Investor's Corner

Tesla Gigafactory 3 buildout sees more roof paving and potential stamping area

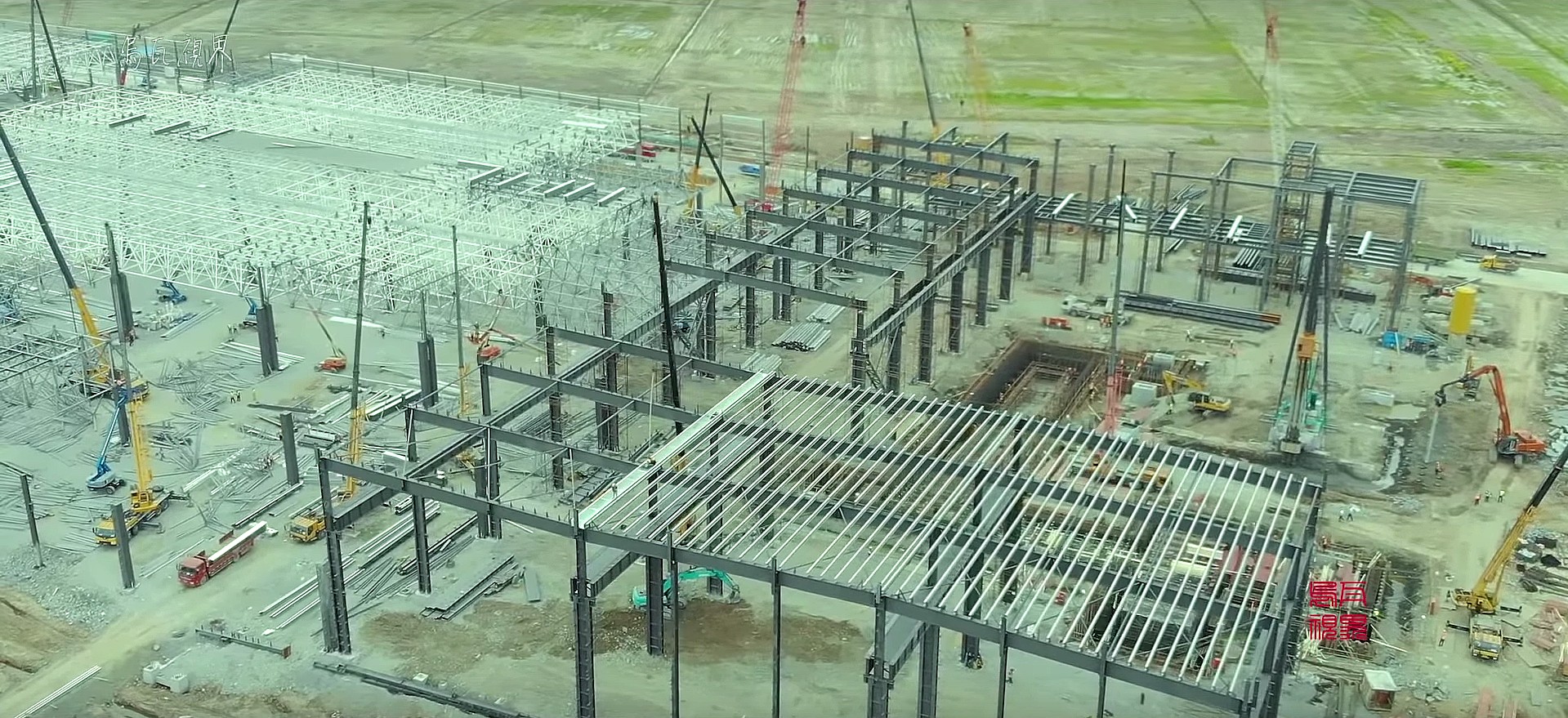

The construction of Tesla’s Gigafactory 3 in China continues to show rapid progress, with numerous workers on the site seemingly focusing on paving large sections of the upcoming general assembly building’s roof. Work in taller sections of the facility also hints at the construction of what could very well be Gigafactory 3’s stamping area.

