Investor's Corner

Tesla shares company-compiled analyst consensus for Q4 2024 deliveries

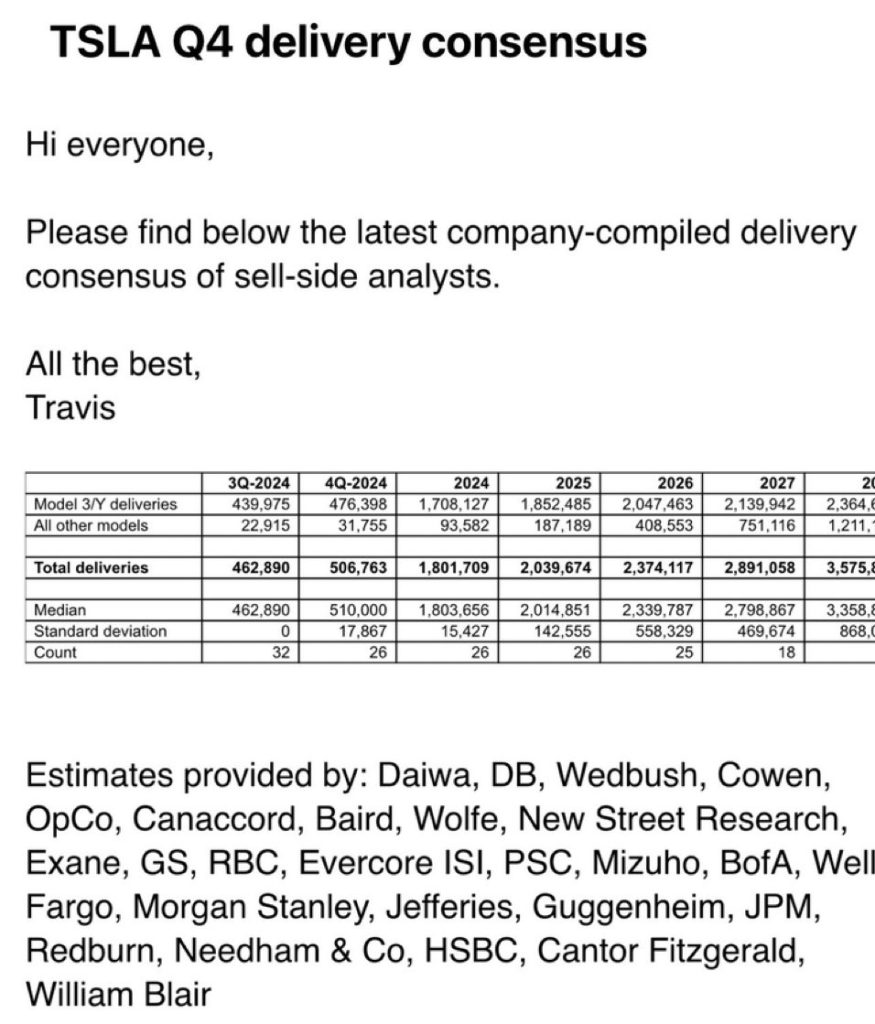

Tesla (NASDAQ:TSLA) has shared its latest company-compiled delivery consensus from sell-side analysts. Based on the consensus, analysts are not expecting Tesla to beat its annual delivery figures from 2023.

The consensus:

- As per Tesla’s company-compiled consensus, analysts are expecting the electric vehicle maker to post 506,763 vehicle deliveries for Q4 2024.

- Analysts expect Tesla to report 476,398 Model 3 and Model Y deliveries, as well as 31,755 deliveries of all other models.

- With these results, Tesla’s company-compiled consensus expects a global total of 1,801,709 vehicle deliveries for 2024.

