Tesla’s (NASDAQ: TSLA) $1.5 billion purchase of Bitcoin, a move announced yesterday in a 10-K document filed with the SEC, was the most popular news surrounding the electric automaker on Monday. While some TSLA investors saw it as their time to get out of being shareholders, others look at it as an advantage in several ways. One person looking at the move from a bullish perspective is ARK Invest’s Tasha Keeney, who believes Tesla’s Bitcoin purchase has heavy advantages as the company moves toward a broader consumer base, especially in international markets.

Tesla’s BTC Purchase

In a 10-K filing with the Securities and Exchange Commission (SEC), Tesla announced it had purchased $1.5 billion in Bitcoin, a cryptocurrency that has massive value, trading at over $46,600 at the time of writing. Tesla added that it “may acquire and hold digital assets from time to time or long-term,” and that it anticipates the purchase of its cars and other products by using the cryptocurrency in the near future.

The move follows CEO Elon Musk’s vocal support of both Bitcoin and Dogecoin, two cryptocurrencies that have maintained huge upside potential over the past several months. Among the ever-growing list of digital currencies, Bitcoin and Dogecoin are among the most popular in 2021, mainly because of ongoing celebrity support.

In the past several years, Bitcoin has become widely popular, especially after a meteoric rise in value in 2017 and 2018 that made it a household name. Early investors used Bitcoin to purchase goods from the internet in an untraceable manner. Now, more retail companies are working on accepting the crypto as a form of payment for everything from a pizza to a Rolex watch.