Previous flyovers of the Gigafactory 3 lot conducted by China-based drone operator Wuwa Vision (烏瓦) revealed that roof trusses are being built in several sections of the site. The operator’s latest video shows that these sections have spread significantly to other areas of the factory, and more of the finished trusses are now being paved. Looking at the roofing of Gigafactory 3 from the air, one cannot help but see similarities to Gigafactory 1 in Nevada when its roofing was under construction.

While most of the work on the site filmed by the drone operator revealed a particular focus on Gigafactory 3’s roof, other areas of the Phase 1 project are beginning to look more refined as well. The taller sections of the facility, which are represented by a steel framework that is several stories high, now look more detailed. Heavy equipment have also been deployed in the area.

Neither Tesla nor its construction partner in China has announced exactly what these taller areas will be once the Phase 1 buildout is complete, but speculations among the Tesla community suggest that the section might be allotted for stamping considering its size and height. Excavations are even underway in the area, possibly to make enough space for heavy presses, which are large machines that require a lot of space.

The recent flyover of Gigafactory 3 ultimately shows a project that is starting to look more and more like a car factory. This is impressive, particularly as work on the Gigafactory 3 buildout started only a few months ago. Elon Musk attended the groundbreaking event for the facility in early January, and since then, Tesla and its construction partner have transformed a section of a large, muddy field into an industrial area where an impressive electric car factory is taking shape.

The speed of Gigafactory 3’s buildout is already pretty insane by Western standards, but work on the facility might get even more expedited in the coming weeks. Last month, Shanghai official Chen Mingbo called for the Phase 1 buildout to be finished in May, which is just a few weeks from today. Once Phase 1 is complete, Tesla is expected to start preparing the site for the installation of electric car manufacturing equipment. Tesla Model 3 production at Gigafactory 3 is expected to begin sometime this year.

Watch Gigafactory 3’s latest progress in the video below.

Elon Musk

SpaceX Starship Flight 13 aborted at Zero and Musk just told us what broke

Four Raptor engines failed to ignite at T-zero, forcing SpaceX to scrub Starship Flight 13 Thursday.

SpaceX scrubbed the Starship Flight 13 launch attempt Thursday evening at the last possible moment, after four of the Super Heavy booster’s 33 Raptor 3 engines failed to ignite during the startup sequence. The 90-minute window had opened at 6:45 p.m. EDT from Starbase in Boca Chica, Texas, and the countdown had proceeded without issue all day, with more than 11.5 million pounds of liquid methane and liquid oxygen being fully loaded into the rocket before the automated abort triggered. SpaceX’s launch directors posted on X, “Standing down from today’s flight test attempt,” and shut down the livestream shortly after.

Musk confirmed the root cause within hours. “Some of the engines didn’t start, triggering an automatic launch abort,” he wrote on X. “To be confident of a good flight, 2 Raptors will be removed and replaced. Most probable launch timing is early next week.” SpaceX engineers began draining propellant tanks immediately and Booster 20 was rolled back to its hangar for inspection.

The timing adds a layer of significance that did not exist during any of the previous 12 Starship flights. This is the first time SpaceX has attempted to launch Starship since the company made its stock market debut in June, listing under ticker SPCX at $135 per share. Public investors are now watching every Starship outcome in real time, and a last-second abort carries more visibility than it would have six months ago.

Flight 13 was designed to be one of the most consequential tests in the program’s history. It was set to carry 20 Starlink V3 satellites, the first operational payload Starship has ever attempted to deploy. Six of those satellites carried external cameras to photograph Starship’s heat shield from the outside during flight, which would act as a self-inspection approach SpaceX has never attempted before. The mission also needed to complete a Raptor engine relight in space, a step SpaceX skipped on Flight 12 in May after losing an engine during ascent. That Flight 12 booster also flipped 90 degrees off course during its boostback burn when five engines failed to reignite.

