News

SpaceX vs. Blue Origin: The bickering titans of new space

In the past three years, SpaceX has made incredible progress in their program of reusability. In the practice’s first year, the young space company led by serial tech entrepreneur Elon Musk has performed three successful commercial reuses of Falcon 9 boosters in approximately eight months, and has at least two more reused flights scheduled before 2017 is out. Blue Origin, headed and funded by Jeff Bezos of Amazon fame, is perhaps most famous for its supreme confidence, best illustrated by Bezos offhandedly welcoming SpaceX “to the club” after the company first recovered the booster stage of its Falcon 9 rocket in 2015.

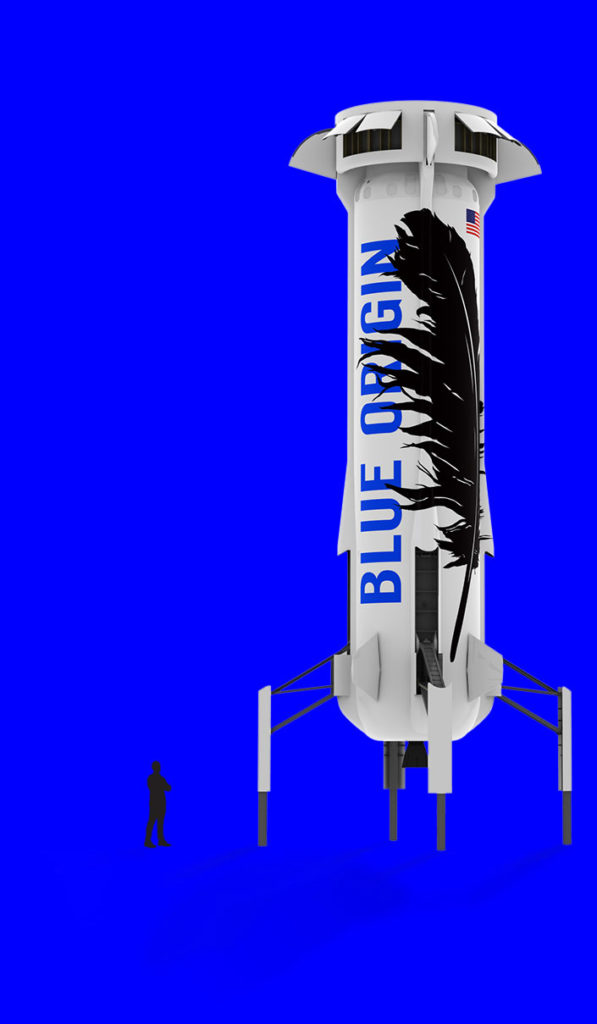

Blue Origin began in the early 2000s as a pet project of Bezos, a long-time fan of spaceflight and proponent of developing economies in space. After more than a decade of persistent development and increasingly complex testbeds, Blue Origin began a multi-year program of test flights with its small New Shepard launch vehicle. Designed to eventually launch tourists to the veritable edge of Earth’s atmosphere in a capsule atop it, New Shepard began its test flights in 2015 and after one partial failure, has completed five successful flights in a row. The space tourism company has subtly and not-so-subtly belittled SpaceX’s accomplishments over the last several years, and has engendered a fair bit of hostility towards it as a result.

Admittedly, CEO Elon Musk nurtured high expectations for the consequences of reuse, and has frequently discussed SpaceX’s ambition to reduce the cost of access to orbit by a factor of 10 to 100. However, after several reuses, it is clear that costs have decreased no more than 10-20%. What gives?

Well, Musk’s many comments on magnitudes of cost reduction were clearly premised upon rapid and complete reuse of both stages of Falcon 9, best evidenced by a concept video the company released in 2011.

The reality was considerably harder and Musk clearly underestimated the difficulty of second stage reuse, something he himself has admitted. COO Gwynne Shotwell was interviewed earlier this summer and discussed SpaceX’s updated approach to complete reusability, and acknowledged that second stage reuse was no longer a real priority, although the company will likely attempt second stage recovery as a validation of future technologies. Instead of pursuing the development of a completely reusable Falcon 9, SpaceX is instead pushing ahead with the development of a much larger rocket, BFR. BFR being designed to enable the sustainable colonization of space by realizing Musk’s original ambition of magnitudes-cheaper orbital launch capabilities.

Competition on the horizon?

