News

Tesla is taking gas cars off the road in huge numbers through trade-ins

Tesla revealed its trade-in statistics in the Q1 2021 Earnings Call Update Letter, showing that a majority of the vehicles it accepts through trade-in are gas-powered.

In the Update Letter that was released a few minutes after Wall Street closed up shop for the Monday trading session, Tesla revealed it had successfully accomplished another profitable quarter thanks to strong demand for its two mass-market vehicles, the Model 3 and Model Y. That, along with expanding production efforts, increasing gross margins, and decreasing manufacturing costs powered a positive quarter once again for the electric carmaker.

The fact of the matter is, however, that gas-powered cars are being displaced by electric vehicles. The market share for the automotive industry still remains heavily based on the production and sale of gas-powered vehicles, but electric cars are beginning to make their presence known. IHS Markit, a market analysis company, said that the overall presence of BEVs rose from .5% in 2019 to 1.2% in 2020. The firm forecasts global EV sales to rise by 70% this year.

With that being said, Tesla is undoubtedly the overall leader in EV sales by a single manufacturer. Statista broke down EV sales by manufacturer in 2020 via CleanTechnica, and Tesla had a commanding lead over second-place Volkswagen. Tesla sold 499,550 vehicles in 2020, Volkswagen sold 220,220 EVs.