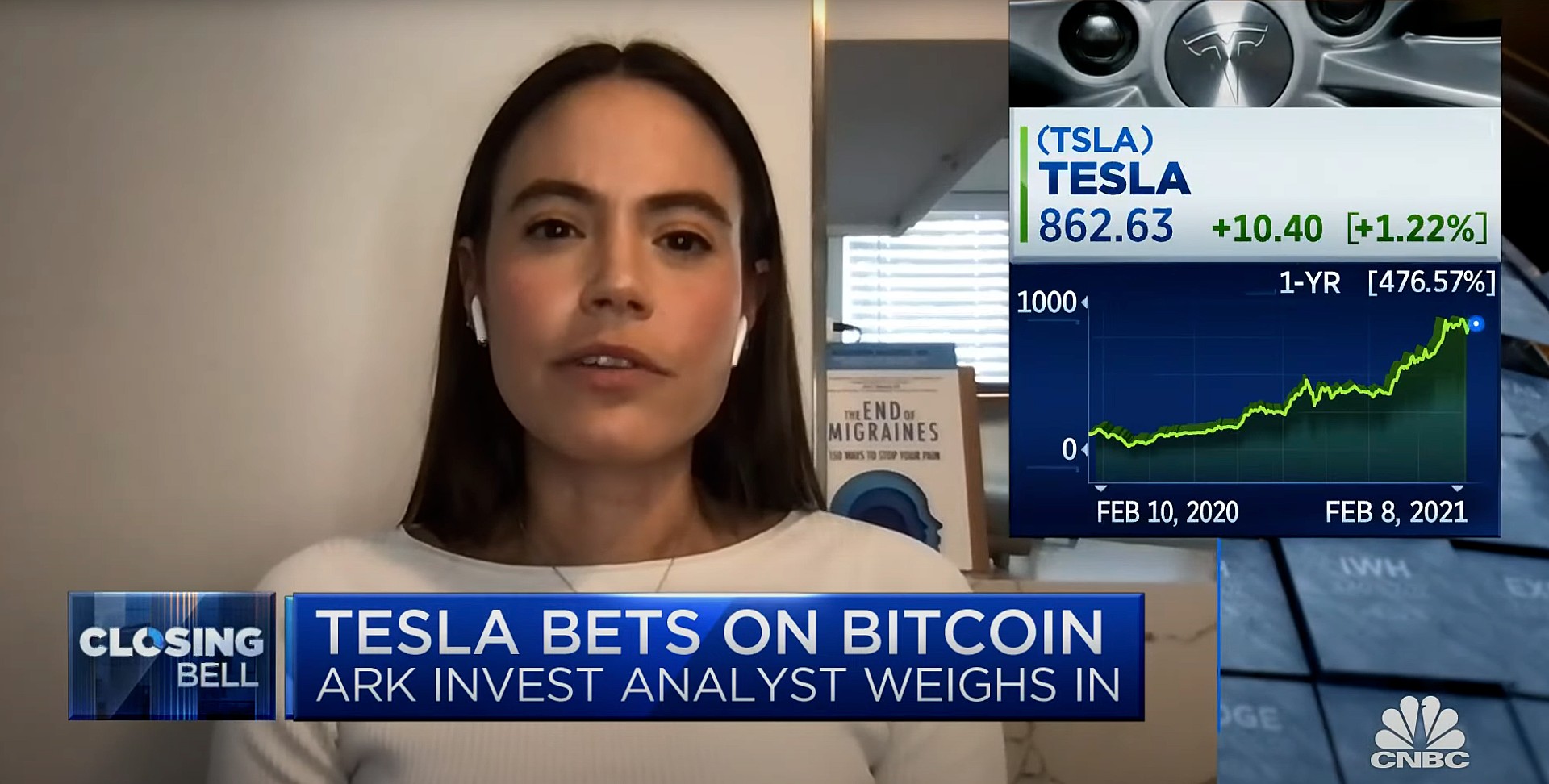

“It is a very serious move from [Tesla] – Keeney

Tasha Keeney, an analyst for Ark Invest, stated that Tesla’s move to purchase Bitcoin is one that aligns with the company’s recent Big Ideas Report. One of the most significant advantages to purchasing Bitcoin for Tesla is the versatility of the cryptocurrency, especially when doing business internationally. “Using Bitcoin as corporate cash, especially if you’re doing business in many different countries with many different foreign currencies…instead of dealing with the complication and the treasury risk, you can instead do this with Bitcoin,” Keeney said. “We think it makes sense from a corporate cash standpoint, and actually, we’ve done some analysts to say that if 1% of all the cash from the companies in the S&P 500 were to be converted into Bitcoin for corporate treasury purposes, this could actually increase the price by a meaningful amount, by about $40,000.”

Additionally, when operational in other countries, Tesla’s planned ride-hailing Robotaxi service could avoid hurdles and complications in payment by using a universal currency instead of multiple different foreign currencies. Keeney says the payment function could be void of conversion issues if customers used a single form of payment instead of dealing with various currencies in each region.

Tesla bull ARK Invest estimates autonomous ride-hailing to generate over $1T in revenue by 2030

-

-

A Publicity Move? ARK doesn’t think so

Bitcoin is no longer a risky or unusual form of payment. Many large companies accept the crypto as a form of currency, and Tesla just plans to be the latest one to accept it. “[Their move] is validated by other firms doing the same thing,” Keeney added during an interview with CNBC.

With Tesla focused on a widespread and quickly accelerating rollout of its products in foreign countries, Bitcoin’s international usage seems to be an advantage that the automaker can use. From a treasury perspective, it doesn’t make sense to deal with so many different foreign currencies, and Bitcoin’s universal acceptance across the world gives Tesla versatility as it expands. With plans to enter the highly elusive Indian market shortly, and expansions in Singapore, Israel, among several other countries, Tesla is technically making a move that supports its goal: accelerate the world’s transition to sustainable energy.

Tesla’s somewhat early adoption of Bitcoin as a payment method and as an internal investment also holds other benefits, Keeney says. With Tesla joining the Bitcoin movement, it, along with other companies, could experience a tailwind in growth from its influence. Other companies are bound to either invest or accept Bitcoin as a currency later on. The entities that got in before it was widely-accepted could benefit from a surge in valuation after it continues to be looked at as a payment method.

“Being one of the first companies to invest in Bitcoin, to transact in Bitcoin, actually gives them sort of an advantage to really lay that infrastructure as it becomes increasingly important. And again, as other firms might do it, because we feel there will be the need for the infrastructure to be set up. So, [Tesla] will be one of the first players to figure this out,” Keeney stated.

Check out Keeney’s interview with CNBC below.

Disclosure: Joey Klender is a TSLA shareholder. He does not hold any BTC and has no intentions to open any positions within 72 hours.

