Tesla (NASDAQ:TSLA) took a steep dive on the heels of the company’s Q4 and FY 2023 earnings call, dropping over 9% as of writing. With the company stating that volume growth would be tempered this year due to its focus on the next-generation platform and executives being quite vague about its guidance for 2024, analysts, including some TSLA bulls, are not happy.

Tesla actually had a record 2023, with vehicle sales growing nearly 40% year-over-year in 2023 to over 1.8 million units worldwide. Wall Street currently expects Tesla to post about 2.1 to 2.2 million vehicle sales for 2024, which would translate to a growth of about 20%. This number seems conservative and attainable enough, but Tesla simply maintained that its volume growth would be substantially lower than 2023’s ~40%.

Wedbush analyst Dan Ives shared his sentiments about Tesla’s earnings call, in a post on X. Ives described the call, which provided some high-level long-term views on the company, as another “train wreck” conference call. Following the earnings call, Ives adjusted his price target for Tesla from $350 to $315 per share, though he also noted that Wedbush remains bullish on the company.

Great to join @bsurveillance discussing another train wreck conf call in our view from Tesla and Musk lacking margin outlook and firm guidance for 24. Remain bullish for long term EV/AI vision but near term headwinds @lisaabramowicz1 @FerroTV @annmarie @BloombergTV https://t.co/E40CMG2Mg0— Dan Ives (@DivesTech) January 25, 2024

“We were dead wrong expecting Musk and team to step up like adults in the room on the call and give a strategic and financial overview of the ongoing price cuts, margin structure, and fluctuating demand. Instead, we got a high-level Tesla long-term view with another train wreck conference call,” Ives noted.

RBC analyst Tom Narayan also maintained his “Buy” rating on Tesla, though he lowered his price target from $300 to $297 per share. “We leave our delivery estimates unchanged after the vague guide, but lower our car gross margin expectations on less robust cost down opportunity,” he noted in a report. Narayan also pointed out that Tesla’s next-generation vehicle platform is still “many quarters away” from impacting the company’s numbers.

New $TSLA report from Adam Jonas: 5 thoughts post earnings call

“We reiterate our OW $TSLA rating ($345 price target) which offers over 80% upside from current levels which we believe is compelling in proportion to the investment level within our US auto coverage.” pic.twitter.com/TdZ2cLavdc— Sawyer Merritt (@SawyerMerritt) January 25, 2024

Morgan Stanley’s Adam Jonas, for his part, pointed out that Tesla almost did not provide any guidance during the call. He also observed that there were no “AI rabbits” pulled out of Tesla’s hat during the call, which was highlighted by Musk’s conservative comments about Dojo. Despite this, Morgan Stanley opted to maintain its “Overweight” rating and $345 price target on Tesla, with a bear case PT of $100 and a bull case PT of $500 per share.

While the sentiments surrounding Tesla’s Q4 and FY 2023 earnings call seem generally negative, some analysts opted to take a more optimistic stance on the company. Canaccord lowered its price target for Tesla from $267 to $234 per share, though the firm also noted that it is time for investors to be patient about the company. The firm noted that it remains bullish about Tesla’s long-term prospects.

NEWS: Canaccord Genuity has lowered its $TSLA price target to $234 (from $267), maintains a BUY rating.

They put out a good note:

“It’s time to be patient. The next-generation vehicle, FSD upgrades, margin improvement, and Optimus will likely bring an acceleration in revenue…— Sawyer Merritt (@SawyerMerritt) January 25, 2024

“It’s time to be patient. The next-generation vehicle, FSD upgrades, margin improvement, and Optimus will likely bring an acceleration in revenue growth. But not this year — 2024 will be subdued; probably a trough, but still relatively slow (we model ~18% y\y revenue growth). Growth curves are seldom smooth, and Tesla is no different.

“We are still quite bullish on Tesla’s long-term growth prospects. We think EVs will replace ICE vehicles despite recent countervailing narratives. We see vehicle autonomy as one of the highest value-creating technologies to be deployed. Ever. And Tesla, with its razor/ razorblade approach, is a leader in this real-world AI. We think Tesla is Apple on steroids as it focuses on manufacturing and a higher level of vertical integration. Tesla is THE sustainability behemoth, in our opinion,” the firm noted.

The critical metric, auto gross margins ex credits, came in at 17%, compared to the Street at 17.3%. I was expecting 16.7%.

While this missed the Street, it marks the end of four consecutive quarters of margin decline, up from 16.3% in the Sep-23.

