News

Tesla stock (TSLA) could double thanks to edge in battery tech: Wall St veteran

Gary Black, a private investor who was once considered as one of Wall Street’s most prominent analysts in the tobacco industry, believes he has found the reason why Tesla stock (NASDAQ:TSLA) continues to climb. According to the finance veteran, a lot of it has to do with the company’s battery technology that just so happens to be head and shoulders above the competition.

On Thursday, Tesla’s stock ended the day at $404.04 a share, giving the company a $73 billion market value. Both of these are records for the electric car maker, and there may be more upside if the company meets its delivery and production targets this fourth quarter. That being said, Black noted in a statement to Barron’s that a lot of Tesla’s momentum is due to the company’s batteries, which give its vehicles like the Model S their industry-leading range.

“When you talk to dealers and non-EV users, the biggest obstacle to buying an EV is battery charge. People want the most range,” Black said.

Recent electric car releases from veteran automakers have only emphasized Tesla’s lead in efficiency and range. A Model 3 Standard Range Plus, for example, starts at $39,990 and offers 250 miles of emission-free driving. On the other hand, a Porsche Taycan Turbo, which costs about $150,000, will only offer 201 miles of range as per estimates from the EPA. That’s 20% less range for the Taycan at over three times the cost of the Model 3 Standard Range Plus.

While a longtime short thesis against Tesla argues that the young company will be buried by electric cars from more experienced rivals, Black remains confident that Tesla will continue to thrive. The veteran noted that Mercedes has delayed the release of its electric car, the EQC, in the United States. Meanwhile, Jaguar and Audi’s battery-powered vehicles have lagged in sales. Part of this is likely due to the vehicles’ range, as well as their lack of a dedicated charging infrastructure like Tesla’s Supercharger Network.

Considering its lead in battery tech, Black believes that Tesla’s sales could hit 1.8 million units annually by 2024. This would equate to around 10% of the United States car market and $8 billion in earnings before interest, taxes or depreciation. This also means that TSLA stock could double to about $800 per share in 2024. “I’m a value investor but I like to buy growth companies at a discount to intrinsic value,” Black said.

This becomes particularly feasible when Tesla’s constant improvements to its battery tech are taken into account. President of Automotive Jerome Guillen previously stated that Tesla’s batteries are never static, as they are always in a constant state of improvement. The company has been pretty secretive about the details of its latest battery tech innovations, but the unveiling of vehicles like the Cybertruck, whose top-tier variant goes over 500 miles of range for a price that’s less than $70,000, suggests that these improvements are significant.

-

-

Tesla currently holds 78% of the electric vehicle market in the United States. Black believes that with competition steadily increasing, the company must be prepared to see its overall presence in the market drop to around 40%. He thinks that drivers who currently utilize electric cars will eventually grow from 3% to 25% of the market, equivalent to 1.8 million battery-powered vehicles on the road. Nevertheless, if competition continues to be as anemic as it has been so far, Tesla may end up holding on to its dominant market share in the US’ EV industry longer than expected.

Disclosure: I have no ownership in shares of TSLA and have no plans to initiate any positions within 72 hours.

