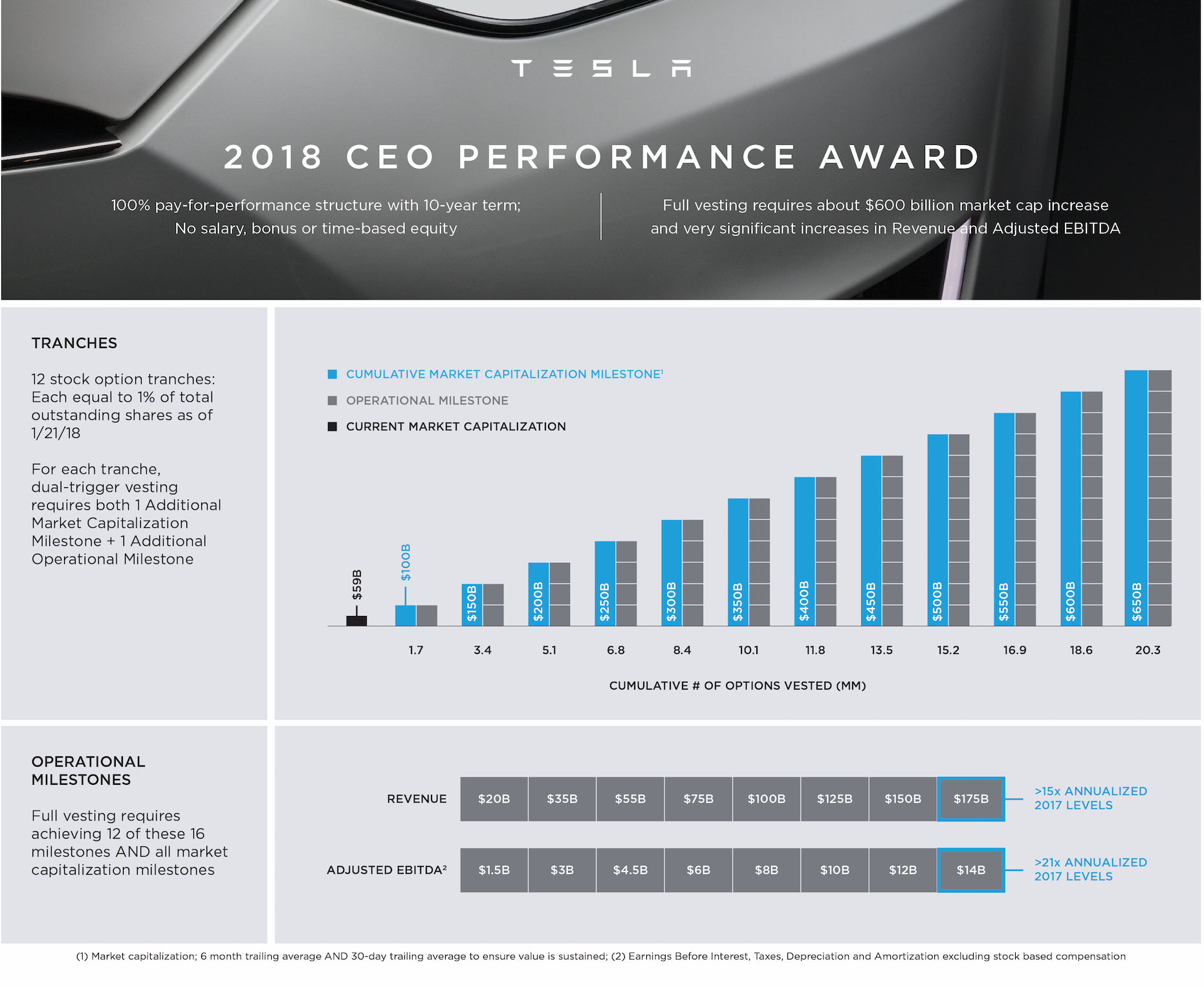

With these milestones in mind, Tesla CEO Elon Musk has effectively hit the targets that would qualify him for two options payouts from his 10-year, high-risk, high-reward performance award. And this time around, these two payouts could be worth a combined $11 billion.

Elon Musk has a unique pay system as CEO of Tesla. He receives no salary for his work at Tesla, as his pay package is linked directly to the company’s market capitalization and financial growth. Proposed in March 2018, Musk’s performance award for his work at Tesla involves 12 milestones comprised of $50 billion additions to TSLA’s market cap.

