Investor's Corner

What to look for in Tesla Motors Q1 Financials

Tesla (NASDAQ: TSLA) is set to announce its first quarter earnings report after market close on Wednesday, May 4, 2016.

TSLA reported 4th quarter 2015 earnings of $ -0.87 per share on February 10, 2016. This missed the consensus of $ 0.10 by $ -0.97 of the 16 analysts covering this company. Interestingly that turned out to be the end of a dramatic 42% slide which began on January 1st. Since then TSLA has moved from its lowest point of $141 on that day to roughly $250 per share, a 78% increase in just 3 months. That kind of tells you that TSLA is a stock not for the faint of heart.

Source: WallSt I/O

The consensus of the 14 analysts covering TSLA for 1st quarter 2016 is a per share loss of $ -.57, with range estimates of: 0.080 | -0.569 | -1.000 (High | Mean | Low).

")

$TSLA earnings summary via E-Trade

Based on 20 analysts offering 12-month targets from TSLA, the average price target is $243.95, effectively a zero-move from the current stock price. If you are an “investor” in TSLA stock, the pros tell you that TSLA will not go anywhere in the next 12 months.

$TSLA analysis via TipRanks

So those are the numbers from the pros, but if you still decide that you want to trade TSLA stock, what should you be looking for in the quarterly results and the conference call webcast?

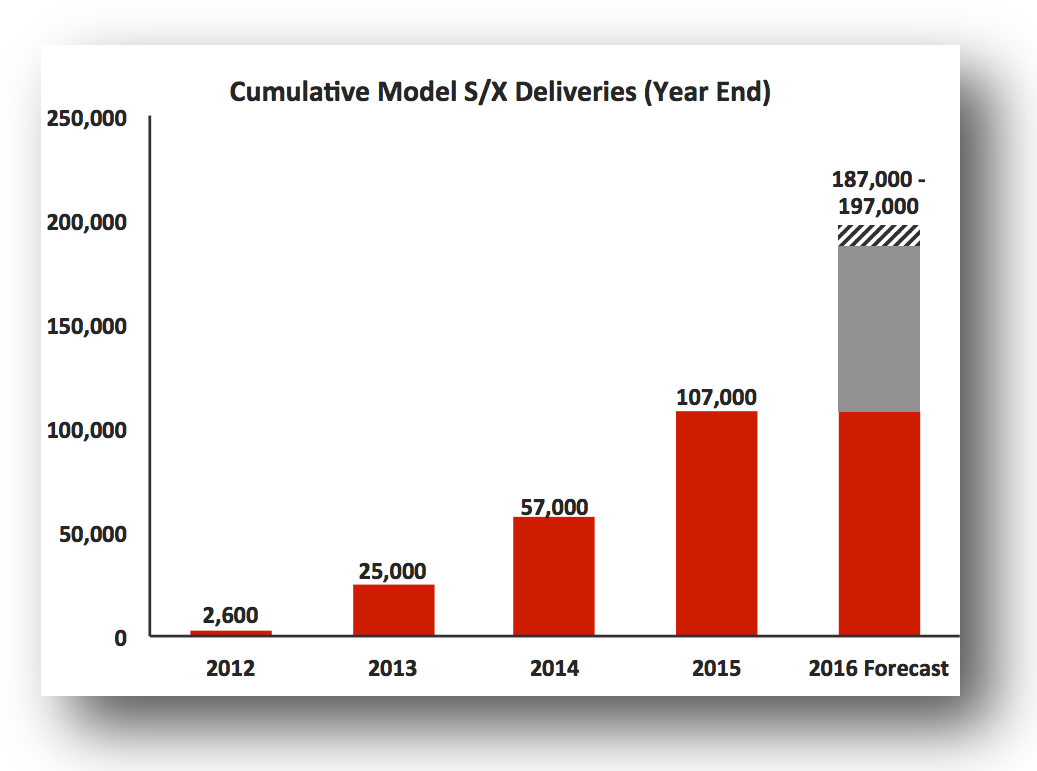

Q1 Vehicle Deliveries

Let’s take a look at a few items from the “Tesla 4th Quarter & Full year 2015 Shareholder Letter”.

