News

Hyundai protects buyers from Trump’s tariffs with assurance program

Hyundai’s new Assurance Program will absorb Trump’s auto tariff costs, keeping prices flat for U.S. buyers.

Hyundai is protecting buyers from U.S. President Trump’s auto tariffs through its new Assurance Program.

The South Korean automaker’s U.S. COO Claudia Marquez launched the Assurance Program at the 2025 New York International Auto Show. The initiative addresses the impact of President Trump’s 25% tariffs on the auto sector, a dominant topic at the event.

Marquez emphasized Hyundai’s commitment to price stability during his announcement. The Assurance Program absorbs tariff-related costs, leveraging Hyundai’s robust U.S. production to mitigate impacts.

“When it comes to the customers, which again is tough and even for us just for planning purposes, what we wanted to make sure is that we have a plan, so we launched our Hyundai Assurance Program, which is confirming and assuring to customers that [prices] are not going to go up, at least this next couple of months,” she told Yahoo Finance.

Hyundai of America produces 40% of its vehicles in the U.S. through its Alabama factory and the newly opened Hyundai Motor Group Metaplant America (HMGMA) in Savannah, Georgia. The Georgia plant began Ioniq 5 production in October 2024 and plans to start Ioniq 9 output by Q1 2025.

“We have a strong representation in the US. We have a factory in Alabama, and just recently, two weeks ago, we opened our new Metaplant in Savannah, Georgia, where we produce our EVs Ioniq 5 and Ioniq 9,” Marquez said.

As President and CEO Jose Muñoz noted, Hyundai’s localization strategy strengthens its tariff resilience. Initially focused on EVs, HMGMA will also produce hybrids following a 2024 dip in EV sales.

“We are looking forward to officially opening Hyundai Motor Group Metaplant America (HMGMA) in Georgia. Our localization strategy in the important U.S. market will help mitigate the impact of any potential policy change,” Muñoz said at the company’s annual shareholders’ meeting.

While Hyundai’s U.S. plants provide a buffer, building such facilities is costly and time-intensive, with potential policy shifts looming by 2028. For now, the Assurance Program and localized production help Hyundai navigate Trump’s tariff, ensuring customer affordability amid trade uncertainties.

Elon Musk

Elon Musk calls out $2 trillion SpaceX IPO valuation as ‘BS’

In a swift rebuke on X, Elon Musk dismissed reports claiming SpaceX had confidentially filed for an initial public offering targeting a valuation above $2 trillion, labeling the information as unreliable.

Elon Musk is quick to call out any false information regarding him or his companies on his social media platform, known as X.

A recent report that claimed SpaceX was aiming to go public with an IPO in the coming weeks at a massive valuation of $2 trillion was called out by Musk, who referred to it as “BS.”

In a swift rebuke on X, Elon Musk dismissed reports claiming SpaceX had confidentially filed for an initial public offering targeting a valuation above $2 trillion, labeling the information as unreliable.

The exchange highlights ongoing media speculation about the rocket company’s future and Musk’s frustration with what he views as inaccurate financial reporting. The report came from Bloomberg.

Don’t believe everything you read.

Bloomberg publishes bs.

— Elon Musk (@elonmusk) April 3, 2026

The controversy erupted on April 2, 2026, when influencer Mario Nawfal amplified claims from Bloomberg.

The outlet posted that SpaceX had boosted its IPO target valuation above $2 trillion, describing it as potentially one of the largest public offerings in history. Musk challenged the story.

It echoes past instances where Musk has corrected valuation rumors about his companies, emphasizing that speculation often outpaces reality.

Background context adds nuance.

Earlier reports indicated SpaceX had filed confidential IPO paperwork with the U.S. Securities and Exchange Commission, potentially positioning it for a record-breaking debut that could eclipse Saudi Aramco’s 2019 listing.

Initial estimates pegged a possible valuation north of $1.75 trillion, building on a post-merger figure around $1.25 trillion after SpaceX absorbed xAI. A subsequent Bloomberg update claimed advisers were floating figures above $2 trillion to investors, with the offering potentially raising up to $75 billion.

SpaceX remains a private powerhouse. Its achievements include thousands of Starlink satellites providing global broadband, routine Falcon 9 rocket reusability, and a mission to slash launch costs, along with ambitions for Starship to enable Mars colonization.

The company also benefits from government contracts with NASA and the Department of Defense. A public listing could democratize access for retail investors while subjecting SpaceX to greater scrutiny and quarterly reporting pressures.

Critics of the reports point to the confidential nature of filings, which limits verifiable details. Musk has previously downplayed inflated valuations, once calling an $800 billion figure for SpaceX “too high.”

Supporters argue that hype around mega-IPOs, especially amid the ongoing AI fervor, fuels premature narratives that distract from core technical milestones, such as full Starship reusability and Starlink constellation expansion.

The incident reflects broader tensions in tech finance. Anonymous sourcing in valuation stories can drive market chatter and betting activity, yet it risks misinformation.

Bloomberg defended its reporting through multiple articles citing “people familiar with the matter,” but Musk’s blunt dismissal resonated widely on X, with users piling on to question media reliability.

