Investor's Corner

Tesla increases Q2 production by 20% but falls short of deliveries

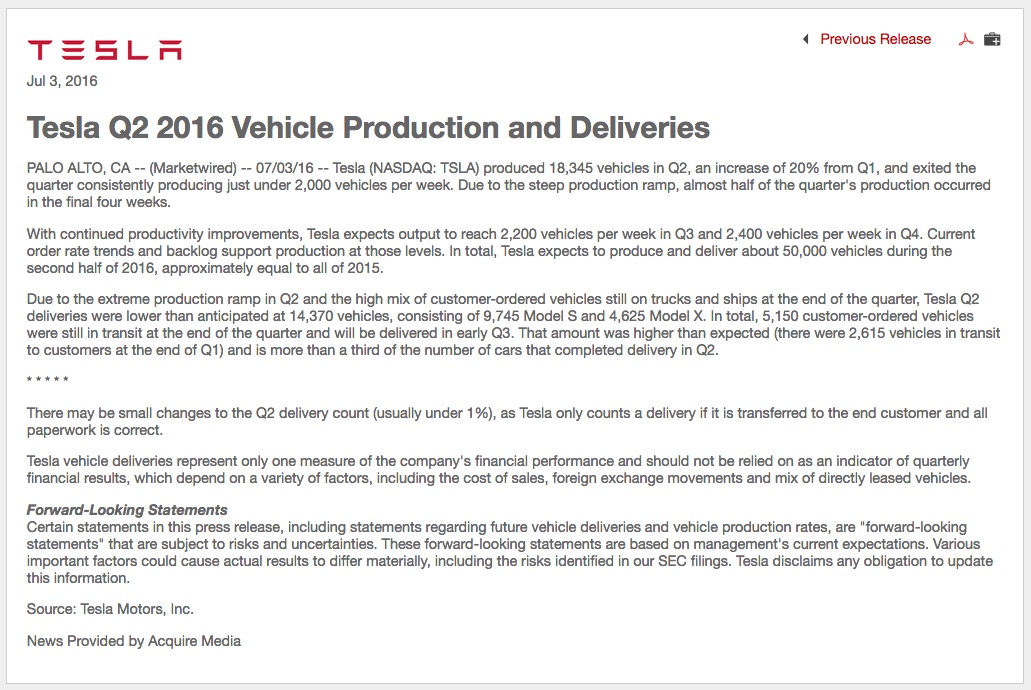

Tesla issued its Q2 production and delivery numbers, indicating that the company produced 20 percent more cars this quarter than the previous however fell short in delivering the vehicles to customers.

The Silicon Valley based electric car company reported 18,345 vehicles produced in Q2 or roughly just under 2,000 vehicles per week, and delivered 14,370 vehicles though guidance was set at 17,000 vehicles. Tesla attributed the fact that “Tesla Q2 deliveries were lower than anticipated” to having “5,150 customer-ordered vehicles [..] still in transit, a much higher number than the 2,615 vehicles in transit to customers at the end of Q1.”

Tesla added that half it saw a huge production ramp towards the end of Q2 resulting in half of the quarter’s production occurring in the final four weeks. Model S continues to lead in terms of deliveries consisting of 9,745 units delivered versus 4,625 Model X.

Tesla Q2 2016 Vehicle Production and Deliveries Release [Source: Tesla Investor Relations]

As far as total deliveries for the full year 2016, “Tesla expects to produce and deliver about 50,000 vehicles during the second half of 2016”, which means it will not be able to hit the low end of previous guidance of “80,000 to 90,000 new vehicles in 2016” as the projected 2016 yearly number for 2016 now stands at 79,000.