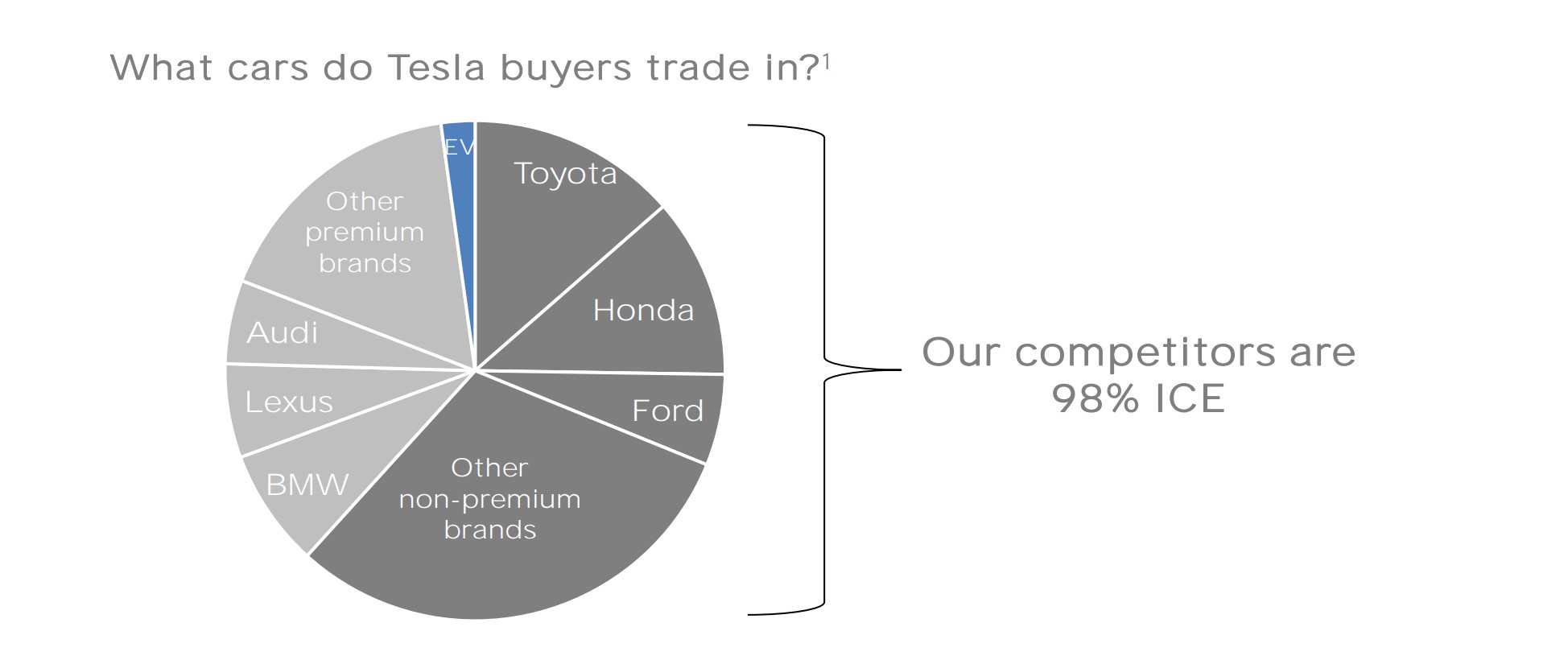

However, some of these sales, not all of them, were brought in by the need for a new car. According to a graphic that the automaker included in its Update Letter, gas-powered vehicles make up an overwhelming percentage of Tesla’s trade-ins: 98%.

Credit: Tesla

The graphic seems to reveal that nearly 60% of its trade-ins come from “non-premium brands,” including Toyota, Honda, Ford, and Chevrolet. Close to 40% of the company’s trade-ins are premium brands, like Audi, Lexus, BMW, and Mercedes-Benz. Only 2% of the trade-ins are EVs, proving the competition, in the simplest terms, is other gas vehicles and not other EVs.

Tesla wrote in its Update Letter:

“ICE vehicles comprised 97% of cars sold globally in 2020 and 98% of Tesla trade-ins. As more OEMs join our mission by launching EVs, we believe consumer confidence in EVs continues to increase, and more customers are willing to make the switch. Our Q1 order rate was the strongest in our history, and we are moving as quickly as possible to add more production capacity.”

-

-

It has always been Tesla’s goal to create more EVs on the road, and doing this requires the displacement of gas-powered cars. Tesla has been able to make their vehicles a more appealing option than gas-powered cars, and consumers are beginning to recognize the advantages that driving an EV has over driving a gas car. The increase in EV market share, which is led by Tesla’s domination of the sector, shows that more people are turning away from fossil fuels and looking toward electrification to solve their transportation needs.

In a new note to investors on Tuesday, Morgan Stanley analyst Andrew Percoco said that Tesla has one big financial question to answer for investors regarding its Robotaxi rollout, Full Self-Driving software, and Optimus.

Percoco said in the note that, for the most part, investors are still very positive about the direction the company is headed. However, there are some things the firm would like to see, and they have to do with financials.

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Tesla bulls are more than convinced that the company’s Full Self-Driving software is proof it can develop physical AI. Financially, however, there are still some questions, especially on elevated spending, which CEO Elon Musk said would occur as the company works to roll out Robotaxi faster and continue developing its Optimus robot.

The latter two are where Tesla will have to prove progress to investors, as Percoco writes that both projects “will require clearer evidence that Robotaxi is scaling and more tangible Optimus proof points to support the ROI on elevated capex.”

Percoco said the second quarter earnings call did not change his long-term thesis of where Tesla is positioned in the AI race, which is out in front. However, there are concerns that weaker gross margins and higher R&D spend will stress financials, and that has “sharpened our (and investors’) focus on measurable progress across Robotaxi and Optimus.”

Additionally, Robotaxi still needs to be proven with more operation in existing cities while maintaining safety but improving how many rides it gives in any given time, he said. For Optimus, Percoco wrote that he is “still looking for evidence beyond commentary around SOP.”

-

Morgan Stanley put Percoco in charge of covering Tesla after long-time analyst Adam Jonas transitioned to the automotive side.

Currently, Morgan Stanley has a $415 price target on Tesla and a ‘Hold’ rating on the stock. It is trading at around $330 at the time of publication, which was 2:30 P.M. on the East Coast.

SpaceX’s massive investment in AI will make it a big winner, Argus Research said after the company’s successful earnings call last week.

The firm also upgraded shares to a Buy from Hold and set a $160 price target.

SpaceX (NASDAQ: SPCX) is currently recovering from its heavy AI infrastructure investments, as it spent nearly $16 billion in Q2 alone. The company did this primarily by monetizing high-demand GPU compute capacity at a much faster pace than traditional data center economics would suggest.

Company CFO Bret Johnsen said that SpaceX would be able to pay back anything on new deployments within a year.