Over this is a positive.— Gene Munster (@munster_gene) January 24, 2024

Longtime Tesla bull Gene Munster of Deepwater Asset Management also pointed out that Tesla’s auto gross margins for the past quarter ended a streak of dropping margins. “The critical metric, auto gross margins ex credits, came in at 17%, compared to the Street at 17.3%. I was expecting 16.7%. While this missed the Street, it marks the end of four consecutive quarters of margin decline, up from 16.3% in the Sep-23. Over, this is a positive,” Munster wrote on X.

Don’t hesitate to contact us with news tips. Just send a message to simon@teslarati.com to give us a heads up.

Elon Musk

Tesla Supercharger Diner food menu gets a sneak peek as construction closes out

What are you ordering at the Tesla Diner?

The Tesla Supercharger Diner in Los Angeles is nearing completion as construction appears to be winding down significantly. However, the more minor details, such as what the company will serve at its 50s-style diner for food, are starting to be revealed.

Tesla’s Supercharger Diner is set to open soon, seven years after CEO Elon Musk first drafted the idea in a post on X in 2018. Musk has largely come through on most of what he envisioned for the project: the diner, the massive movie screens, and the intended vibe are all present, thanks to the aerial and ground footage shared on social media.

We already know the Diner will be open 24/7, based on decals placed on the front door of the restaurant that were shared earlier this week. We assume that Tesla Optimus will come into play for these long and uninterrupted hours.

The Tesla Diner is basically finished—here’s what it looks like

As far as the food, Tesla does have an email also printed on the front door of the Diner, but we did not receive any response back (yet) about what cuisine it will be offering. We figured it would be nothing fancy and it would be typical diner staples: burgers, fries, wings, milkshakes, etc.

According to pictures taken by @Tesla_lighting_, which were shared by Not a Tesla App, the food will be just that: quick and affordable meals that diners do well. It’s nothing crazy, just typical staples you’d find at any diner, just with a Tesla twist:

Tesla Diner food:

• Burgers

• Fries

• Chicken Wings

• Hot Dogs

• Hand-spun milkshakes

• And more https://t.co/kzFf20YZQq pic.twitter.com/aRv02TzouY— Sawyer Merritt (@SawyerMerritt) July 17, 2025

As the food menu is finalized, we will be sure to share any details Tesla provides, including a full list of what will be served and its prices.

Additionally, the entire property appears to be nearing its final construction stages, and it seems it may even be nearing completion. The movie screens are already up and showing videos of things like SpaceX launches.

There are many cars already using the Superchargers at the restaurant, and employees inside the facility look to be putting the finishing touches on the interior.

🚨 Boots on the ground at the Tesla Diner:

— TESLARATI (@Teslarati) July 17, 2025

It’s almost reminiscent of a Tesla version of a Buc-ee’s, a southern staple convenience store that offers much more than a traditional gas station. Of course, Tesla’s version is futuristic and more catered to the company’s image, but the idea is the same.

It’s a one-stop shop for anything you’d need to recharge as a Tesla owner. Los Angeles building permits have not yet revealed the date for the restaurant’s initial operation, but Tesla may have its eye on a target date that will likely be announced during next week’s Earnings Call.

News

Tesla’s longer Model Y did not scale back requests for this vehicle type from fans

Tesla fans are happy with the new Model Y, but they’re still vocal about the need for something else.

Tesla launched a slightly longer version of the Model Y all-electric crossover in China, and with it being extremely likely that the vehicle will make its way to other markets, including the United States, fans are still looking for something more.

The new Model Y L in China boasts a slightly larger wheelbase than its original version, giving slightly more interior room with a sixth seat, thanks to a third row.

Tesla exec hints at useful and potentially killer Model Y L feature

Tesla has said throughout the past year that it would focus on developing its affordable, compact models, which were set to begin production in the first half of the year. The company has not indicated whether it met that timeline or not, but many are hoping to see unveilings of those designs potentially during the Q3 earnings call.

However, the modifications to the Model Y, which have not yet been officially announced for any markets outside of China, still don’t seem to be what owners and fans are looking forward to. Instead, they are hoping for something larger.

A few months ago, I reported on the overall consensus within the Tesla community that the company needs a full-size SUV, minivan, or even a cargo van that would be ideal for camping or business use.

