Investor's Corner

Tesla could see a ~40% rally, but that doesn’t mean it’s a ‘Buy,’ claims analyst

In a rather interesting episode of CNBC‘s Trading Nation, Oppenheimer technical analyst Ari Wald mentioned that Tesla stock (NASDAQ:TSLA) could be poised to see some recovery. Despite this, the analyst mentioned during his segment that he does not consider Tesla stock a “Buy.”

The Oppenheimer analyst argued that Tesla stock has been notably volatile to the point where its price direction is nearly aimless. In the past 12 months alone, Tesla shares swung from prices as high as $387 per share to as low as $244.59 per share. With $250 being a big support range level, Wald estimated that TSLA shares could swing back to $360 per share.

“This is one we’ve been on the sidelines with, avoiding both on the long end and short side, just given how directionless and choppy it’s been, and that’s still the case. It’s paid to buy it when it’s ugly and sell it when it starts to look good, so with that in mind, it probably looks more positive than not, just considering how bad it’s performed; $250 is the big support range level, $360 is the upside there,” the analyst said.

If Tesla does move back to the $360 per share level, it will represent a nearly 40% upside from Monday’s $260.42 close. Yet, despite the potential recovery, Wald stated that this does not mean TSLA is a “Buy.” “You can see the flat 200-day that exemplifies that directionless action. If we allocate toward stocks that trend, this isn’t one of them,” he noted.

Tesla stock has been weighed down recently partly due to concerns over the Model 3’s alleged “meager” demand and the ongoing issues between CEO Elon Musk and the Securities and Exchange Commission (SEC). On Monday alone, RBC analyst Joseph Spak slashed his price target on Tesla by $35 to $210 each. JMP Securities analyst Joseph Osha also trimmed his price target for Tesla by 3% to $394 per share. Both analysts cited reservations over the Model 3’s demand this first quarter as among the drivers behind their more conservative estimates.

Tesla, for its part, appears to be drawing the curtains back for some good news. On Monday, Tesla proved victorious after a judge dismissed a lawsuit claiming that the company committed fraud during the initial months of the Model 3 production ramp. A recent update from Morgan Stanley analyst Adam Jonas also confirmed that Tesla is not under a Wells notice and is not legally prevented from issuing stock, putting to rest a persistent point that has been brought against the company by its critics. The average price target in Wall St for Tesla stock also remains at $335 per share, implying a ~30% upside from Monday’s close.

This Tuesday, Tesla’s shares appear to be getting a breather, trading (+2.90%) at $267.84 per share as of writing.

Disclosure: I have no ownership in shares of TSLA and have no plans to initiate any positions within 72 hours.

Elon Musk

SpaceX’s newest logo confirms everything about what it’s become

SpaceX officially absorbed xAI under the SpaceXAI brand, completing the largest private merger in history.

SpaceX made its corporate transformation official in May 2026 when Elon Musk posted on X that xAI would cease to exist as a standalone company. “xAI will be dissolved as a separate company, so it will just be SpaceXAI, the AI products from SpaceX,” he wrote.

A new SpaceXAI logo was announced today, visually embedding the xAI letters inside the SpaceX identity, which can be seen as a deliberate design choice that signals the merger is not a partnership but a full absorption and XAi a core function of the same company. The same way Starlink is not a separate brand but a SpaceX product. The announcement closed the loop on a process that began February 2, 2026, when SpaceX acquired xAI in the largest private merger in history, valued at $1.25 trillion. SpaceX at $1 trillion and xAI at $250 billion.

We are now @SpaceXAI. pic.twitter.com/ema66xDWC9

— SpaceXAI (@SpaceXAI) July 6, 2026

The reason SpaceX bought xAI was stated plainly by Musk at the time of the deal: to build orbital data centers. SpaceX had simultaneously filed with the FCC to launch up to one million satellites designed to function as AI compute nodes in low Earth orbit, escaping what Musk described as the energy constraints limiting AI development on Earth.

xAI provided the AI software stack, with Grok, the X platform, and the Colossus supercomputer infrastructure in Memphis with over 220,000 NVIDIA GPUs, while SpaceX provided the rockets, Starlink, and the capital base to fund it. The two companies needed each other. xAI was burning $2.5 billion in losses on $250 million in revenue. SpaceX was generating an estimated $8 billion in profit on $15 billion in revenue and needed an AI narrative to command the valuation it was targeting for its IPO.

What SpaceX has done, regardless of how the orbital AI vision ultimately plays out, is walk into a public market as something no company has been before: a rocket manufacturer, satellite internet provider, AI software company, social media platform, and supercomputer operator under one ticker. Whether that combination is worth $2 trillion depends entirely on which of those businesses you believe in most.