Meanwhile, SpaceX’s only near-term competitor interested in serious reuse has made gradual progress over the last several years, accelerating its pace of development more recently. Blue Origin’s second New Shepard vehicle, designed to serve the suborbital space tourism industry, conducted an impressive five successful launches and landings over the course of 2016 before being summarily retired. NS2’s antecedent suffered a failure while attempting its first landing and was destroyed in 2015, but Blue learned quickly from the issues of Shepard 1 and has already shipped New Shepard 3 to its suborbital launch facilities near Van Horn, Texas. While NS3 is aiming for an inaugural flight later this year, NS4 is under construction in Kent, Washington and could support Blue’s first crewed suborbital launches in 2018.

-

-

More significant waves were made with an announcement in 2016 that Blue was pursuing development of a partially reusable orbital-class launch vehicle, the massive New Glenn. On paper, New Glenn is quite a bit larger than even SpaceX’s Falcon 9, and appears to likely be more capable than the company’s “world’s most powerful rocket” while completely recovering its boost stage. In a completed, manufactured, and demonstrably reliable form, New Glenn would be an extraordinarily impressive and capable launch vehicle that could undoubtedly catapult Blue Origin into position of true competition with SpaceX’s reusability efforts.

-

- The New Shepard booster. (Blue Origin)

-

- Blue Origin’s New Shepard capsule could carry passengers as high as 100km in 2018. (Blue Origin)

-

- A render of Blue Origin’s larger New Glenn vehicle. (Blue Origin)

However, while Blue Origin executives brag about “operational reusability” and tastelessly lampoon efforts that “decided to slap some legs on [to] see if [they] could land it”, the unmentioned company implicated in those barbs has begun to routintely and commercially reuse orbital-class boosters five times the size of Blue’s suborbital testbed, New Shepard.

Apples to oranges

The only point at which Blue Origin poses a risk to SpaceX’s business can be found in a comparison of funding sources. SpaceX first successes (and failures) were funded out of Elon Musk’s own pocket, but nearly all of the funding that followed was won through competitive government contracts and rounds of private investment. To put it more simply, SpaceX is a business that must balance costs and returns, while Blue Origin is funded exclusively out of billionaire CEO Jeff Bezos’ pocket.

As a result of being completely privately funded, Bezos’ deep pockets could render Blue more flexible than SpaceX when pricing launches. If Blue chooses to aggressively price New Glenn by accounting for booster reusability, it could pose a threat to SpaceX’s own business strategy. If SpaceX is unable to recoup its investment in reusability before New Glenn is regularly conducting multiple commercial missions per year, likely no earlier than 2021 or 2022, SpaceX’s Falcon 9 pricing could be rendered distinctly noncompetitive.

However, this concern seems almost entirely misplaced. SpaceX has half a decade of experience mass-producing orbital-class (reusable) rockets, (reusable) fairings, and propulsion systems, whereas Blue Origin at best has minimal experience manufacturing a handful of suborbital vehicles over a period of a few years. Blue has a respectable amount of experience with their BE-3 hydrolox propulsion system, and that will likely transfer over to the BE-3U vacuum variant to be used for New Glenn’s third stage. The large methalox rocket engine (BE-4) that will power New Glenn’s first stage also conducted its first-ever hot-fire just weeks ago, a major milestone in propulsion development but also a reminder that BE-4 has an exhaustive regime of engineering verification and flight qualification testing ahead of it.

First hotfire of our BE-4 engine is a success #GradatimFerociter pic.twitter.com/xuotdzfDjF

— Blue Origin (@blueorigin) October 19, 2017

-

Perhaps more importantly, the company’s relative success with New Shepard’s launch, recovery, and reuse has not and cannot move beyond small suborbital hops, and thus cannot provide the experience at the level of orbital rocketry. New Shepard is admittedly capable of reaching an altitude of 100km, but the suborbital vehicle’s flight regime does not require it to travel beyond Mach 4 (~1300 m/s). The first stage of Falcon 9, however, is approximately four times as tall and three times the mass of New Shepard, and boosters attempting recovery during geostationary missions routinely reach almost twice the velocity of New Shepard, entering the thicker atmosphere at more than 2300 m/s (1500-1800 m/s for LEO missions). Falcon 9’s larger mass and velocity translates into intense reentry heating and aerodynamic forces, best demonstrated by the glowing aluminum grid fins that can often be seen in SpaceX’s live coverage of booster recovery. Blue Origin’s New Glenn concept is extremely impressive on paper, but the company will have to pull off an extraordinary leap of technological maturation to move directly from suborbital single-stage hops to multi-stage orbital rocketry. Blue’s accomplishments with New Shepard are nothing to scoff at, but they are a far cry from routine orbital launch services.