Tesla is missing one type of vehicle in its lineup and fans want it fast

That mentality still seems very present amongst fans and owners, who state that a full-size SUV with enough seating for a larger family, more capability in terms of cargo space for camping or business operation, and something to compete with gas cars like the Chevrolet Tahoe, Ford Expedition, or electric ones like the Volkswagen ID.BUZZ.

We asked the question on X, and Tesla fans were nearly unanimously in support of a larger SUV or minivan-type vehicle for the company’s lineup:

🚨 More and more people are *still* saying that, despite this new, longer Model Y, Tesla still needs a true three-row SUV

Do you agree? https://t.co/QmbRDcCE08 pic.twitter.com/p6m5zB4sDZ

— TESLARATI (@Teslarati) July 16, 2025

Here’s what some of the respondents said:

100% agree, we need a larger vehicle.

Our model Y is quickly getting too small for our family of 5 as the kids grow. A slightly longer Y with an extra seat is nice but it’s not enough if you’re looking to take it on road trips/vacations/ kids sports gear etc.

Unfortunately we…

— Anthony Hunter (@_LiarsDice_) July 17, 2025

Had to buy a Kia Carnival Hybrid because Tesla doesn’t have a true 3 row vehicle with proper space and respectable range. pic.twitter.com/pzwFyHU8Gi

— Neil, like the astronaut (@Neileeyo) July 17, 2025

Agreed! I’m not sure who created this but I liked it enough to save it. pic.twitter.com/Sof5nMehjS

— 🦉Wise Words of Wisdom – Inspirational Quotes (IQ) (@WiseWordsIQ) July 16, 2025

Tesla is certainly aware that many of its owners would like the company to develop something larger that competes with the large SUVs on the market.

However, it has not stated that anything like that is in the current plans for future vehicles, as it has made a concerted effort to develop Robotaxi alongside the affordable, compact models that it claims are in development.

It has already unveiled the Robovan, a people-mover that can seat up to 20 passengers in a lounge-like interior.

The Robovan will be completely driverless, so it’s unlikely we will see it before the release of a fully autonomous Full Self-Driving suite from Tesla.