Investor's Corner

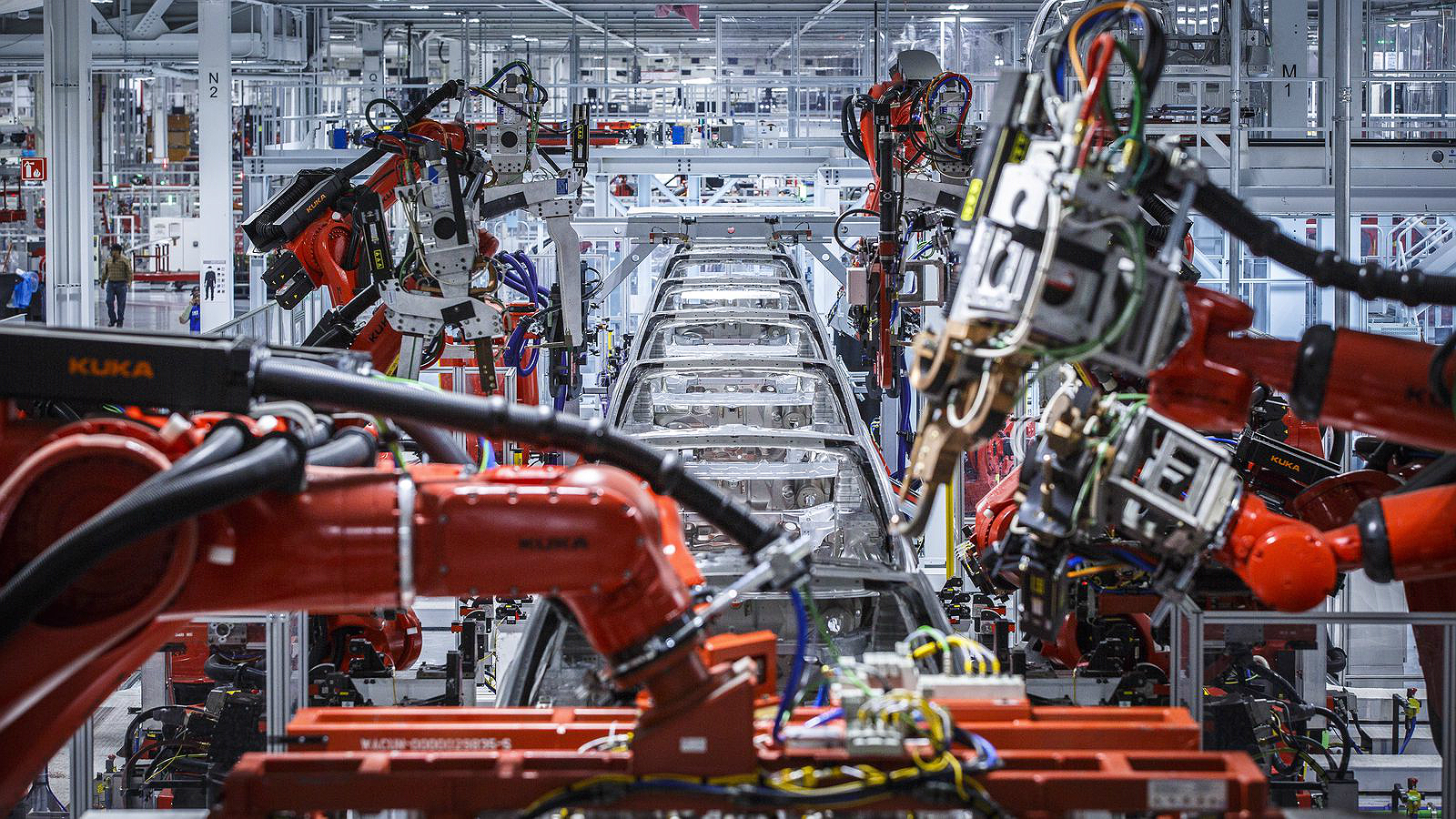

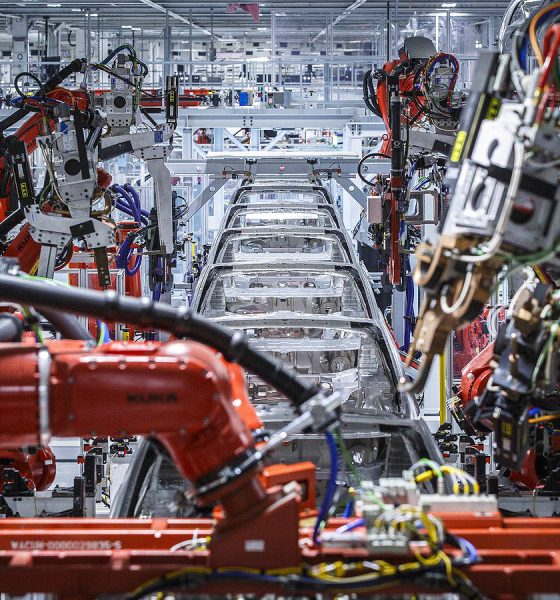

Tesla challenges startups to score a gig inside its most advanced European factory

Tesla is challenging startups to bring their best battery tech directly to Gigafactory Berlin.