Whether SpaceX ultimately goes public remains uncertain. Musk has teased an IPO tied to Starlink maturity, but priorities center on engineering breakthroughs over Wall Street timelines. For now, the $2 trillion figure joins a list of rumored milestones that Musk insists should be taken with skepticism.

Elon Musk

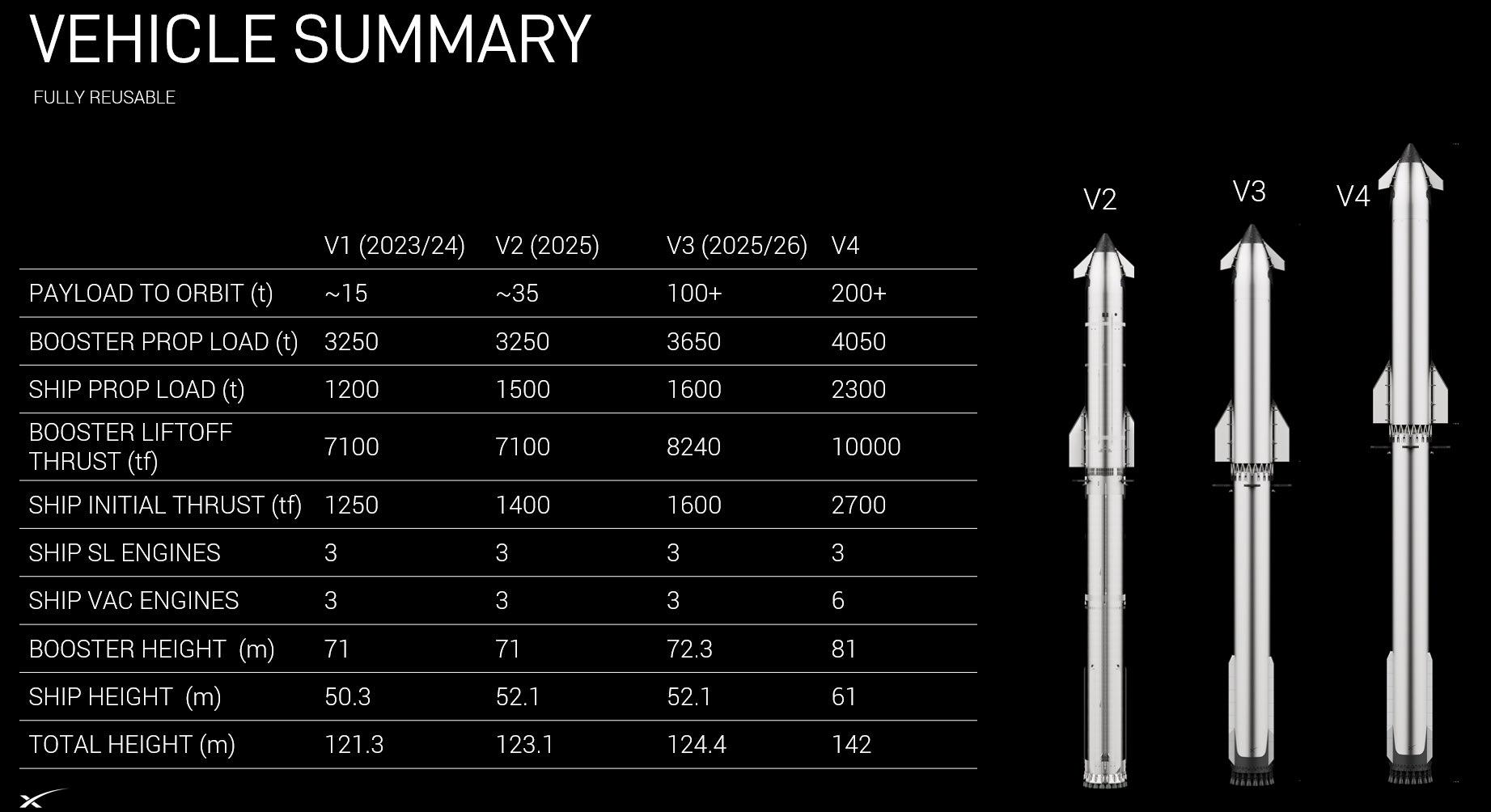

Elon Musk reveals date of SpaceX Starship v3’s maiden voyage

The announcement arrives after Flight 11 on October 13 of last year, which concluded a busy 2025 testing campaign. Since then, SpaceX has focused on ground testing, including cryoproofing of Ship 39 and preparations for Booster 19, the first V3 Super Heavy.

SpaceX CEO Elon Musk has revealed the timeline for the next Starship launch. It will be the first launch using SpaceX’s revamped design for Starship, as its v3 rocket will take its maiden voyage sooner than many might expect.

Musk announced on April 3 on X that the next Starship flight test, and the first flight of the upgraded v3 ship and booster, is 4 to 6 weeks away. The update signals the end of a nearly six-month hiatus since the program’s last launch.

