Investor's Corner

TSLA Extended Hours Action after Q1 Report & Conference Call

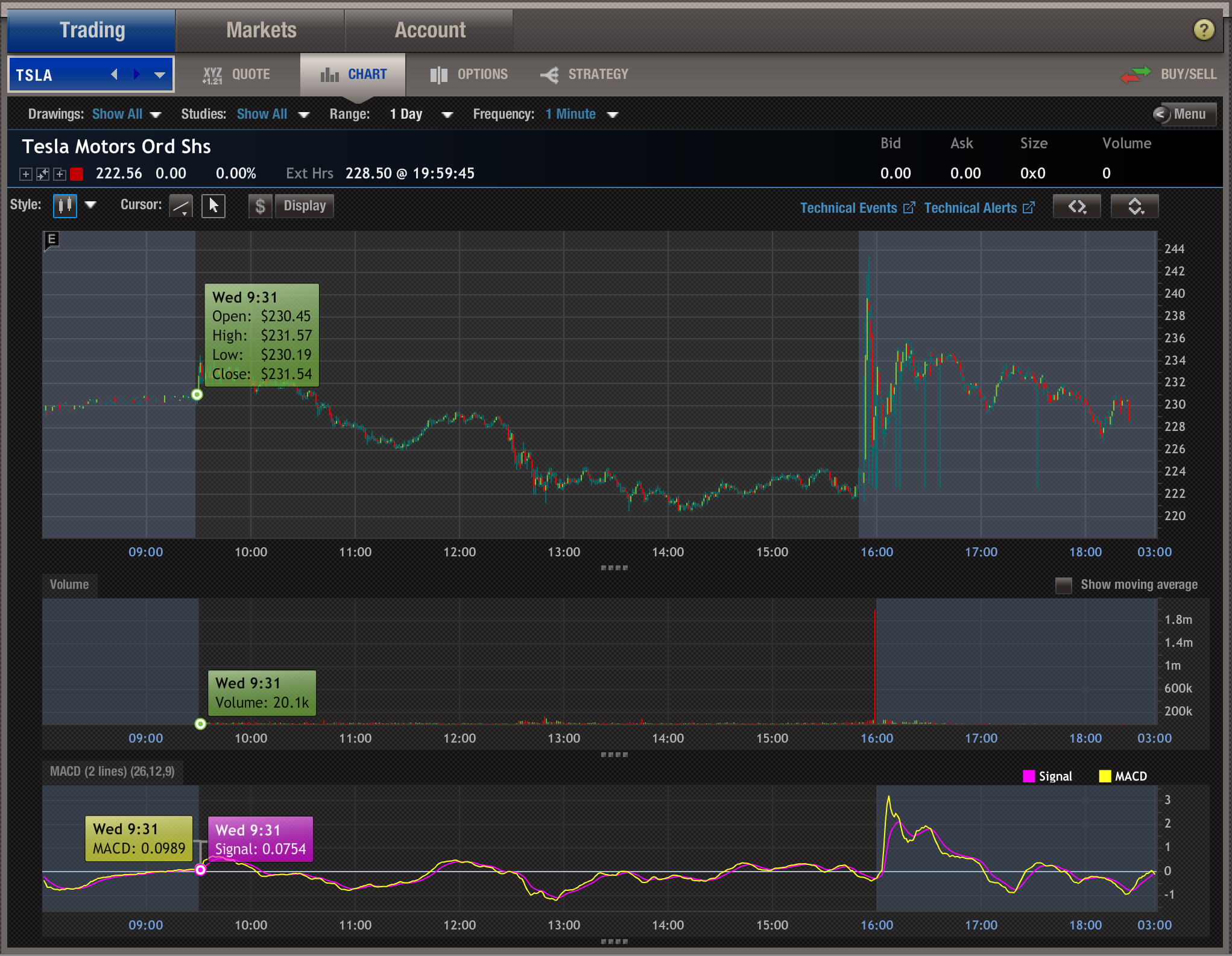

TSLA action on the day of the Q1 Report was effectively a wash: TSLA stock opened at 230.29 and closed the regular trading session down -4.20% at $222.56, but gained almost all of it back during “extended hours”, closing the day at 228.50. Right after the quarterly results were released, it traded as high as $243.43.

Source: OptionsHouse Trading Application

Obviously traders and brokers liked both the results and the subsequent answers that were given in the conference call.

