Investor's Corner

Tesla bull ARK loads up on TSLA shares amid stock slide

Tesla (NASDAQ: TSLA) bull ARK Invest, headed by CEO and CIO Cathie Wood, loaded up on shares of the electric automaker’s stock as it has slid to lower prices over the past few weeks.

According to ARK’s Daily Trade Information, the fund bought 19,272 shares of Tesla, adding onto its massive holdings of the electric automaker’s shares. After the purchase on Friday, ARK now holds 3,566,628 shares of Tesla stock, which makes up 9.99% of its total portfolio. Square Inc. is ARK’s second-largest holding, with 6.28% of the portfolio being made up of the financial company.

ARK’s Tesla holdings are worth $2,132,665,212.60, according to the documents released on Friday.

The purchase of 19,272 additional shares supplements the addition of 130,000 shares in mid-February that were added to several different ARK ETFs. The ARK Innovation ETF bought 89,447 TSLA shares, while the ARK Next Generation Internet ETF added 29,508 Tesla stocks, and the ARK Autonomous Technology and Robotics ETF added 13,173 shares in February.

ARK is one of Tesla’s biggest bulls on Wall Street, holding tremendously high expectations for the electric automaker’s outlook over the next nine years. By 2030, ARK believes that Tesla’s Robotaxi fleet could generate more than $1 trillion in operating revenue, evidently remaining bullish on the automaker despite a recent slide in stock price.

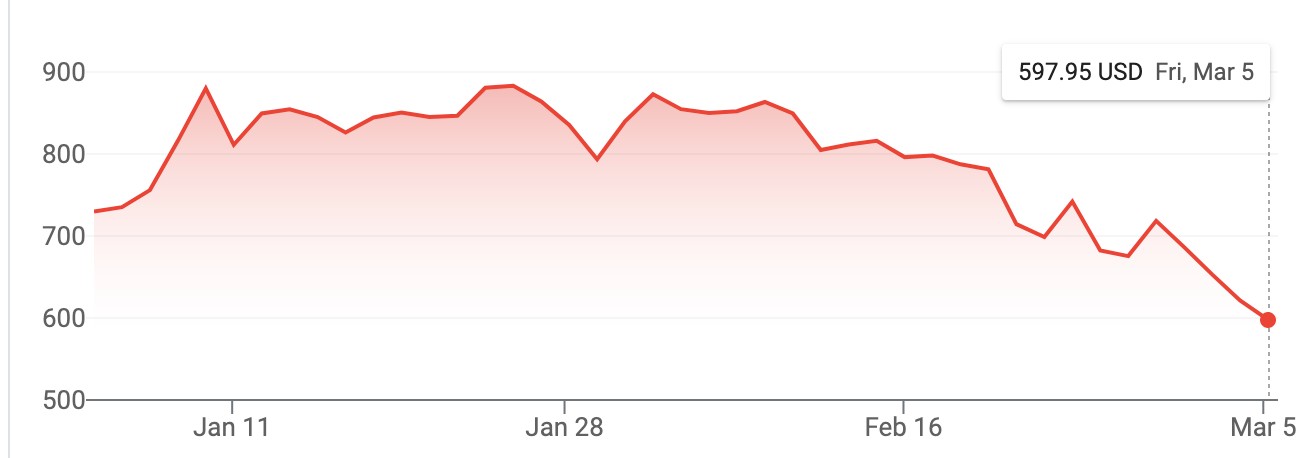

Tesla is down 30.75% over the past month and down 18% on the year. The stock currently sits at $597.95, closing on Friday down 3.78% or $23.49.

Tesla’s 2021 Stock Graph (Google)

After surging to prices as high as $880.02 in January, the stock remained relatively consistent in price until February 8th, when the price began to fall. Some analysts attributed the fall to Tesla’s lack of delivery forecast after the Q4 2020 Earnings Call. While Tesla executives didn’t give a specific figure, they did indicate that they expect 50% growth in deliveries annually, with some years providing more expansion.

A statement during the company’s most recent Earnings Call said that Tesla expects “to achieve 50% average annual growth in vehicle deliveries. In some years, we may grow faster, which we expect to be the case in 2021.” Additionally, it is difficult to give a specific figure as Tesla is expecting both Giga Berlin and Giga Texas to be completed at some point this year. With both facilities moving along quickly in the construction process, there is no specific time frame when they will be completed, which could be why Tesla did not provide specific delivery goals for 2021.

-

-

Many believe this is a temporary setback for Tesla. With expanding demand for the company’s vehicles and its place as the EV leader, Tesla is primed to dominate an expanding sector in the coming years. Dan Ives of Wedbush believes Tesla’s path to victory ultimately lies in China, where competitors are firing on all cylinders to catch up with Elon Musk’s company.

Tesla stock pullback temporary, China demand paves way to $1T market cap, Wedbush says

Disclosure: Joey Klender is a TSLA Shareholder.

SpaceX (NASDAQ: SPCX) got an absolutely crazy price target rating from Raymond James after the company experienced a tough first few weeks following its Initial Public Offering (IPO).

Despite the tumultuous start, SpaceX has plenty of believers, and the company’s massively successful Starship launch last Friday, its 13th test flight of the massive rocket, went so smoothly that Raymond James analysts pushed its price target on the company to roughly 7 times its current trading level.

SpaceX Starship just nailed something it’s never done before

The firm officially put a “Strong Buy” rating and an $800 price target on the stock. It currently trades at around $113. Its all-time high is $225.64, reaching this trading level shortly after shares first went public.