In the “Q1 and Full Year 2016 Outlook” section, Tesla states that “we plan to deliver 80,000 to 90,000 new Model S and Model X vehicles in 2016. […] In Q1, we plan to grow deliveries 60% year on year to approximately 16,000 vehicles”.

Source: Tesla Motors

We already know that Q1 deliveries did not meet the promised 16,000 units, as that number was actually 14,820, due to “severe Model X supplier parts shortages in January and February” as provided in a Press Release on April 4, 2016. In the same release, “Tesla reaffirms its full-year delivery guidance [of 80,000 to 90,000 vehicles].”

The missing income due to the delayed Model X vehicles delivery will be partially offset by the initial Model 3 “reservations”. It is quite interesting that reservations opened on March 31, 2016, the last day in the quarter, and at least 125,000 of them may be counted as an additional $125M income in Q1. In the end, guidance on vehicle deliveries for Q2 2016 will be one of the deciding factors on where TSLA stock moves post the Q1 report.

Cash Flow and Margins

In the same Q4 Shareholder Letter, Tesla states that “we expect to generate positive net cash flow and achieve non-GAAP profitability for the full-year 2016”, and “we plan to fund about $1.5 billion in capital expenditures without accessing any outside capital.” These are both very aggressive goals, especially in light of the 400,000+ Model 3 reservations, as of the latest disclosed counts. Elon Musk has already tweeted that he is “definitely going to need to rethink production plans”, which likely means that another factory will be needed to produce the Model 3 in a reasonable timeline that will allow delivery to the majority of the current reservation holders. This more aggressive delivery of Model 3 vehicles as originally envisioned will likely require outside capital for building such factory.

Definitely going to need to rethink production planning…

— Elon Musk (@elonmusk) April 1, 2016

Since missing the mark on Model X will impact cash flow for Q1, I would expect questions in the conference call asking if the issues have been resolved, and if the missing Model X numbers can be made up in Q2. While cash flow reversed action to the positive for the first time during Q4 2015, with a strong $179M cash flow from core operations, Tesla needs to prove that this behavior will continue in 2016.

Again in the Q1 Shareholder Letter, Tesla states that “Throughout the rest of 2016, Automotive gross margins should continue to increase. […] Model S gross margins should begin to approach 30% and Model X gross margins should be about 25%.” In Q4 gross margins were 20.9% for the Tesla Model S and even a slight increase in margins will be viewed positively by the market. This is a number that will be greatly watched as Tesla needs to prove that it can eventually deliver 500K+ vehicles / year at a profit. Much of the current valuation of Tesla stock is built on this assumption. Accordingly, a drop in margins for Q1 would be viewed very negatively by the market, at least for the short term.

Summarizing, besides vehicle delivery, cash flow and margins will be the other two drivers of the TSLA stock short-term market action after the Q1 report numbers are released.

Live Q&A Webcast

Tesla management will hold a live question & answer webcast on May 4 at 2:30pm Pacific Time to discuss the Company’s financial and business results and outlook. Live and replay webcast will be available at http://ir.teslamotors.com/eventdetail.cfm?EventID=171952 .

Tip of the Week

Starting with today’s posting I’ll be including a “tip of the week.” This may involve covering a trading concept, or recommending a website with tools or information useful to investors and traders of TSLA.

For this week, I am recommending signing up for the free Basic Membership of TipRanks. With it you can receive free alerts for 1 stock and 1 expert, which is enough for the ones just interested in TSLA stock. Happy trading.

Disclosure: I currently have no positions in any stocks mentioned, but I may plan to initiate positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Teslarati). I have no business relationship with any company whose stock is mentioned in this article.