-

-

-

Venture capitalist Chamath Palihapitiya has cautioned investors shorting SpaceX shares, drawing a direct parallel to the intense short-selling pressure Tesla faced in its early public years.

Responding to reports of elevated short interest in the newly public rocket, satellite, and AI company, Palihapitiya noted that similar dynamics played out with Tesla, where aggressive short sellers ultimately “went broke.”

SpaceX (NASDAQ: SPCX) went public on June 12, 2026, in the largest IPO on record, pricing at $135 per share. Shares quickly surged to an all-time high of $225.64 just days later, briefly implying a valuation exceeding $2 trillion. The stock has since retreated sharply amid valuation concerns, lockup expiration fears, and broader market dynamics.

By early August, it traded near $108–$125, representing a roughly 50 percent decline from the peak and bringing the market capitalization closer to the $1.5–1.7 trillion range. On August 4, shares closed up more than 9 percent at $125.33 ahead of earnings before facing pressure in after-hours and premarket trading.

Short interest has climbed dramatically. According to S3 Partners data widely cited in market reports, short positions reached approximately 219.3 million shares by late July, about 34 percent of the limited public float of roughly 640 million shares, and represented a notional value of around $24.6 billion.

Utilization of shares available to borrow hit 95 percent, with borrow fees rising. This level of shorting exceeded the dollar value of short bets against Tesla at the time and built rapidly ahead of two catalysts: the company’s first post-IPO earnings and an August 6 lockup expiration that could free up to 911.5 million additional shares.

-

CEO Elon Musk has issued warnings of his own. In mid-July, as short interest approached one-third of the float, he posted that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” reiterating his view that the company could ultimately be worth more than Earth if it achieves its goals.

On August 4, just before earnings, Musk responded to the latest short-interest data by saying, “I try to warn them, but they just double down.”

SpaceX delivered its first quarterly results as a public company after the close on August 4. Second-quarter revenue rose 92 percent year-over-year to $7.8 billion, beating consensus estimates near $6.8–6.9 billion.

The net loss narrowed to $541 million, or 9 cents per share, better than the roughly 23–24 cent loss expected. Starlink/connectivity contributed about $4.3 billion (up 66 percent), while the AI business generated $2.6 billion (up roughly 250 percent). Capital expenditures were heavy at $18.4 billion, largely tied to AI infrastructure. Management projected a $100 billion annualized revenue run rate by year-end 2026 and outlined a path toward $1 trillion in annual revenue by 2030.

The combination of Chamath’s historical reminder, Musk’s repeated alerts, and the company’s ambitious growth targets underscores the high-stakes debate surrounding SPCX. Short sellers are positioned for near-term supply pressure from the lockup, while long-term bulls point to Starlink scale, Starship progress, and AI compute expansion as reasons the bears may ultimately face the same fate as many early Tesla skeptics.

Investor's Corner

SpaceX and Nvidia team up on Musk’s orbital AI bet

SpaceX revealed a new Nvidia satellite partnership, then Musk pledged an exclusive Nvidia hardware commitment.

SpaceX and Nvidia are now working together on the hardware that will power Musk’s orbital data center ambitions. SpaceX announced on X on Tuesday that it is partnering with Nvidia to design the compute payload for Starmind AI1, the first satellite in a planned constellation built to run AI workloads directly in orbit. Each Starmind satellite will carry Nvidia’s Rubin GPUs and Vera CPUs, according to the post, which included renderings of the payload design.

The announcement landed hours before SpaceX’s first earnings call as a public company, where Musk went further, saying the company has committed to building its AI infrastructure exclusively on Nvidia hardware. “We think the Vera Rubin architecture is the best architecture. We think it’s the best AI computer, and we greatly value our close cooperation and partnership on many levels with Nvidia,” Musk told investors on the call,. “So we’re exclusive to Nvidia.”

Musk said SpaceX plans to deploy Nvidia’s Vera Rubin NVL72 rackscale system, codenamed Kyber, both on the ground and in space. He set a target of 2 gigawatts of compute capacity online by the end of this year, scaling to roughly 10 gigawatts by the end of 2027.