-

-

Elon Musk

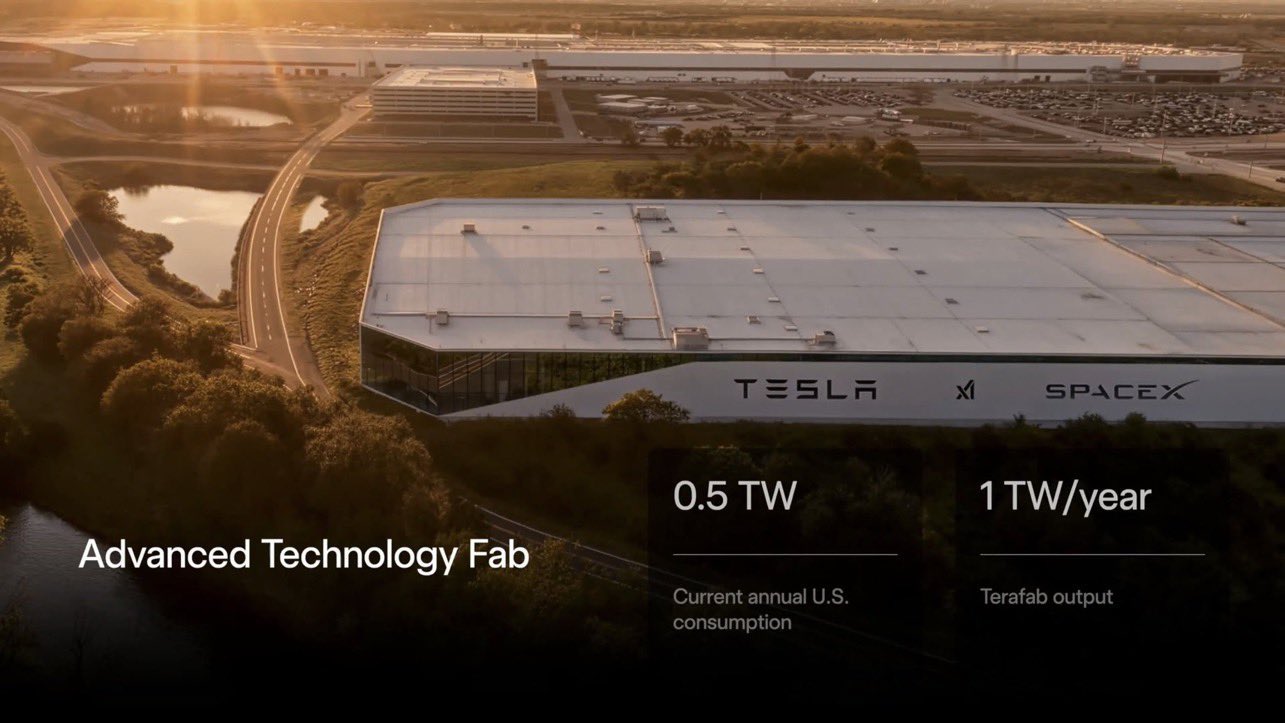

Space finally faced the people living next to its next Terafab mega-project

SpaceX confirmed Terafab’s Grimes County site is locked in, with construction starting within months.

SpaceX and Terafab representatives sat across from Grimes County residents for the first time on Wednesday, telling a packed Commissioners Court room that the $55 billion chip manufacturing project is now a done deal at the Gibbons Creek Reservoir site.

The meeting followed a $10 million check SpaceX sent the county earlier this week, satisfying a payment deadline built into the tax abatement agreement both sides signed in June. Elon Musk shared a post on X confirming the payment, and County Judge Joe Fauth told the San Antonio Express-News his office deposited the check after it beat its deadline.

Wednesday’s session, first reported by KBTX, moved the project from paperwork to construction. Terafab representative Riley Trennell told residents the JETI tax break agreements with Iola ISD and Anderson-Shiro CISD are signed and active, and that civil work and foundation prep are starting almost immediately. Renderings of the facility could be released within days, he said, with construction beginning within months.

Elon Musk launches TERAFAB: The $25B Tesla-SpaceXAI chip factory that will rewire the AI industry

Musk first announced Terafab in March as a joint venture between Tesla, SpaceX and xAI aimed at producing over a terawatt of AI compute annually, an amount that dwarfs the roughly 20 gigawatts the entire global chip industry produces today. Intel joined as a manufacturing partner in April. Musk has said the project needed its own day in the spotlight rather than being squeezed into an earnings call, and for months the Grimes County site remained unconfirmed even as reporting pointed there.

SpaceX attorney Buck Brannon used Wednesday’s meeting to note that the company’s abatement is roughly 78 percent, not the 100 percent some earlier reports suggested. In exchange, SpaceX will pay Grimes County a fixed $20 million a year for 35 years, a total of $710 million, which Brannon said exceeds the $14 million Tesla paid Travis County in 2025.

SpaceX also addressed environmental concerns that have followed the project since Musk’s Terafab partnership with Intel was announced. Representatives said Terafab will not raise electric bills for other ratepayers, will not deplete local water supplies and will not draw down the Navasota River. SpaceX confirmed it owns the Navasota River pumping station, which it plans to use to divert stormwater into the Gibbons Creek Reservoir, and said it will build its own natural gas plants to power the facility rather than pulling from the ERCOT grid.

Grimes County commissioners also approved an addendum letting county employees use ten approved AI chatbots for work, including Grok.

Elon Musk has declared that SpaceX has effectively solved one of Starship’s most persistent engineering challenges: the reliability of its heat shield tiles.

During the company’s first-ever Earnings Call, the SpaceX CEO stated:

“I don’t want to jinx it or anything, but I think I would call the heat shield problem solved at this point. All indications from data and visual inspection is we have solved it. That doesn’t mean we won’t make improvements, but we do not see any technical obstacles to achieving rapid reusability at this point.”

Starship’s heat shield consists of roughly 18,000 hexagonal ceramic tiles covering the windward side of the upper stage. These tiles form the thermal protection system that shields the vehicle’s stainless-steel structure from the extreme heat of atmospheric reentry.

Elon says he believes the heat shield problem with Starship is currently solved.

He called it “arguably the single biggest problem” pic.twitter.com/eEE9vM5zlz

— TESLARATI (@Teslarati) August 4, 2026

During descent, atmospheric friction generates temperatures exceeding several thousand degrees Celsius and creates plasma flows capable of melting unprotected metal. The tiles absorb, radiate, and insulate against this energy, allowing the vehicle to survive and potentially fly again. Without a durable heat shield, full and rapid reusability, the cornerstone of Starship’s design for frequent launches, satellite deployments, and deep-space missions, would remain impossible.