Investor's Corner

Tesla could save $2.5B by replacing 10% of staff with Optimus: Morgan Stanley

Jonas assigned each robot a net present value (NPV) of $200,000.

Tesla’s (NASDAQ:TSLA) near-term outlook may be clouded by political controversies and regulatory headwinds, but Morgan Stanley analyst Adam Jonas sees a glimmer of opportunity for the electric vehicle maker.

In a new note, the Morgan Stanley analyst estimated that Tesla could save $2.5 billion by replacing just 10% of its workforce with its Optimus robots, assigning each robot a net present value (NPV) of $200,000.

Morgan Stanley highlights Optimus’ savings potential

Jonas highlighted the potential savings on Tesla’s workforce of 125,665 employees in his note, suggesting that the utilization of Optimus robots could significantly reduce labor costs. The analyst’s note arrived shortly after Tesla reported Q2 2025 deliveries of 384,122 vehicles, which came close to Morgan Stanley’s estimate and slightly under the consensus of 385,086.

“Tesla has 125,665 employees worldwide (year-end 2024). On our calculations, a 10% substitution to humanoid at approximately ($200k NPV/humanoid) could be worth approximately $2.5bn,” Jonas wrote, as noted by Street Insider.

Jonas also issued some caution on Tesla Energy, whose battery storage deployments were flat year over year at 9.6 GWh. Morgan Stanley had expected Tesla Energy to post battery storage deployments of 14 GWh in the second quarter.

Musk’s political ambitions

The backdrop to Jonas’ note included Elon Musk’s involvement in U.S. politics. The Tesla CEO recently floated the idea of launching a new political party, following a poll on X that showed support for the idea. Though a widely circulated FEC filing was labeled false by Musk, the CEO does seem intent on establishing a third political party in the United States.

Jonas cautioned that Musk’s political efforts could divert attention and resources from Tesla’s core operations, adding near-term pressure on TSLA stock. “We believe investors should be prepared for further devotion of resources (financial, time/attention) in the direction of Mr. Musk’s political priorities which may add further near-term pressure to TSLA shares,” Jonas stated.

Investor's Corner

Two Tesla bulls share differing insights on Elon Musk, the Board, and politics

Two noted Tesla bulls have shared differing views on the recent activities of CEO Elon Musk and the company’s leadership.

Two noted Tesla (NASDAQ:TSLA) bulls have shared differing views on the recent activities of CEO Elon Musk and the company’s leadership.

While Wedbush analyst Dan Ives called on Tesla’s board to take concrete steps to ensure Musk remains focused on the EV maker, longtime Tesla supporter Cathie Wood of Ark Invest reaffirmed her confidence in the CEO and the company’s leadership.

Ives warns of distraction risk amid crucial growth phase

In a recent note, Ives stated that Tesla is at a critical point in its history, as the company is transitioning from an EV maker towards an entity that is more focused on autonomous driving and robotics. He then noted that the Board of Directors should “act now” and establish formal boundaries around Musk’s political activities, which could be a headwind on TSLA stock.

Ives laid out a three-point plan that he believes could ensure that the electric vehicle maker is led with proper leadership until the end of the decade. First off, the analyst noted that a new “incentive-driven pay package for Musk as CEO that increases his ownership of Tesla up to ~25% voting power” is necessary. He also stated that the Board should establish clear guidelines for how much time Musk must devote to Tesla operations in order to receive his compensation, and a dedicated oversight committee must be formed to monitor the CEO’s political activities.

Ives, however, highlighted that Tesla should move forward with Musk at its helm. “We urge the Board to act now and move the Tesla story forward with Musk as CEO,” he wrote, reiterating its Outperform rating on Tesla stock and $500 per share price target.

Tesla CEO Elon Musk has responded to Ives’ suggestions with a brief comment on X. “Shut up, Dan,” Musk wrote.