For each of the 12 tranches that are achieved, Musk will vest in stock options that correspond to 1% of Tesla’s current total outstanding shares. Each tranche also gives Musk the option to purchase TSLA stock at $70 per share, a discount of over 90% from the company’s current price in the market.

As indicated by the company in its Q1 report, Tesla posted quarterly revenue of $10.39 billion and adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of $1.84 billion. This effectively surpassed milestones that triggered the fifth and sixth of Elon Musk’s 12-tranche performance award. At Tesla’s current valuation, these payouts correspond to a combined amount of about $11 billion.

When it was proposed, Tesla was aiming to reach a market cap of $650 billion, a target that seemed extremely far away then. It was also considered a high-reward and high-risk plan, as Musk would receive no compensation if Tesla fails to reach its targets. So far, however, Musk has been hitting his goals, potentially paving the way for the 10-year plan’s overall targets to be achieved well ahead of time.

Tesla’s Q1 earnings are undoubtedly impressive, though TSLA shares dipped over 4% on Tuesday’s trading. In a statement to Teslarati, Peter Hanks, an analyst at DailyFX, a news and finance research platform, noted that this drop was likely due to Tesla only meeting expectations. The analyst remarked that Tesla’s long-term prospects still look very good, however.

“Tesla’s revenue and earnings per share results were largely in line with analyst expectations, but given the price-to-earnings ratio of the stock and its role as a lightning rod of speculative risk appetite, meeting expectations is rather underwhelming. As a result, the electric car maker saw its shares dip slightly after the report was released.

“All in all, however, Tesla looks well-positioned to continue delivering more vehicles in the future as more production plants come online, which, in turn, could see the company reign in the ludicrous valuation metrics that it currently possesses. In the meantime, stock price gains may be limited relative to the run-up experienced in the second half of 2020,” Hanks said.

-

-

Don’t hesitate to contact us for news tips. Just send a message to tips@teslarati.com to give us a heads up.

SpaceX just picked up another $1.6 billion from the Pentagon, with the U.S. Space Force awarding two task orders worth $1.6 billion to fly 18 Falcon 9 missions from Vandenberg Space Force Base in California through the end of 2027. The launches will carry satellites for the Space Based Sensing and Targeting portfolio, a set of programs meant to help the military detect and track airborne threats and relay that information across forces in near real time.

The award falls under National Security Space Launch Phase 3 Lane 1, the Space Force’s faster, commercial style procurement track for missions that do not require the military’s most demanding certification process. It is also the largest single order publicly disclosed under that program so far, and the first task order issued since the Space Force nearly tripled Lane 1’s contract ceiling from $5.6 billion to $17 billion on July 17.

SpaceX to become America’s Military data backbone for missiles, drones, and warfighters

Eric Zarybnisky, the Space Force’s acting portfolio acquisition executive for space access, said the entire process, from identifying the requirement to signing the contract, took about two months, including a month set aside for companies to prepare proposals.

SpaceX is not just launching these satellites. It already holds the contracts to build two of the programs within the same portfolio, $4.16 billion for the Space Based Airborne Moving Target Indicator system and $2.29 billion for the Space Data Network Backbone, which Teslarati covered in May. That means SpaceX is now responsible for both building key pieces of the military’s next generation sensing network and getting them into orbit.

With this latest award, SpaceX’s Pentagon contract total for 2026 alone tops $8 billion, adding to a defense portfolio that already includes the Golden Dome missile defense software group SpaceX joined in April and a string of GPS launches it inherited after ULA’s Vulcan rocket ran into a booster anomaly, which we detailed in March.

Lane 1’s vendor pool technically includes seven companies: SpaceX, ULA, Blue Origin, Rocket Lab, Stoke Space, Impulse Space, and Relativity Space. In practice, SpaceX remains the only provider with the combination of launch cadence, flight proven Falcon 9 hardware, and West Coast infrastructure to support a campaign requiring roughly one Vandenberg launch a month for the next year and a half.

-

Some lawmakers have flagged the growing concentration of national security launches with one company as a risk worth watching. For now, the Space Force keeps backing SpaceX, with it being the company that shows up ready to launch.