What items did the traders actually like?

– Beating analysts’ expectations for earnings by 3 cents.

– Revenue of $1.15B, with sales of $1.6B. Net loss of $ -57c a share. A beat on the loss, a meet on sales.

– A decrease in capital expenditures by 47% from Q4 2015, with spending decreases at both Fremont factory and Gigafactory.

– A much more ambitious timeline of delivery of vehicles: 500,0000 vehicles in 2018 (two years ahead of the previous projections), and 1 Million vehicles in 2020.

– Adjusted plans for the Gigafactory to support the new timeline targets in 2018.

– A mix of 100-150K Model S and X, plus 300-400K Model 3, for 2018 vehicle deliveries.

– A July 1st, 2017 deadline for suppliers of Model 3 parts.

– A combination of capital & debt to support the more ambitious timeline.

– Projections of 20,000 vehicles delivered in Q2, and 50,000 in the rest of the year, maintaining the 80,000 to 90,000 vehicles projection for the year 2016.

– Brushing off the loss of 2 top executives for production and manufacturing, because Tesla is the place top talent in manufacturing would want to be, since at Tesla “innovation in manufacturing is more important than innovation in design” (a subtle swipe at Apple).

Interestingly no new reservation numbers for Model 3 were given, as we stand at “almost 400,000” from a couple of weeks ago.

Will Tesla be able to deliver on the adjusted projections? History tells us probably no. But short-term, Elon & Co. delivered: the pessimism that was evident among brokers and traders before the report and conference call, pretty much evaporated. My expectation for Thursday’s market is an opening between 228 and 230.

After 6 sessions that brought the stock from $255 down 9% to $222, we may see momentum start going the other way up again.

Update

While TSLA, as expected, opened at 228.46, it quickly turned red and within an hour was done 4.5%. From the morning broker’s comments, not everybody is buying Elon’s rosy projections. You have now witnessed how “volatile” TSLA stock can be: it went from an after-hours peak of $243 to $212 in a span of a few trading hours, a 13% drop. Not a stock for the faint of heart.

In a pointed message on X, Elon Musk warned that firms maintaining significant short positions in SpaceX over time face “very low” survival probability.

The statement comes amid post-IPO volatility for the rocket company, now trading under the ticker $SPCX.

The survival probability of firms who maintain a significant short position in SpaceX over time is very low

— Elon Musk (@elonmusk) July 17, 2026

Five weeks after what was described as the largest IPO in history, the stock had fallen roughly 30% from its peak above $2.6 trillion, briefly surpassing Microsoft and Amazon in market value. Short sellers celebrated gains of about $8.7 billion, but Musk’s reply underscores his long-term conviction.

The warning directly echoes a detailed bullish analysis arguing that Starship’s cost reductions could unlock a multi-trillion-dollar space economy. Projects ranging from solar power beamed from orbit and asteroid mining to orbital data centers and Mars terraforming were projected to create over $100 trillion in new market capitalization.

In this vision, SpaceX acts as the essential infrastructure provider, akin to AWS for cloud computing, capturing monopoly-like revenues from launches, crew transport, and data traffic across a rapidly expanding frontier.

This is far from the first time Musk has targeted short sellers. With Tesla, he has repeatedly framed persistent bears as destined for major losses. In July 2024, Musk declared that once Tesla achieves full autonomy and volume production of Optimus robots, “anyone still holding a short position will be obliterated. Even Gates,” referencing Microsoft co-founder Bill Gates’ reported short bets.

Elon Musk reveals what Tesla stock surge could do to Bill Gates

Earlier, in 2018, he taunted shorts that they had “about three weeks before their short position explodes,” a remark followed by sharp stock gains. Musk has also called short selling “value destroying” and once suggested it “should be illegal,” viewing it as betting against innovation and progress.

Critics often dismiss Musk’s optimism as hype, especially when near-term metrics like quarterly deliveries or stock fluctuations disappoint.

Yet his pattern remains consistent: framing short positions against his companies as fundamentally misjudging exponential technological leaps. For SpaceX shorts, the message is clear: betting against multi-planetary ambitions and the infrastructure monopoly they enable carries existential risk for the firms involved.

As Musk and supporters see it, the space economy’s upside dwarfs Earth-bound valuation models, making today’s dips temporary in a decades-long ascent.