SpaceX’s future fast approaches

Translating back to the new establishment, Falcon 9 will likely remain SpaceX’s workhorse rocket for some five or more years, at least until BFR can prove itself to be a reliable and affordable replacement. This change in focus, combined with the downsides of second stage recovery and reuse on a Falcon 9-sized vehicle, means that SpaceX will ‘only’ end up operationally reusing first stages and fairings from the vehicle. The second stage accounts for approximately 20-30% of Falcon 9’s total cost, suggesting that rapid and complete reuse of the fairing and first stage could more than halve its ~$62 million price. Yet this too ignores another mundane fact of corporate life SpaceX must face. Its executives, Musk included, have lately expressed a desire to at least partially recoup the ~$1 billion that was invested to develop reuse. Assuming a partial 10% reduction in cost to reuse customers and profit margins of 50% with rapid and total reuse of the first stage and fairing, 20 to 30 commercial reuses would recoup most or all of SpaceX’s reusability investment.

Musk recently revealed that SpaceX is aiming to complete 30 launches in 2018, and that figure will likely continue to grow in 2019, assuming no major anomalies occur. Manufacturing will rapidly become the main choke point for increased launch cadence, suggesting that drastically higher cadences will largely depend upon first stage reuse with minimal refurbishment, which just so happens to be the goal of the Falcon 9’s upcoming Block 5 iteration. Even if the modifications only manage a handful of launches without refurbishment, rather than the ten flights being pursued, each additional flight without maintenance will effectively multiply SpaceX’s manufacturing capabilities. More bluntly: ten Falcon 9s capable of five reflights could do the same job of 50 brand new rockets with 1/5th of the manufacturing backend.

-

- BulgariaSat-1 was successfully launched 48 hours before Iridium-2, and marked the second or three successful, commercial reuses of an orbital rocket. (SpaceX)

-

- SpaceX’s Hawthorne factory routinely churns out one to two complete Falcon 9s every month. (SpaceX)

-

- Falcon 9 B1040 returns to LZ-1 after the launch of the USAF’s X-37B spaceplane. (SpaceX)

Assuming that upcoming reuses proceed without significant failures and Falcon 9 Block 5 subsumes all manufacturing sometime in 2018 or 2019, it is entirely possible that SpaceX will undergo an extraordinarily rapid phase change from expendability to reusability. Mirroring 2017, we can imagine that SpaceX’s Hawthorne factory will continue to churn out at least 10 to 20 Block 5 Falcon 9s over the course of 2018. Assuming 5 to 10 maintenance-free reuses and a lifespan of as many as 100 flights with intermittent refurb, a single year of manufacturing could provide SpaceX with enough first stages to launch anywhere from 50 to 2000 missions. The reality will inevitably find itself somewhere between those extremely pessimistic and optimistic bookends, and they of course do not account for fairings, second stages, or expendable flights.

If we assume that the proportional cost of Falcon 9’s many components very roughly approximates the amount of manufacturing backend needed to produce them, downsizing Falcon 9 booster production by a factor of two or more could free a huge fraction of SpaceX’s workforce and floor space to be repurposed for fairing and second stage production, as well as the company’s Mars efforts. Such a phase change would also free up a considerable fraction of the capital SpaceX continually invests in its manufacturing infrastructure and workforce, capital that could then be used to ready SpaceX’s facilities for production and testing of its Mars-focused BFR and BFS.

-

“Gradatim ferociter”

It cannot be overstated that the speculation in this article is speculation. Nevertheless, it is speculation built on real information provided over the years by SpaceX’s own executives. Rough estimates like this offer a glimpse into a new launch industry paradigm that could be only a year or two away and could allow SpaceX to begin aggressively pursuing its goal of enabling a sustainable human presence on Mars and throughout the Solar System.

Blue Origin’s future endeavors shine on paper and their goal of enabling millions to work and live space are admirable, but the years between the present and a future of routine orbital missions for the company may not be kind. The engineering hurdles that litter the path to orbital rocketry are unforgiving and can only be exacerbated by blind overconfidence, a lesson that is often only learned the hard way. Blue Origin’s proud motto “Gradatim ferociter” roughly translates to “Step by step, ferociously.” One can only hope that some level of humility and sobriety might temper that ferocity before customers entrust New Glenn with their infrastructural foundations and passengers entrust New Shepard with their lives.