Energy

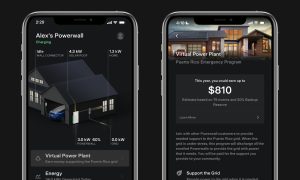

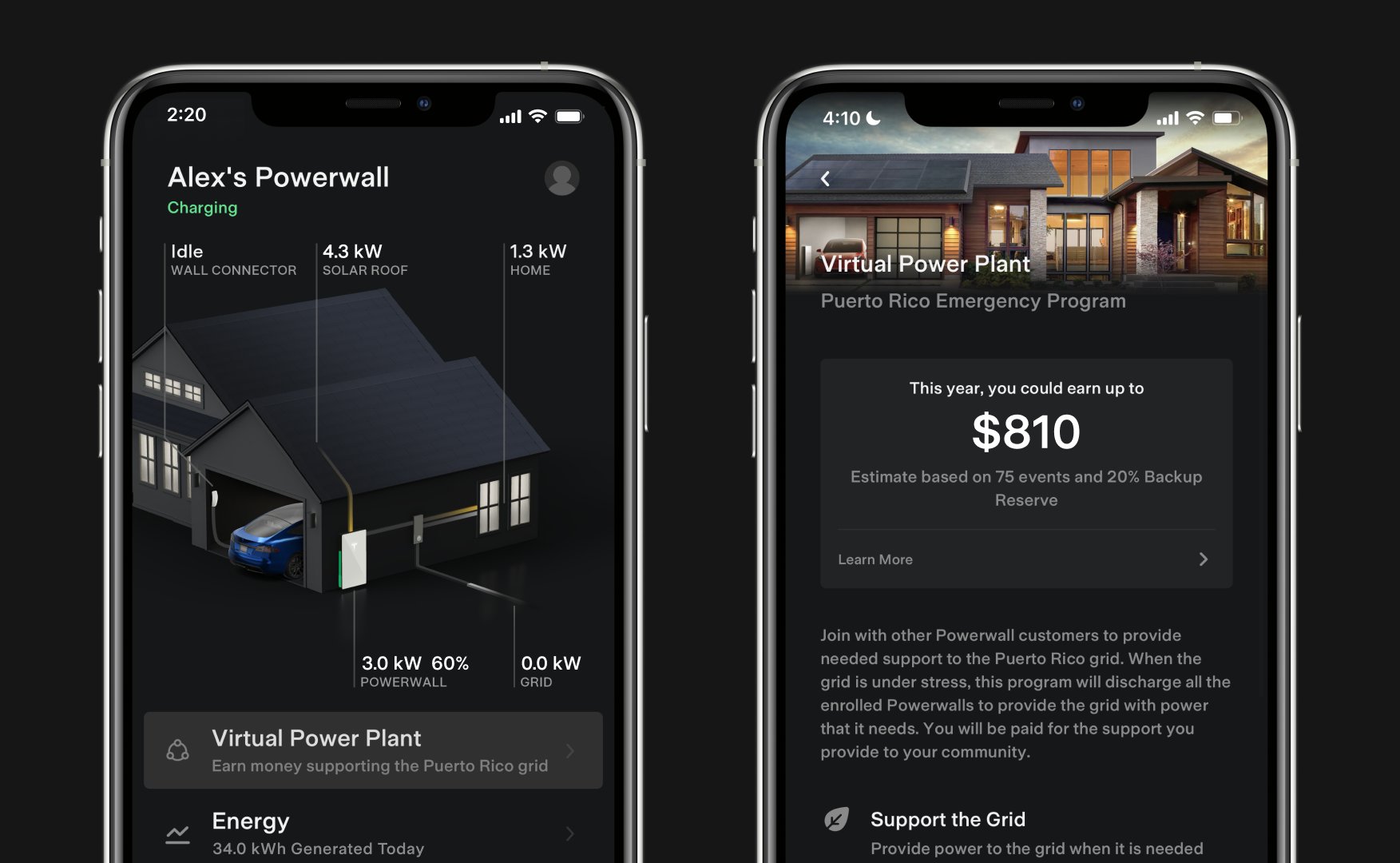

Tesla launches first Virtual Power Plant in UK – get paid to use solar

Tesla has launched its first-ever Virtual Power Plant program in the United Kingdom.

Tesla has launched its first-ever Virtual Power Plant program in the United Kingdom. This feature enables users of solar panels and energy storage systems to sell their excess energy back to the grid.

Tesla is utilizing Octopus Energy, a British renewable energy company that operates in multiple markets, including the UK, France, Germany, Italy, Spain, Australia, Japan, New Zealand, and the United States, as the provider for the VPP launch in the region.

The company states that those who enroll in the program can earn up to £300 per month.

Tesla has operated several VPP programs worldwide, most notably in California, Texas, Connecticut, and the U.S. territory of Puerto Rico. This is not the first time Tesla has operated a VPP outside the United States, as there are programs in Australia, Japan, and New Zealand.

This is its first in the UK:

Our first VPP in the UK

You can get paid to share your energy – store excess energy in your Powerwall & sell it back to the grid

You’re making £££ and the community is powered by clean energy

Win-win pic.twitter.com/evhMtJpgy1

— Tesla UK (@tesla_uk) July 17, 2025

Tesla is not the only company that is working with Octopus Energy in the UK for the VPP, as it joins SolarEdge, GivEnergy, and Enphase as other companies that utilize the Octopus platform for their project operations.

It has been six years since Tesla launched its first VPP, as it started its first in Australia back in 2019. In 2024, Tesla paid out over $10 million to those participating in the program.

Participating in the VPP program that Tesla offers not only provides enrolled individuals with the opportunity to earn money, but it also contributes to grid stabilization by supporting local energy grids.

Tesla Supercharger Diner food menu gets a sneak peek as construction closes out

Tesla’s longer Model Y did not scale back requests for this vehicle type from fans

Tesla launches first Virtual Power Plant in UK – get paid to use solar

-

Elon Musk1 day ago

Elon Musk1 day agoWaymo responds to Tesla’s Robotaxi expansion in Austin with bold statement

-

News1 day ago

News1 day agoTesla exec hints at useful and potentially killer Model Y L feature

-

Elon Musk2 days ago

Elon Musk2 days agoElon Musk reveals SpaceX’s target for Starship’s 10th launch

-

Elon Musk3 days ago

Elon Musk3 days agoTesla ups Robotaxi fare price to another comical figure with service area expansion

-

News1 day ago

News1 day agoTesla’s longer Model Y did not scale back requests for this vehicle type from fans

-

News1 day ago

News1 day ago“Worthy of respect:” Six-seat Model Y L acknowledged by Tesla China’s biggest rivals

-

News2 days ago

News2 days agoFirst glimpse of Tesla Model Y with six seats and extended wheelbase

-

Elon Musk2 days ago

Elon Musk2 days agoElon Musk confirms Tesla is already rolling out a new feature for in-car Grok