There are plenty of ways the company can do this:

Leasing excess compute capacity through contracts

SpaceX has already built Colossus and Colossus II, largely for its own model training. However, much of that capacity is already rented out to third parties. It already has major deals with Anthropic, Google, and Reflection AI. These partnerships are adding billions per month to SpaceX’s spreadsheet.

-

High utilization driven by industry-wide scarcity

The demand for advanced AI training and inference capacity continues to exceed what is available for use. SpaceX can fill new racks quickly after they come online, so the capital deployed converts into revenue with minimal idle time.

Additionally, management and outside observers have described the new compute capital as behaving more like a cost-of-goods-sold than traditional multi-year capex, especially because of this rapid monetization pattern.

Capacity has already scaled from ~0.4 GW a year to 1.4 GW annually by the end of Q2. There are targets of more than 2 GW by year-end.

High incremental margins on the rental business once capacity is online

GPU cloud providers often operate at strong gross margins. SpaceX can monetize capacity that was already partially built or can be added efficiently. This means that incremental EBITDA margins on the rental revenue are usually high. This accelerates cash recovery relative to the gross capital outlay.

Parallel monetization of its own AI software and applications

Beyond pure infrastructure rental, SpaceX also generates revenue from Grok through subscriptions and usage, from X through ads, data, and other related services, enterprise APIs, and the planned integration of the Cursor coding tools acquisition.

These application layers ride on the same compute infrastructure and provide additional high-margin streams that could offset build-out costs. AI-segment revenue overall rose sharply to about $2.6 billion in Q2, according to Motley Fool. This was driven primarily by the infrastructure contracts, but the software side is also partially responsible.

Efficient, large-scale deployment and vertical integration advantages

SpaceX has emphasized the rapid construction of power and cooling infrastructure and favorable cost-per-megawatt economics relative to industry benchmarks in some disclosures.

-

Combined with its ability to scale capacity aggressively and the fact that many contracts start generating revenue within months of capacity coming online, the effective payback compresses dramatically compared with more conventional multi-year data-center projects.

SpaceX’s dominant near-term recovery path will turn the AI clusters into a hyperscale-style compute rental business for other leading AI companies while still using a portion for internal models.

Tesla headlights have caused a recall of over 20,000 of the company’s two most popular vehicles, the Model 3 and Model Y, due to the low-beam bulb exceeding the maximum allowed intensity according to federal standards.

Tesla initiated the recall with the National Highway Traffic Safety Administration (NHTSA) this morning, stating that the low-beam output “exceeds the maximum allowed intensity in the outer upper-right and outer upper-left areas of the 10U and 90U zone, as prescribed in FMVSS No. 108.”

Tesla sourced the impacted headlights from Marelli Automotive Lighting, a Mexico-based company. The recall impacts 2020-2023 Model Y vehicles and 2017-2023 Model 3 vehicles. It is estimated that every VIN in this recall is impacted by the defect.

🚨 Tesla is recalling 20,349 2020-23 Model Y vehicles and 2017-23 Model 3 vehicles due to an excessively bright headlamp low beam.

Currently, there is no remedy plan in place, as it is still being developed. pic.twitter.com/y34cIO2U0B

— TESLARATI (@Teslarati) August 11, 2026

Typically, Tesla would remedy recalls of this nature through an Over-the-Air software update, which has been a major focus of criticism by the company and its supporters because the NHTSA still refers to it as a “recall,” even though it requires no action by the vehicle owner. The fix is shipped over the internet and downloaded to the car.

-

However, there appears to be a potentially different solution for this problem. Tesla has not developed a remedy for this issue, so it could potentially be on the way. The big issue appears to be the fact that these recalled lamps are out of production, and this is an old body style for both vehicles. The headlights and front-end designs are completely different.

Tesla switched to another supplier when the affected headlight design was discontinued. It plans to begin notifying owners of their remedy options by September 15.

Tesla filed a petition protesting the recall to fix the vehicles’ headlight issue, but the NHTSA denied it. Now, Tesla will come up with a solution to fix it.

Tesla has one big financial question to answer for investors: Morgan Stanley

SpaceX AI investment gamble will make it a big winner, firm says