Tesla Market Action

During the past week $TSLA stock seems to have safely discarded the major bad news about the Model S driver killed while using Autopilot. While the press was flooded with negative articles about the accident (I counted an average of 2-4 articles per day in the Wall Street Journal and on Bloomberg), and the news ended up being reported 2 days in a row in the national news broadcast of all major networks, Wall Street traders shrugged the bad news off completely. While the stock had a temporary drop to 206 in after hours extended trading on Thursday when the news came up on the wire, $TSLA stock shot back with a vengeance to the $216 level on Friday, giving traders one of the best weeks of the year with a whopping 15% weekly gain.

What will $TSLA stock do when the market reopens on Tuesday after the 4th of July holiday? If we look at the response after the Q1 deliveries were reported on April 4, most news outlets reported that Tesla Missed Its Q1 Delivery Targets. Wall Street traders did not care much then, trading the stock up for 3 sessions to an all time high of $266 after the news. In that case, Tesla had reiterated the 80 to 90 thousand deliveries for the year, which may have softened the bad news of total quarterly deliveries.

This is a quick look to today’s headlines in response to the Q2 delivery numbers.

-

-

- The Verge: Tesla falls short of delivery estimates in Q2 despite ramping production

- NBC News: Tesla cranks out 20% more cars in Q2, but struggles to deliver them

- USA Today: Tesla deliveries in Q2 fall short of estimates

- ABC News: Tesla Vehicle Deliveries Slip in Q2

Technical indicators were in a really good spot at market close on Friday: 4-days of positive Heikin Ashi charts, MACD positive, MACD averages “pinching”, indication the possible start of a longer breakout on the upside. But the possible bullish breakout could be stopped by the market reaction to what is effectively a “miss” of guidance for the year, more than the smaller numbers for the quarter.

Will Wall Street traders shrug off the Q2 negative results like they did with Q1?

Source: Wall Street I/O

Elon Musk

SpaceX Starship just nailed something it’s never done before

SpaceX’s Starship flew successfully Friday, landing both stages and deploying its first Starlink V3 satellites.

Starship’s thirteenth test flight delivered exactly what SpaceX needed with a clean liftoff, two successful stage recoveries, and the first real payload the vehicle has ever carried to space. Booster 20 and Ship 40 lifted off at 5:51 p.m. CT from Starbase, and by the time the mission wrapped roughly an hour later, both halves of the rocket had done exactly what they were supposed to do.

Booster 20 separated from Ship 40 a few minutes into the flight and stuck a controlled splashdown in the Gulf of Mexico about six minutes after liftoff. That is a meaningful turnaround from Flight 12 in May, when the booster lost several engines during its boostback burn before a hard water landing attempt.

Starship as seen from Starlink satellites pic.twitter.com/e2hvfmnewh

— Elon Musk (@elonmusk) July 25, 2026

Starship 40’s performance was arguably the bigger win. The vehicle deployed the first 20 operational Starlink V3 satellites Starship has ever carried, then flew a suborbital arc to a landing in the Indian Ocean that SpaceX commentator Dan Huot called the company’s softest splashdown yet. “This is a dream scenario for this team that’s trying to get this heat shield data,” Huot said on the live broadcast, according to Space.com’s live coverage. “I’m a little over the moon right now. Wow. Lucky number 13.”

Unlike the mass simulators SpaceX flew on Flight 12, these were production Starlink V3 satellites, meant to extend solar arrays and antennas and attempt to link with the broader constellation before reentering minutes later. Getting real hardware through a full deploy sequence on only the second flight of the V3 generation keeps Starship on schedule for the payload work NASA is counting on for future Artemis lunar landings.

What an awesome launch, really seems like everything went super well and it was all incredibly smooth.

SpaceX is awesome. Very interested to see how the market will respond on Monday pic.twitter.com/KSHmyBfV55

— TESLARATI (@Teslarati) July 25, 2026

-

— TESLARATI (@Teslarati) July 25, 2026

The flight also arrives at a moment when SpaceX needed a win. SPCX has traded below its $135 IPO price since mid-July, as Teslarati reported when the mission slipped to Friday, and short interest has climbed to roughly a third of the tradable float. A clean flight will not fix a balance sheet, but it does answer the one question SpaceX absolutely needed answered this week: whether the fixes made after the July 16 abort would hold up under real flight conditions. They did, on both stages, on the first try after the redesign.