Raymond James’ price target is tied to the firm’s confidence after Starship’s 13th test flight. Analysts at the firm said it was an incremental step that reduces engineering risks, citing the widely successful heat shield test that CEO Elon Musk recently detailed, the smooth deployment of Starlink V3 satellites, and a successful in-space engine relight.

SpaceX also managed to see Starship splash down safely in the Indian Ocean, while the Super Heavy Booster fell down to the Gulf of America with no incidents.

It is interesting to see these launches have such a tremendous impact on the stock and what investors think of it. After SpaceX initially delayed the Starship launch last week, shares fell tremendously. Most probably did not realize that the stand-down is a standard practice, especially if everything is not perfect.

-

The mission was initially aborted due to an issue with Raptor engines. This was resolved, and Starship launched last Friday after another delay on Thursday, which was caused by weather.

Now that analysts have seen what SpaceX launches are capable of and how impressive the feat is, firms are adjusting their price targets accordingly, making it known that they have high expectations for the space exploration company.

Elon Musk

SpaceX Starship just nailed something it’s never done before

SpaceX’s Starship flew successfully Friday, landing both stages and deploying its first Starlink V3 satellites.

Starship’s thirteenth test flight delivered exactly what SpaceX needed with a clean liftoff, two successful stage recoveries, and the first real payload the vehicle has ever carried to space. Booster 20 and Ship 40 lifted off at 5:51 p.m. CT from Starbase, and by the time the mission wrapped roughly an hour later, both halves of the rocket had done exactly what they were supposed to do.

Booster 20 separated from Ship 40 a few minutes into the flight and stuck a controlled splashdown in the Gulf of Mexico about six minutes after liftoff. That is a meaningful turnaround from Flight 12 in May, when the booster lost several engines during its boostback burn before a hard water landing attempt.

Starship as seen from Starlink satellites pic.twitter.com/e2hvfmnewh

— Elon Musk (@elonmusk) July 25, 2026

Starship 40’s performance was arguably the bigger win. The vehicle deployed the first 20 operational Starlink V3 satellites Starship has ever carried, then flew a suborbital arc to a landing in the Indian Ocean that SpaceX commentator Dan Huot called the company’s softest splashdown yet. “This is a dream scenario for this team that’s trying to get this heat shield data,” Huot said on the live broadcast, according to Space.com’s live coverage. “I’m a little over the moon right now. Wow. Lucky number 13.”

Unlike the mass simulators SpaceX flew on Flight 12, these were production Starlink V3 satellites, meant to extend solar arrays and antennas and attempt to link with the broader constellation before reentering minutes later. Getting real hardware through a full deploy sequence on only the second flight of the V3 generation keeps Starship on schedule for the payload work NASA is counting on for future Artemis lunar landings.

What an awesome launch, really seems like everything went super well and it was all incredibly smooth.

SpaceX is awesome. Very interested to see how the market will respond on Monday pic.twitter.com/KSHmyBfV55

— TESLARATI (@Teslarati) July 25, 2026

-

— TESLARATI (@Teslarati) July 25, 2026

The flight also arrives at a moment when SpaceX needed a win. SPCX has traded below its $135 IPO price since mid-July, as Teslarati reported when the mission slipped to Friday, and short interest has climbed to roughly a third of the tradable float. A clean flight will not fix a balance sheet, but it does answer the one question SpaceX absolutely needed answered this week: whether the fixes made after the July 16 abort would hold up under real flight conditions. They did, on both stages, on the first try after the redesign.

SpaceX has not set a target date for Flight 14, though the company has said it wants to push toward an orbital attempt on the next mission. After Friday, that goal looks a lot more within reach.

Tesla short sellers won big following the company’s massive fall on Wall Street after it reported subpar Earnings on Wednesday.

Tesla short sellers collected about $4.12 billion in single-day profits on Thursday, according to Bloomberg. Shares fell as much as 15 percent during Thursday’s session. It closed as one of the worst days for Tesla on Wall Street in the past three years.

Investors sold off the stock after Tesla said it would aggressively direct its spending toward AI and its Optimus robot project. The company had record revenues, which were driven by one of the strongest quarters in terms of vehicle deliveries in company history.

However, it missed EPS estimates by reporting just $0.33, a far cry from the $0.53 analysts expected.

S3 Partners reported that about 3 percent of Tesla’s outstanding stock is sold short. Managing Director at S3, Ihor Dusaniwsky, provided the short seller’s potential profit, as well as another figure: shorts have likely had paper gains of $8.92 billion this year, as Tesla shares are down 30 percent in 2026.

-

Tesla (TSLA) Q2 2026 earnings results: miss on EPS, beat on revenue

Tesla has burned short sellers many times in the past, but the company’s latest Earnings Call was a chance for those skeptics to taste some payback. Although the company gave some very transparent information regarding future projects, the rollout of Robotaxi, Optimus, and Semi, many investors took their profits on Thursday.

Notable short sellers like Michael Burry have been transparent about their skepticism around Tesla shares. Burry just revealed three weeks ago that he had opened up a new short on the stock, stating he shorted Tesla shares at $416.22. “Happy it jumped back to this level,” he said in a blog post.

At the time of publication, Tesla shares were down about 3 percent and the stock was trading at $309.92.

Elon Musk updates the SpaceX timeline for Mars

SpaceX gets an absolutely crazy price target after rough IPO