Cathie Wood reiterates trust in Musk and Tesla board

Meanwhile, Ark Investment Management founder Cathie Wood expressed little concern over Musk’s latest controversies. In an interview with Bloomberg Television, Wood said, “We do trust the board and the board’s instincts here and we stay out of politics.” She also noted that Ark has navigated Musk-related headlines since it first invested in Tesla.

Wood also pointed to Musk’s recent move to oversee Tesla’s sales operations in the U.S. and Europe as evidence of his renewed focus in the electric vehicle maker. “When he puts his mind on something, he usually gets the job done,” she said. “So I think he’s much less distracted now than he was, let’s say, in the White House 24/7,” she said.

TSLA stock is down roughly 25% year-to-date but has gained about 19% over the past 12 months, as noted in a StocksTwits report.

Investor's Corner

Cantor Fitzgerald maintains Tesla (TSLA) ‘Overweight’ rating amid Q2 2025 deliveries

Cantor Fitzgerald is holding firm on its bullish stance for the electric vehicle maker.

Cantor Fitzgerald is holding firm on its bullish stance for Tesla (NASDAQ: TSLA), reiterating its “Overweight” rating and $355 price target amidst the company’s release of its Q2 2025 vehicle delivery and production report.

Tesla delivered 384,122 vehicles in Q2 2025, falling below last year’s Q2 figure of 443,956 units. Despite softer demand in some countries in Europe and ongoing controversies surrounding CEO Elon Musk, the firm maintained its view that Tesla is a long-term growth story in the EV sector.

Tesla’s Q2 results

Among the 384,122 vehicles that Tesla delivered in the second quarter, 373,728 were Model 3 and Model Y. The remaining 10,394 units were attributed to the Model S, Model X, and Cybertruck. Production was largely flat year-over-year at 410,244 units.

In the energy division, Tesla deployed 9.6 GWh of energy storage in Q2, which was above last year’s 9.4 GWh. Overall, Tesla continues to hold a strong position with $95.7 billion in trailing twelve-month revenue and a 17.7% gross margin, as noted in a report from Investing.com.

Tesla’s stock is still volatile

Tesla’s market cap fell to $941 billion on Monday amid volatility that was likely caused in no small part by CEO Elon Musk’s political posts on X over the weekend. Musk has announced that he is forming the America Party to serve as a third option for voters in the United States, a decision that has earned the ire of U.S. President Donald Trump.

Despite Musk’s controversial nature, some analysts remain bullish on TSLA stock. Apart from Cantor Fitzgerald, Canaccord Genuity also reiterated its “Buy” rating on Tesla shares, with the firm highlighting the company’s positive Q2 vehicle deliveries, which exceeded its expectations by 24,000 units. Cannacord also noted that Tesla remains strong in several markets despite its year-over-year decline in deliveries.

SpaceX’s Crew-11 mission targets July 31 launch amid tight ISS schedule

EV fans urge Tesla to acquire Unplugged Performance for edge in fleet and security industry

Tesla debuts hands-free Grok AI with update 2025.26: What you need to know

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoTesla investors will be shocked by Jim Cramer’s latest assessment

-

Elon Musk3 days ago

Elon Musk3 days agoxAI launches Grok 4 with new $300/month SuperGrok Heavy subscription

-

Elon Musk5 days ago

Elon Musk5 days agoElon Musk confirms Grok 4 launch on July 9 with livestream event

-

News1 week ago

News1 week agoTesla Model 3 ranks as the safest new car in Europe for 2025, per Euro NCAP tests

-

Elon Musk1 week ago

Elon Musk1 week agoxAI’s Memphis data center receives air permit despite community criticism

-

News2 weeks ago

News2 weeks agoXiaomi CEO congratulates Tesla on first FSD delivery: “We have to continue learning!”

-

News2 weeks ago

News2 weeks agoTesla sees explosive sales growth in UK, Spain, and Netherlands in June

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoTesla scrambles after Musk sidekick exit, CEO takes over sales