SpaceX (NASDAQ: SPCX) got an absolutely crazy price target rating from Raymond James after the company experienced a tough first few weeks following its Initial Public Offering (IPO).

Despite the tumultuous start, SpaceX has plenty of believers, and the company’s massively successful Starship launch last Friday, its 13th test flight of the massive rocket, went so smoothly that Raymond James analysts pushed its price target on the company to roughly 7 times its current trading level.

SpaceX Starship just nailed something it’s never done before

The firm officially put a “Strong Buy” rating and an $800 price target on the stock. It currently trades at around $113. Its all-time high is $225.64, reaching this trading level shortly after shares first went public.

Raymond James’ price target is tied to the firm’s confidence after Starship’s 13th test flight. Analysts at the firm said it was an incremental step that reduces engineering risks, citing the widely successful heat shield test that CEO Elon Musk recently detailed, the smooth deployment of Starlink V3 satellites, and a successful in-space engine relight.

SpaceX also managed to see Starship splash down safely in the Indian Ocean, while the Super Heavy Booster fell down to the Gulf of America with no incidents.

It is interesting to see these launches have such a tremendous impact on the stock and what investors think of it. After SpaceX initially delayed the Starship launch last week, shares fell tremendously. Most probably did not realize that the stand-down is a standard practice, especially if everything is not perfect.

-

The mission was initially aborted due to an issue with Raptor engines. This was resolved, and Starship launched last Friday after another delay on Thursday, which was caused by weather.

Now that analysts have seen what SpaceX launches are capable of and how impressive the feat is, firms are adjusting their price targets accordingly, making it known that they have high expectations for the space exploration company.

Elon Musk

SpaceX Starship just nailed something it’s never done before

SpaceX’s Starship flew successfully Friday, landing both stages and deploying its first Starlink V3 satellites.

Starship’s thirteenth test flight delivered exactly what SpaceX needed with a clean liftoff, two successful stage recoveries, and the first real payload the vehicle has ever carried to space. Booster 20 and Ship 40 lifted off at 5:51 p.m. CT from Starbase, and by the time the mission wrapped roughly an hour later, both halves of the rocket had done exactly what they were supposed to do.

Booster 20 separated from Ship 40 a few minutes into the flight and stuck a controlled splashdown in the Gulf of Mexico about six minutes after liftoff. That is a meaningful turnaround from Flight 12 in May, when the booster lost several engines during its boostback burn before a hard water landing attempt.

Starship as seen from Starlink satellites pic.twitter.com/e2hvfmnewh

— Elon Musk (@elonmusk) July 25, 2026

Starship 40’s performance was arguably the bigger win. The vehicle deployed the first 20 operational Starlink V3 satellites Starship has ever carried, then flew a suborbital arc to a landing in the Indian Ocean that SpaceX commentator Dan Huot called the company’s softest splashdown yet. “This is a dream scenario for this team that’s trying to get this heat shield data,” Huot said on the live broadcast, according to Space.com’s live coverage. “I’m a little over the moon right now. Wow. Lucky number 13.”

Unlike the mass simulators SpaceX flew on Flight 12, these were production Starlink V3 satellites, meant to extend solar arrays and antennas and attempt to link with the broader constellation before reentering minutes later. Getting real hardware through a full deploy sequence on only the second flight of the V3 generation keeps Starship on schedule for the payload work NASA is counting on for future Artemis lunar landings.

What an awesome launch, really seems like everything went super well and it was all incredibly smooth.

SpaceX is awesome. Very interested to see how the market will respond on Monday pic.twitter.com/KSHmyBfV55

— TESLARATI (@Teslarati) July 25, 2026

-

— TESLARATI (@Teslarati) July 25, 2026

The flight also arrives at a moment when SpaceX needed a win. SPCX has traded below its $135 IPO price since mid-July, as Teslarati reported when the mission slipped to Friday, and short interest has climbed to roughly a third of the tradable float. A clean flight will not fix a balance sheet, but it does answer the one question SpaceX absolutely needed answered this week: whether the fixes made after the July 16 abort would hold up under real flight conditions. They did, on both stages, on the first try after the redesign.

SpaceX has not set a target date for Flight 14, though the company has said it wants to push toward an orbital attempt on the next mission. After Friday, that goal looks a lot more within reach.

Autonomous vehicle red tape gets slashed by Trump Administration

Elon Musk has a crazy prediction about AI in two years