The tiles have long been a source of difficulty. On earlier test flights, a significant number of tiles detached during ascent due to vibration, aerodynamic loads, and imperfect attachment methods using pins and adhesives. Gaps between tiles allowed hot plasma to infiltrate, causing secondary damage and hot spots on the underlying structure.

These issues echoed challenges faced by NASA’s Space Shuttle, whose ceramic tiles required extensive, labor-intensive inspections and replacements between missions, preventing rapid turnaround. SpaceX has iteratively improved materials, standardized tile shapes, refined attachment techniques, added secondary ablative layers, and tested sealing methods such as “crunch wrap” felt to close gaps.

Progress was visible across Flights 10–12, with steadily better tile retention, yet questions remained about whether the system could support the minimal-refurbishment goal of rapid reuse.

Flight 13 on July 24 provided the decisive evidence. Ship 40 flew a deliberately more demanding profile with higher dynamic pressure to stress the heat shield beyond typical operational loads. It successfully deployed 20 operational Starlink V3 satellites, the first such payload on a Starship mission, performed an in-space Raptor engine relight, and executed a controlled reentry.

Elon Musk sheds two new bits of detail on Starship after 13th test launch

Cameras on six of the satellites and onboard sensors captured extensive imagery and data of the shield throughout the flight. The ship then achieved its softest splashdown to date in the Indian Ocean, remaining intact and floating rather than breaking apart or exploding as on prior missions. This allowed drone inspections and continuous telemetry of the heat shield in near-real time.

Post-flight analysis showed the majority of tiles remaining attached with only minor damage and limited plasma streaking at seams. Musk noted that the mission delivered “all the heat shield data we needed and then some.” Combined with visual inspections, these results underpinned his subsequent assessment that the core technical barriers to rapid reusability have been cleared. While refinements will continue, Flight 13 marked a pivotal step toward Starship’s operational future.

SpaceX COO Gwynne Shotwell outlined ambitious plans for Starlink Mobile during the company’s August 4 Earnings call, signaling a direct challenge to U.S. wireless giants like AT&T, T-Mobile, and Verizon.

Shotwell noted that the three companies generate roughly $600 billion in combined annual revenue. “I anticipate us to be able to acquire quite a few of their customers because I think our service will be better,” she said. “We will eliminate dead zones leveraging the satellites in orbit. It will be better during any natural disaster… I’m quite excited about Starlink Mobile.”

SpaceX President & COO Gwynne Shotwell on @Starlink Mobile and its impact on Verizon, AT&T and T-Mobile:

“Roughly, between them, $600 billion a year. I anticipate us to be able to acquire quite a few of their customers. Our service will be better. We will eliminate dead zones… pic.twitter.com/UYZUkrGc0L

— Sawyer Merritt (@SawyerMerritt) August 4, 2026

SpaceX intends to combine its satellite constellation with terrestrial infrastructure. The company has acquired about 65 MHz of spectrum from EchoStar and plans to deploy next-generation Starlink Mobile satellites in 2027, with upgraded service targeted for the end of that year.

Shotwell described the enhanced network, leveraging more satellites and spectrum, as potentially “100 times better” than the current direct-to-cell offering, which already supports basic texting and app-based voice/video in coverage gaps through partnerships. She also indicated plans for low-cost cellular base stations that could integrate with existing Starlink dishes, creating a hybrid system for broader capacity in urban, suburban, and rural areas.

For the general public, Starlink Mobile promises significant advantages. Satellite connectivity can fill gaps where traditional cell towers fail, delivering service in remote locations, mountains, or during outages caused by storms, wildfires, or infrastructure damage—conditions in which ground networks often collapse.

Users could enjoy more consistent coverage without relying solely on dense tower builds, potentially at competitive prices as SpaceX scales. The hybrid approach aims to support full mobile services, including higher-speed data, while working with unmodified smartphones over time.

These developments revive long-standing but unfounded rumors of a Musk-developed “Tesla phone.” Speculative claims of a “Pi Phone” or similar device with built-in Starlink connectivity have circulated for years on social media, often featuring fabricated images and details. Elon Musk has repeatedly denied any such plans, stating Tesla has no intention of entering the smartphone market unless forced by extreme circumstances with app stores.

No official product, filings, or development announcements have ever materialized; the rumors remain hoaxes.

The announcement quickly pressured telecom stocks. Shares of AT&T, Verizon, and T-Mobile fell between roughly 2 and 4 percent in after-hours and premarket trading as investors weighed the competitive threat from a hybrid satellite-terrestrial network.

While execution challenges remain—spectrum deployment, infrastructure rollout, and regulatory hurdles—Shotwell’s remarks mark SpaceX’s clearest signal yet of entering the consumer mobile market as a full competitor.

Space finally faced the people living next to its next Terafab mega-project

SpaceX has solved Starship’s biggest challenge, Elon Musk says