Tesla’s sources:

- The analyst consensus for Tesla’s Q4 2024 vehicle delivery results was provided by the following firms:

- Daiwa, DB, Wedbush, Cowen, OpCo, Canaccord, Baird, Wolfe, New Street Research, Exane, GS, RBC, Evercore ISI, PSC, Mizuho, BofA, Well Fargo, Morgan Stanley, Jefferies, Guggenheim, JPM, Redburn, Needham & Co, HSBC, Cantor Fitzgerald, and William Blair

Tesla’s Q4 consensus vs 2023’s deliveries:

- For comparison, Tesla reported a total of 484,507 vehicle deliveries for Q4 2023.

- These were comprised of 461,538 Model 3 and Model Y, as well as 22,969 units of Tesla’s other models.

- With these results, Tesla delivered a total of 1,808,581 vehicles globally in Full Year 2023.

Tesla’s FY 2024 deliveries in context:

- For Tesla to match its 2023 delivery numbers, the company would have to deliver about 515,000 vehicles this fourth quarter.

- This, however, would require Tesla to deliver the most vehicles it has ever delivered in a quarter.

- Even if Tesla does not meet its 2023 figures this year, the company’s overall performance is not as grim as what skeptics may believe.

- Tesla’s business, after all, is no longer just focused on its automotive division. Tesla Energy is growing rapidly, and the company’s work on its FSD system could pave the way for a software licensing business in the long run.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Tesla received a price target upgrade just on the heels of what was a crazy successful quarter for its automotive business, as the company reported a delivery beat of over 15 percent for Q2.

Jefferies analysts are upping Tesla’s price target (NASDAQ: TSLA) to $400 from $375, while maintaining their “Hold” rating on shares, and the strong automotive deliveries from Q2 is a big reason. However, there are some other catalysts that Jefferies believes position Tesla for a strong position in the second half of the year.

Strong Deliveries

Tesla reported 480,000 deliveries for Q2, while Wall Street was between 395,000 and 405,000, as an overall consensus. It was an incredibly strong quarter from a delivery perspective, and Tesla sold well more than it produced during the three months.

Tesla crushes Wall Street expectations, beats delivery estimates by over 15 percent

While vehicle deliveries are not necessarily looked at in the light that they used to be, Tesla still maintains a lot of advantages for keeping deliveries strong. With the loss of the $7,500 EV Tax Credit last year, Tesla still maintains a strong demand case for its EVs.

Robotaxi Performance

Tesla has been operating Robotaxi for over a year now, as it launched in Austin in mid-2025. That program has expanded to Houston and Dallas, the San Francisco Bay Area, and, most recently, Miami, Florida, the suite’s first appearance in the Sunshine State.

While the Robotaxi suite is still in its early phases and Tesla is working through things like fleet size and wait times, the company has been able to undercut the pricing of its competitors and has a great safety record.

Merger Speculation with Tesla and SpaceX

This is perhaps the biggest topic that many are speaking about with Tesla and SpaceX, and it is the one thing that seems to be on the mind of every investor.

Jefferies warns that growing talk of a Tesla-SpaceX merger could cause Tesla stock to trade more like a SpaceX proxy, which may disconnect it from underlying automotive fundamentals. SpaceX has a lot going for it, especially its compute deals that have been widely publicized as of late.

Profitability in New Projects Could Take Some Time

Tesla has a few long-term ventures in the pipeline, most notably the Optimus project and Robotaxi, which is launched but will take several years to expand to a meaningful level that resonates with everyday people.

This is something that investors need to be careful of. Tesla’s projects could take some time to round out, so Jefferies advises that these may carry initial losses, rather than immediate profit. Seasoned Tesla investors have echoed something like this for a long time; they knew going in it would not be an open-and-shut strategy. It was going to take time.

These new projects are no different.

Investor's Corner

NASA taps SpaceX to launch the telescope that could unlock new worlds

NASA’s Roman Space Telescope heads to orbit this August aboard SpaceX’s Falcon Heavy with massive scientific ambitions.

SpaceX is set to play a central role in one of NASA’s most anticipated science missions in years. The company’s Falcon Heavy rocket, currently the most powerful operational launch vehicle in the world, will carry the Nancy Grace Roman Space Telescope into orbit on August 30 from Kennedy Space Center in Florida. Roman is now in final preparations inside the Payload Hazardous Servicing Facility, where on June 26 technicians used a crane to lift the observatory into a specialized stand for fueling and pre-launch testing.