SpaceX has not announced an official next launch date. Musk’s “early next week” window points to July 21 or 22 at the earliest, pending the engine swap and a return to the pad.

Lucid CEO Silvio Napoli responded to rumors of an imminent bankruptcy that was reportedly being mulled after a report stated the automaker was working with the firm AlixPartners to iron out its next steps.

The company felt a massive loss on Wall Street yesterday, as the report essentially pushed the stock down as much as 55 percent on Tuesday.

The report, published initially by Eletric-Vehicles.com, claimed Lucid was essentially in dire straits and was told by AlixPartners, a commonly used restructuring advisor, to either take shares private or file for Chapter 11 bankruptcy protection.

Lucid’s head of Communications, Nick Twork, immediately challenged the report and stated the company “has sufficient liquidity to carry its operations well into next year.”

Now, the company’s CEO is chiming in as well, stating that the report is “so far from the facts that they require a direct response.”

Napoli said:

“Lucid is not considering bankruptcy or a transaction to take the company private. Those reports are false. The Board did not explore either scenario. Period.

As disclosed in our most recent quarterly filing, Lucid has sufficient liquidity to fund its operations well into next year.

We work with outside advisors to improve operational performance and execution. They are not advising Lucid on a take-private transaction or bankruptcy, and any suggestion that they have recommended either course of action to management or the Board is false.

My priority is clear: turn this company around. That is where the leadership team and I are focused.

I look forward to providing a full update during our quarterly earnings call on August 4th.”

🚨 Lucid CEO Silvio Napoli calls rumors of financial issues “so far from the facts that they require a direct response.”

Read his full remarks here: https://t.co/t3Pg1NHvzy pic.twitter.com/LvHUPhO4Qf

— TESLARATI (@Teslarati) July 15, 2026

It seems pretty clear that Lucid is confident things will be okay, and, to be honest, they should not have much to worry about, especially considering the company has been backed by the Saudi Public Investment Fund (PIF) for years. It has solid financial backing, and its sales, while weak, are pretty much right on par with a company of this age.

Lucid also sent a Cease & Desist letter to the publication for their report.

Lucid shares have rebounded nicely and are up nearly 21 percent at the time of publication. As soon as the company dispelled the rumors of bankruptcy yesterday, the stock began to climb back toward more reasonable levels.

Electric vehicle maker Lucid Group has denied rumors of an imminent bankruptcy after a report from this morning sent the stock on a dramatic drop on Wall Street, seeing losses of more than 40 percent during trading hours.

Lucid’s Director of Communications, Nick Twork, responded to the report from Eletric-Vehicles.com, which stated the company’s restructuring advisor, AlixPartners, was asked to review two decisions: taking Lucid shares private or filing for Chapter 11 bankruptcy protection.

The report also claims AlixPartners told the Lucid board to “concentrate on Gravity production while improving its quality, and to temporarily hold back the Lucid Air, the sedan that has defined the company since its launch.”

Twork said:

$LCID The rumors are completely false. The company has sufficient liquidity to carry its operations well into next year, as recently published in its last quarterly filings, and it has not formed any special Board committee to explore the scenarios reported today. Our focus is…

— Nick Twork (@ntwork) July 14, 2026

Shares rebounded after the response to the report, halving its losses as the trading day neared 3 p.m. Eastern.

Lucid has struggled to get its sales off the ground and into more respectable numbers, but the company is in its early years, when things are hard to begin with. It is also backed by several notable investors, including the Saudi Public Investment Fund (PIF), which has nearly limitless money and likely would not ditch an investment of this size so soon.

Lucid shares were down just 14 percent at the time of publication, a far cry from the 55 percent its losses topped out at during the day.

SpaceX Starship Flight 13 aborted at Zero and Musk just told us what broke

Elon Musk secretly acquires $1B energy company to power the AI future