Elon Musk

SpaceX Starship Flight 13 aborted at Zero and Musk just told us what broke

Four Raptor engines failed to ignite at T-zero, forcing SpaceX to scrub Starship Flight 13 Thursday.

SpaceX scrubbed the Starship Flight 13 launch attempt Thursday evening at the last possible moment, after four of the Super Heavy booster’s 33 Raptor 3 engines failed to ignite during the startup sequence. The 90-minute window had opened at 6:45 p.m. EDT from Starbase in Boca Chica, Texas, and the countdown had proceeded without issue all day, with more than 11.5 million pounds of liquid methane and liquid oxygen being fully loaded into the rocket before the automated abort triggered. SpaceX’s launch directors posted on X, “Standing down from today’s flight test attempt,” and shut down the livestream shortly after.

Musk confirmed the root cause within hours. “Some of the engines didn’t start, triggering an automatic launch abort,” he wrote on X. “To be confident of a good flight, 2 Raptors will be removed and replaced. Most probable launch timing is early next week.” SpaceX engineers began draining propellant tanks immediately and Booster 20 was rolled back to its hangar for inspection.

The timing adds a layer of significance that did not exist during any of the previous 12 Starship flights. This is the first time SpaceX has attempted to launch Starship since the company made its stock market debut in June, listing under ticker SPCX at $135 per share. Public investors are now watching every Starship outcome in real time, and a last-second abort carries more visibility than it would have six months ago.

Flight 13 was designed to be one of the most consequential tests in the program’s history. It was set to carry 20 Starlink V3 satellites, the first operational payload Starship has ever attempted to deploy. Six of those satellites carried external cameras to photograph Starship’s heat shield from the outside during flight, which would act as a self-inspection approach SpaceX has never attempted before. The mission also needed to complete a Raptor engine relight in space, a step SpaceX skipped on Flight 12 in May after losing an engine during ascent. That Flight 12 booster also flipped 90 degrees off course during its boostback burn when five engines failed to reignite.

SpaceX has not announced an official next launch date. Musk’s “early next week” window points to July 21 or 22 at the earliest, pending the engine swap and a return to the pad.

Lucid CEO Silvio Napoli responded to rumors of an imminent bankruptcy that was reportedly being mulled after a report stated the automaker was working with the firm AlixPartners to iron out its next steps.

The company felt a massive loss on Wall Street yesterday, as the report essentially pushed the stock down as much as 55 percent on Tuesday.

The report, published initially by Eletric-Vehicles.com, claimed Lucid was essentially in dire straits and was told by AlixPartners, a commonly used restructuring advisor, to either take shares private or file for Chapter 11 bankruptcy protection.

Lucid’s head of Communications, Nick Twork, immediately challenged the report and stated the company “has sufficient liquidity to carry its operations well into next year.”

Now, the company’s CEO is chiming in as well, stating that the report is “so far from the facts that they require a direct response.”

Napoli said:

“Lucid is not considering bankruptcy or a transaction to take the company private. Those reports are false. The Board did not explore either scenario. Period.

As disclosed in our most recent quarterly filing, Lucid has sufficient liquidity to fund its operations well into next year.

We work with outside advisors to improve operational performance and execution. They are not advising Lucid on a take-private transaction or bankruptcy, and any suggestion that they have recommended either course of action to management or the Board is false.

My priority is clear: turn this company around. That is where the leadership team and I are focused.

I look forward to providing a full update during our quarterly earnings call on August 4th.”

🚨 Lucid CEO Silvio Napoli calls rumors of financial issues “so far from the facts that they require a direct response.”

Read his full remarks here: https://t.co/t3Pg1NHvzy pic.twitter.com/LvHUPhO4Qf

— TESLARATI (@Teslarati) July 15, 2026

It seems pretty clear that Lucid is confident things will be okay, and, to be honest, they should not have much to worry about, especially considering the company has been backed by the Saudi Public Investment Fund (PIF) for years. It has solid financial backing, and its sales, while weak, are pretty much right on par with a company of this age.

Lucid also sent a Cease & Desist letter to the publication for their report.

Lucid shares have rebounded nicely and are up nearly 21 percent at the time of publication. As soon as the company dispelled the rumors of bankruptcy yesterday, the stock began to climb back toward more reasonable levels.

Tesla expands ridesharing service in California to new hotspot

Tesla reveals 2026 Summer Update with crazy fixes to Nav and more