Roman is named after Nancy Grace Roman, NASA’s first chief of astronomy, whose career helped shape how the agency approaches space science.

NASA chose SpaceX Falcon Heavy because of Roman’s needs to reach a specific orbit far from Earth, well beyond where a standard Falcon 9 can deliver it. The Falcon Heavy, which first flew in 2018, has since become NASA’s go-to option for missions that need serious muscle without the cost and complexity of older launch systems.

Celebrating SpaceX’s Falcon Heavy Tesla Roadster launch, seven years later (Op-Ed)

Roman will carry a field of view at least 100 times wider than the Hubble Space Telescope, meaning it can photograph enormous swaths of the universe in a single shot rather than the narrow slices Hubble captures. That difference in scale is significant. While Hubble reshaped our understanding of the cosmos over 30 years, Roman is built to work faster and wider, surveying hundreds of millions of galaxies at once.

One of Roman’s most compelling capabilities is its potential to discover and photograph planets orbiting stars outside our solar system, and with enough precision to directly image planets that would otherwise be lost. That means scientists could study the atmosphere and surface characteristics of distant worlds rather than simply confirming they exist. Combined with Roman’s sweeping field of view, the telescope could detect thousands of exoplanets, and some of those planets may be in habitable zones where liquid water could exist. No telescope currently in operation has this level of power and capability. That capability alone could change what we know about other worlds, and perhaps finally answer the question: are we the only intelligent lifeforms in existence?

What Roman actually finds once it reaches orbit is an open question, and that is exactly what makes this launch worth watching.

Elon Musk

California snubs Tesla in its newly passed EV incentive that favors Rivian and Lucid

California passed a $135 million EV incentive that rewards Rivian and Lucid while sidelining Tesla

California just drew a line in the EV incentive sand to put Tesla on the wrong side of it. The state recently passed a $135 million program offering first-time electric vehicle buyers a direct incentive with no application required, but the rules were written in a way that leaves Tesla at a structural disadvantage compared to Rivian and Lucid.

The program caps eligible vehicles at $50,000 for new EVs and $25,000 for used ones. That pricing threshold rules out a significant portion of Tesla’s lineup, though some lower-priced Model 3 and Model Y configurations would still qualify. California-based automakers are exempt from the price cap entirely, regardless of what their vehicles cost. Rivian, headquartered in Irvine, and Lucid, based in the San Francisco Bay Area, both benefit from that exemption. Rivian’s R2 starts at roughly $45,000 but has versions above the cap. Lucid’s Air and Gravity start at $70,990 and $79,990 respectively, well above any threshold a non-California company would face.

California hits Tesla Cybercab and Robotaxi driverless cars with new law

Tesla built its reputation and a significant portion of its early market share in California, where EV adoption has consistently led the nation. The company operates its original factory in Fremont, California, and the state was home to Tesla’s headquarters for most of its existence. That changed in 2021 when Tesla moved its corporate headquarters to Austin, Texas. Since then, the relationship between the company and California Governor Gavin Newsom has been openly adversarial, with Musk and Newsom trading public criticism on multiple occasions.

California’s EV incentive landscape has shifted repeatedly in recent years, and Tesla has previously lost eligibility for state-level programs as its vehicles exceeded income-adjusted price thresholds. The federal $7,500 EV tax credit, which Tesla models have qualified for and lost depending on policy cycles, is no longer available after it expired without renewal, making state-level programs more meaningful to buyers than they have been in years.

The practical impact for buyers is more nuanced than the headline suggests. California residents purchasing a Tesla under $50,000 for the first time can still access the incentive. But the exemption written for California-based manufacturers is a structural advantage that rewards where a company plants its headquarters flag rather than where it builds its products, and Tesla moved that flag to Texas.

Tesla Semi enters new Pilot Program with interesting challenge

Tesla is building a wheelchair-accessible Robotaxi