Elon says the first V3 Starship launch will occur in 4-6 weeks

It will be the first Starship launch since Flight 11 on October 13, 2025 https://t.co/QnnYPTdbUu

— TESLARATI (@Teslarati) April 3, 2026

The upcoming mission, designated as Starship’s 12 integrated flight test (IFT-12), marks a significant milestone. It will be the debut of the v3 configuration, featuring a taller Super Heavy Booster and Starship upper stage. The changes SpaceX has made with the v3 rocket and booster are an increased propellant capacity and the more powerful Raptor 3 engines.

Earlier predictions from Musk in March had pointed to an April timeframe, but the latest timeline now targets a launch window in early to mid-May 2026.

The V3 iteration represents a substantial evolution from previous Starship prototypes. Engineers have optimized the design for improved manufacturability, higher thrust, and greater efficiency. Raptor 3 engines deliver significantly more power while reducing weight and production costs compared to earlier variants.

With these enhancements, SpaceX aims to boost payload capacity toward 200 metric tons to low Earth orbit in a fully reusable configuration — a dramatic leap from the roughly 35-ton target of prior versions. Such capabilities are critical for ambitious goals, including NASA’s Artemis lunar missions and eventual crewed flights to Mars.

The announcement arrives after Flight 11 on October 13 of last year, which concluded a busy 2025 testing campaign. Since then, SpaceX has focused on ground testing, including cryoproofing of Ship 39 and preparations for Booster 19, the first V3 Super Heavy.

Recent activities have involved static fires, activation of the new Pad 2 at Starbase in Boca Chica, Texas, and integration of Raptor 3 engines.

A prior incident with an early V3 booster on the test stand in late 2025 contributed to the delay, necessitating additional assembly and qualification work.

Musk’s timeline updates have become a hallmark of the Starship program, often described with characteristic optimism.

SpaceX’s Starship V3 is almost ready and it will change space travel forever

While past targets have occasionally shifted by weeks, the rapid iteration pace remains impressive. However, don’t be surprised if this timeline shifts again, as Musk has been overly optimistic in the past with not only launches, but products under his other companies, too.

SpaceX continues to refine launch infrastructure, including new propellant loading systems and tower mechanisms designed to support higher cadence operations. A successful V3 flight could pave the way for more frequent tests, tower catches of both booster and ship, and progression toward operational reusability.

The v3 debut is viewed as a transition point for Starship, moving beyond experimental flights toward a system capable of supporting large-scale deployment of Starlink satellites, lunar landers, and interplanetary transport.

Success on IFT-12 would demonstrate not only the new hardware’s performance but also SpaceX’s ability to recover from setbacks and maintain momentum.

As the 4-to-6-week countdown begins, anticipation builds at Starbase. Teams are finalizing vehicle stacking, conducting final pre-flight checks, and preparing for regulatory approvals. The world will be watching to see if Starship V3 can deliver on its promise of transforming humanity’s access to space.

Elon Musk

SpaceX to launch military missile tracking satellites through new Space Force contract

SpaceX wins a $178.5M Space Force contract to launch missile tracking satellites starting in 2027.

The U.S. Space Force awarded SpaceX a $178.5 million task order on April 1, 2026 to launch missile tracking satellites for the Space Development Agency. The contract, designated SDA-4, covers two Falcon 9 launches beginning in Q3 2027, one from Cape Canaveral Space Force Station in Florida and one from Vandenberg Space Force Base in California. The satellites, built by Sierra Space, are designed to bolster the nation’s ability to detect and track missile threats from orbit.

The award falls under the National Security Space Launch Phase 3 Lane 1 program, which Space Force uses to move payloads to orbit on faster timelines and at more competitive prices. “Our Lane 1 contract affords us the flexibility to deliver satellites for our customers, like SDA, more easily and faster than ever before to all the orbits our satellites need to reach,” said Col. Matt Flahive, SSC’s system program director for Launch Acquisition, in the official press release.

SpaceX is quietly becoming the U.S. Military’s only reliable rocket

The SDA-4 contract is the latest in a long string of national security wins for SpaceX. As Teslarati reported last month, the Space Force recently shifted a GPS III satellite launch from ULA’s Vulcan rocket to SpaceX’s Falcon 9 after a significant Vulcan booster anomaly grounded ULA’s military missions indefinitely. That move made it four consecutive GPS III satellites transferred to SpaceX after contracts were originally awarded to its competitor.

This didn’t come without a fight and dates back years. SpaceX originally had to sue the Air Force in 2014 for the right to compete for national security launches, at a time when United Launch Alliance held a near monopoly on the market. Since then, the company has steadily displaced ULA as the dominant provider, and last year the Space Force confirmed SpaceX would handle approximately 60 percent of all Phase 3 launches through 2032, worth close to $6 billion.

With missile defense satellites now part of its launch manifest alongside GPS, communications, and reconnaissance payloads, SpaceX is giving hungry investors something to chew on before its imminent IPO.

Elon Musk calls out $2 trillion SpaceX IPO valuation as ‘BS’

Elon Musk reveals date of SpaceX Starship v3’s maiden voyage