SpaceX’s newest Starmind will make earth data centers obsolete

Starmind has been in development since Musk confirmed the name in June, following an xAI trademark filing that tipped off the project before SpaceX made it official. The idea is massive in scope and instead of moving data down to ground based servers, satellites equipped with onboard processors and large solar arrays would compute AI workloads in orbit and beam results back to Earth. SpaceX has already filed with the FCC for a constellation of up to one million satellites to support the effort, citing constant solar power and the absence of zoning restrictions as advantages over terrestrial data centers.

The Nvidia exclusivity marks a shift in tone from just two weeks ago, when Musk was busy knocking down a report that SpaceX had ordered $52 billion worth of Nvidia GPUs through Foxconn, calling it fake news at the time. The dollar figure in that rumor may have been wrong, but the underlying direction seems correct. SpaceX’s AI division already leases Colossus compute capacity to Anthropic and Google, and Tuesday’s earnings report showed AI revenue climbing sharply as those deals ramp up.

Nvidia shares rose roughly 3% in Tuesday trading on the news, while SpaceX stock climbed nearly 9% during the day before giving back gains after hours as investors digested the earnings report’s capital spending figures.

-

SpaceX (NASDAQ: SPCX) reported a beat in revenues and EBITDA in its first earnings call report while also minimizing losses as its business continues to gain momentum.

After its IPO in July, SpaceX saw some tough losses on Wall Street due to a major selloff after a delay in its 13th Starship test flight. The ship launched later that week and completed what was arguably the most successful IFT operation in the Starship program’s history.

Nevertheless, the company is continuing on and reported some encouraging financials while also promoting what appears to be a robust outlook moving forward in its Space, AI, and Connectivity divisions.

SpaceX to report first-ever earnings today: here’s what to expect

Earnings Results

- Revenues: $7.8 billion reported vs. $6.7 billion expected

- Adjusted EBITDA: $3.5 billion vs. $2 billion expected

- Net loss of $541 million, an improvement of $467 million from net loss of $1.0 billion

Additionally, CFO Bret Johnsen had these comments:

“2026 has been a momentous year so far, and the second quarter demonstrated the true power of SpaceX. Revenue growth accelerated across all our business segments and we delivered strong operating leverage, with significant margin expansion led by our new AI compute agreements. Our unparalleled leadership in launch, Starlink subscriber growth, new enterprise and government partnerships, and best-in-class AI infrastructure underscore our ability to drive meaningful scale and deliver attractive returns. As a newly public company, we are delighted to welcome our broad base of shareholders and bondholders. We ended the second quarter with $100 billion of cash, cash equivalents, and marketable securities, and $47.5 billion in backlog. This financial strength gives us substantial capacity to invest in Starship, Starlink Broadband and Mobile satellites, and our AI platform, while maintaining a disciplined long-term capital allocation framework.”

Space Business Highlights

SpaceX shared some of its biggest Space Business Highlights for Q2:

- Space revenues grew 55% sequentially and 29% year-over-year to $962 million, driven by a higher number of large customer launches and a favorable customer shift compared to the prior year

- Total costs and expenses for the Space segment were up by $389 million year-over-year, as we continued to accelerate R&D investments in our Starship program, which we believe will reduce the cost to orbit by 99% or more relative to the historical average, and unlock significant revenue potential across all business segments

- Leading launch provider for the world with 78 launches and 1,041 metric tons of mass to orbit deployed over the six months ended June 30, 2026, primarily allocated to Connectivity for the deployment of our Starlink constellation

- Starship V3 development continued to advance towards full and rapid reusability:

- Completed Starship V3’s first suborbital mission in May, Flight 12, which achieved a successful lift off from our new Starbase pad, a precision landing of Starship’s upper stage, and deployment of modified V2 Starlink satellites

- Subsequent to the second quarter, completed Starship Flight 13 in July, which achieved all flight objectives including deploying 20 production V3 satellites, demonstrating in-space relight of a Raptor engine, and executing the softest ever splashdown of Starship, providing critical views of an intact heatshield

SpaceX will report its earnings today at 4:30 P.M. EDT.

-

SpaceX has solved Starship’s biggest challenge, Elon Musk says

SpaceX is coming for wireless giants with Starlink Mobile