SpaceX has not set a target date for Flight 14, though the company has said it wants to push toward an orbital attempt on the next mission. After Friday, that goal looks a lot more within reach.

Tesla short sellers won big following the company’s massive fall on Wall Street after it reported subpar Earnings on Wednesday.

Tesla short sellers collected about $4.12 billion in single-day profits on Thursday, according to Bloomberg. Shares fell as much as 15 percent during Thursday’s session. It closed as one of the worst days for Tesla on Wall Street in the past three years.

Investors sold off the stock after Tesla said it would aggressively direct its spending toward AI and its Optimus robot project. The company had record revenues, which were driven by one of the strongest quarters in terms of vehicle deliveries in company history.

However, it missed EPS estimates by reporting just $0.33, a far cry from the $0.53 analysts expected.

S3 Partners reported that about 3 percent of Tesla’s outstanding stock is sold short. Managing Director at S3, Ihor Dusaniwsky, provided the short seller’s potential profit, as well as another figure: shorts have likely had paper gains of $8.92 billion this year, as Tesla shares are down 30 percent in 2026.

-

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Tesla has burned short sellers many times in the past, but the company’s latest Earnings Call was a chance for those skeptics to taste some payback. Although the company gave some very transparent information regarding future projects, the rollout of Robotaxi, Optimus, and Semi, many investors took their profits on Thursday.

Notable short sellers like Michael Burry have been transparent about their skepticism around Tesla shares. Burry just revealed three weeks ago that he had opened up a new short on the stock, stating he shorted Tesla shares at $416.22. “Happy it jumped back to this level,” he said in a blog post.

At the time of publication, Tesla shares were down about 3 percent and the stock was trading at $309.92.

Tesla stock (NASDAQ: TSLA) endured one of its sharpest single-day declines in years on July 23, tumbling approximately 14.5 percent and closing near $320 after opening the session around $374. The drop erased more than $140 billion in market value amid heavy trading volume and left the shares at multi-week lows.

The sell-off followed the company’s second-quarter 2026 results, released the previous evening. Tesla reported record revenue of $28.2 billion, up 26 percent year over year, driven by a Q2-record 480,126 vehicle deliveries. Energy storage deployments also rose strongly.

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Yet profitability disappointed sharply. Operating income fell 57 percent to $398 million, compressing the operating margin to just 1.4 percent. Non-GAAP earnings per share came in at $0.33, well below the roughly $0.53 analysts had expected. Free cash flow turned negative by $1.1 billion as capital expenditures surged 142 percent to $5.8 billion, largely tied to accelerated spending on artificial intelligence, robotics, and autonomous systems.

The losses on capex were expected, as Tesla said it would be spending heavily in 2026.

Investors also reacted to lingering uncertainty surrounding key product timelines. During the Earnings Call, management reiterated ambitions for Robotaxi deployment and the Optimus humanoid robot, but offered limited new concrete milestones, renewing questions about execution pace that have long accompanied Tesla’s ambitious roadmap.

The magnitude of the decline places it among Tesla’s more severe one-day percentage losses since its 2010 initial public offering. Historically, the two largest single-day drops (split-adjusted) remain September 8, 2020, when shares fell 21.1 percent amid broader market volatility and valuation concerns, and January 13, 2012, with a 19.3 percent plunge during the company’s early growth struggles.

-

Other notable declines include an 18.6 percent drop on March 16, 2020, at the onset of pandemic-related market turmoil. Thursday’s move ranks roughly ninth on the all-time list but stands out as the steepest in more than a year.

Despite the short-term pain, Tesla’s long-term trajectory has repeatedly recovered from such volatility. The latest results underscore both the strength of its core automotive and energy businesses and the near-term costs of heavy investment in next-generation technologies.

Tesla Summer Update begins rolling out: a look at the new features