Tesla has issued an open challenge to startups across Europe, inviting them to bring their best battery technology directly to the floor of Gigafactory Berlin. The program, called the JUNI x Tesla Battery Cell Giga Challenge, opened applications this month with a deadline of July 24, 2026, and is targeting startups with solutions that can make battery cell manufacturing faster, cheaper, safer, and more scalable at an industrial level.

The timing of the challenge is directly tied to Tesla’s most aggressive European battery investment yet. On May 12, 2026, Giga Berlin plant manager André Thierig announced a $250 million investment to scale the factory’s annual 4680 cell production capacity from 8 GWh to 18 GWh, more than doubling the previous target set just months earlier in December 2025. Thierig confirmed the expansion on X, saying the investment “will enable 18 GWh of annual 4680 cell production and create more than 1,500 new jobs.” Combined with a previously announced battery investment at the Grunheide site now approaches $1.2 billion.

Today, we announced a $ 250m investment for our Giga Berlin Cell factory. This will enable 18GWh of annual 4680 cell production and create more than 1500 new jobs. Good news during challenging times for the German industry. pic.twitter.com/ou4SWMfWh9

— André Thierig (@AndrThie) May 12, 2026

The challenge is looking specifically for startups with proven solutions across five categories: materials, equipment, operations, automation, and artificial intelligence. Applications are screened directly by Tesla’s cell manufacturing team in Grunheide, and the strongest submissions move through technical discussions, a pitch day in front of Tesla stakeholders, and potentially a paid pilot project with the cell team. Tesla is not looking for ideas at concept stage. The program requires applicants to demonstrate working prototypes, test data, or prior pilots before being considered.

The historical context matters here. Elon Musk first announced plans for what he called the world’s largest battery cell production facility alongside the Giga Berlin car factory back in 2020, targeting up to 250 GWh of annual capacity. Those plans were shelved in 2022 when Tesla shifted its battery investment focus to the United States to take advantage of Inflation Reduction Act incentives. The revival of cell production at Giga Berlin, now backed by over $1 billion in committed capital, represents a return to an ambition that was set aside for three years. As Teslarati has reported, the 4680 format is central to Tesla’s long-term cost reduction strategy across vehicles, energy storage, including the Tesla Semi and Cybercab.

By opening the challenge to outside startups, Tesla is acknowledging that reaching 18 GWh at Grunheide will require technology it does not currently have in-house, and it is willing to pay for the right solutions. For a startup in the battery supply chain, a paid pilot with Tesla’s European cell team is as close to a direct commercial path as the industry offers.

Investor's Corner

Tesla crushes Wall Street expectations, beats delivery estimates by over 15 percent

Tesla (NASDAQ: TSLA) beat Wall Street expectations of 406,000 vehicles delivered in Q2 by reporting 480,126 deliveries for the three months ending in June.

Tesla reported it delivered 467,762 Model 3 and Model Y units, while 12,364 Model S, Model X, and Cybertrucks switched hands during the quarter. The Model S and Model X were officially sunset this past quarter and will no longer be part of the company’s Production & Delivery reports moving forward.

🚨 BREAKING: Tesla delivered 480,126 vehicles in Q2, ANNIHILATING Wall Street expectations of 406,000. Production was reported at 451,758.

Deliveries:

Model 3/Y: 467,762

Other Models: 12,364Production:

Model 3/Y: 442,936

Other Models: 8,822 https://t.co/TTHwQAsKt8 pic.twitter.com/7qI4Zj6FE5— TESLARATI (@Teslarati) July 2, 2026

The quarter is a pleasant surprise and a good rebound from Q1, when Tesla slightly missed the Wall Street consensus of 365,645 cars by reporting 358,023 deliveries for the first three motnhs of the year.

Energy storage deployments also provided some strength in Tesla’s delivery report, hitting 13.5 GWh for Q2. This is a particular division of Tesla’s business that has been overwhelmingly robust over the past few years, truly being a strong point of the company’s overall model.

For the year, Tesla analysts still predict deliveries to trend in the 1.69 million unit region, a modest 3 to 5 percent increase from the 1.64 million cars the company delivered last year. Tesla will likely return to more sequential and noticeable year-over-year growth as the Cybercab project starts to ramp up considerably in the next few years.

Tesla has some other potential catalysts to spur vehicle deliveries, too. Not only is it expecting Cybercab to truly start making a change in the next few years, but other vehicles could be entering the company’s lineup.

Tesla sends production Cybercab with no steering wheel, pedals to on-road testing

The slightly longer Model Y L has been a highly speculated release candidate in the U.S. It has already done incredibly well in China, and U.S. buyers have been wanting slightly more interior space than the Model Y. Now that the Model X is gone, it is more needed than ever.

Q2 highlights a pretty stable automotive division within Tesla, and no true concerns arise from these figures, especially considering it managed to beat expectations convincingly.

SpaceX’s newest logo confirms everything about what it’s become

Tesla flexes how it will help the blind with Cybercab