Elon Musk

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it

The Boring Company’s new tunnel vehicle runs on Tesla Model 3 batteries and drive units.

The Boring Company just introduced a new piece of hardware, and it runs on parts pulled straight from a Tesla showroom. Liner Truck 3, unveiled in a post from the tunneling company’s official X account, is an all electric vehicle built around Tesla Model 3 battery packs and drive units, purpose built to move concrete tunnel segments to the boring machine face without a single person underground.

Introducing Liner Truck 3 — our latest fully electric tunnel vehicle.

– Tesla Model 3 battery and drive units

– Transports 22,000+ lb of concrete segments to the boring machine

– 28 miles of range

– 12 mph max operating speed

– Remotely piloted from Global OCC in Texas, with… pic.twitter.com/XB7FgSXnpy— The Boring Company (@boringcompany) August 7, 2026

The job itself is unglamorous but critical. Each precast segment run weighs more than 22,000 pounds, roughly the load of a full cement mixer, and Liner Truck 3 hauls that weight repeatedly between the surface staging area and wherever the Prufrock machine happens to be cutting.

The Boring Company said Liner Truck 3 is piloted remotely out of its Global Operations Control Center in Texas, extending the Zero-People-In-Tunnel approach the company has spent years building toward. An earlier version of a ZPIT liner truck was already tested at the company’s Bastrop, Texas research tunnels, and a factory tour released last month showed an employee flying a fully loaded liner truck with a PlayStation controller. Liner Truck 3 looks like the production version of that same idea, cleaned up and pushed into daily use.

The timing lines up with a company digging in more places than it ever has before. The Boring Company now has multiple Prufrock machines active or arriving in Nashville, where Music City Loop construction has been accelerating since February, and its Vegas Loop network keeps adding tunnel mileage on a near monthly basis. Every one of those projects depends on getting concrete segments to the cutting face fast enough to keep the boring machine from idling, which is exactly the bottleneck Liner Truck 3 is designed to remove.

-

It also reinforces something Tesla owners have watched happen gradually across Musk’s companies: passenger car hardware finding a second life in heavy equipment. Model 3 drive units already move people through the Vegas Loop, and now the same components are hauling concrete underground in Nashville and wherever The Boring Company digs next. Whether that kind of component reuse extends further into TBC’s equipment lineup, or into other Musk owned industrial hardware, is the next thing worth watching.

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

-

News

The Boring Company’s newest Vegas Station has a permit quietly waiting behind it

Sahara Las Vegas opened a new Vegas Loop station, joining an exclusive two resort transit club.

Sahara Las Vegas opened a new Vegas Loop station Thursday, giving The Boring Company’s underground transit system its northernmost stop yet on the Strip. The station sits at Sahara’s Paradise Road entrance, on the southeast corner of Las Vegas Boulevard and Sahara Avenue, and connects riders to the Las Vegas Convention Center, other Strip resorts on the network and, eventually, Harry Reid International Airport.

The addition makes Sahara the second resort, after Fontainebleau opened its own station in January, to get a stop built at street level rather than tucked into the property itself. Sahara now joins Westgate as the only two Strip resorts offering both a Vegas Loop station and a stop on the Las Vegas Monorail, giving guests two separate ways to get around without leaving the property.

The Boring Company just doubled its tunneling power in Nashville

The bigger news buried in Thursday’s announcement is what comes next. Boring Company has already secured its first permit to tunnel north of Sahara Avenue, extending the network beyond where it currently ends, even though permits to push the Loop toward downtown Las Vegas still haven’t been granted. Crews are also working on a two mile dual tunnel line running from Westgate to a planned station at 4744 Paradise Road, just north of Tropicana Avenue, that Las Vegas Convention and Visitors Authority CEO Steve Hill has said the company hopes to open in time for November’s Las Vegas Grand Prix.

Ridership has grown alongside the buildout. The Loop moved roughly 82,000 passengers during CONEXPO in early March, a total the company highlighted on its own X account at the time, and the system has now carried more than 4 million passengers through 11 open stations since it began running in 2021. The airport connector tunnels, meant to give the Loop a direct link to Harry Reid, have slipped past their original first quarter target and remain under construction, with Boring Company director Mike Baier saying that a full opening is still a few months out.

For Sahara, the calculation is straightforward. Convention traffic drives a large share of Loop ridership, and a station at the property’s front door gives conventiongoers one more reason to book rooms on the Strip’s north end instead of closer to the convention center itself.

-

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it

Elon Musk and SpaceX shrugs off the trading day Wall Street feared most