Investor's Corner

Tesla streamlined Model 3 battery pack production time by 96%, says Elon Musk

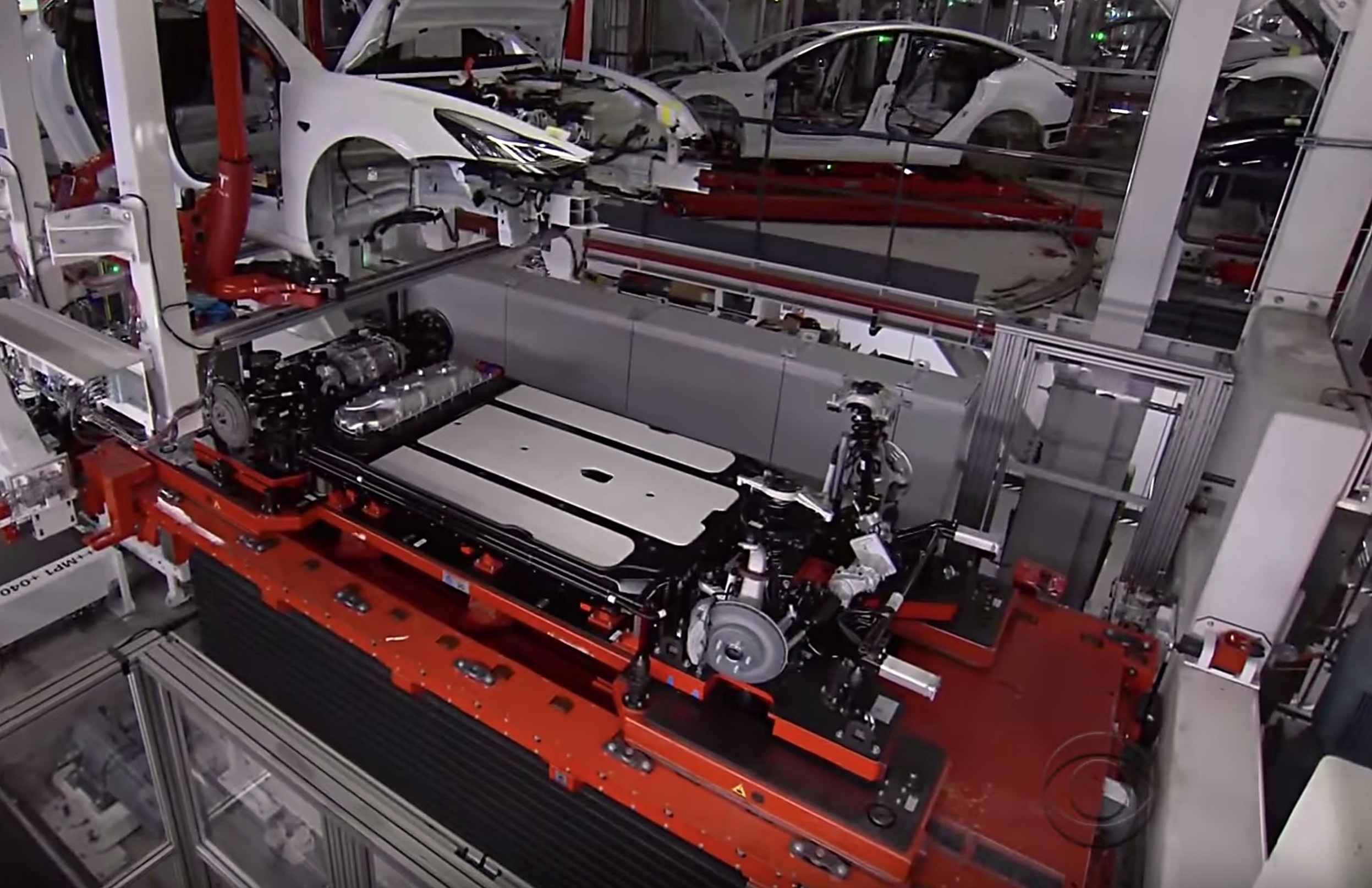

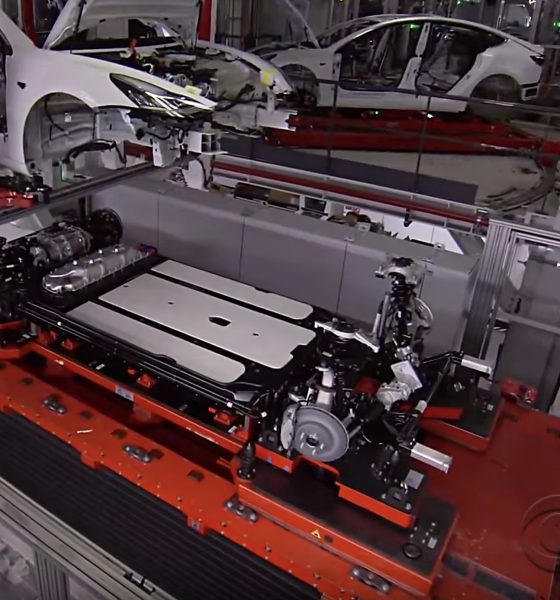

Tesla CEO Elon Musk stated during Wednesday’s Q1 2018 earnings call that the company has managed to reduce the time it takes to produce a Model 3 battery pack by 94%, from 7 hours to under 17 minutes. According to Musk, addressing the over-generalization of the Model 3’s design, as well as the excessive automation in Gigafactory, proved beneficial to the improvement in the manufacturing rate of the car’s battery packs.

“This still remains to be fixed, but in any case, overgeneralizing the design. For example, the current battery pack has a port for front drive units, which we then put a steel blanking plate on. So essentially, we punched a hole in it and put a blanking plate at the hole. And (we had to) do that for all rear drive unit cars, which is kinda crazy.

“It would have added cost, it would have added a manufacturing step, it would have added a failure mode; and four ports was unnecessary… That’s changed. So, the result was we had a rapid improvement in battery pack production, from taking 7 hrs to make a pack 3 weeks ago to under 17 minutes now. We’re able to also achieve a sustained rate of 3,000 vehicles a week, so we’re actually slightly ahead in battery module and pack production than expected.”

With the optimizations to the line in place, Musk revealed that Tesla is now producing 3,000 battery packs per week at the Nevada Gigafactory, with peak hours of production hitting a rate of 5,000 per week.

“In the last 24 hours at the Gigafactory, we managed to keep a sustained rate of over 3,000 packs per week. We actually reached a peak hour, extrapolated outward would be a rate of over 5,000 cars per week… Every hour is as good as its peak. If you can achieve it even once in an hour, then with continued refinement of the system, and improved operational time of the machinery, you can achieve that sustained rate with more refinement.”

Musk reiterated his previous statement about the company automating too much of its production line. According to Musk, Tesla “went too far and automated some pretty silly things,” including an incredibly complex “fluff machine” that ended up making production complicated.

“One of the things we’ve found is that there are some things that are very well suited to manual operations, and there are some things are very well suited to automated operations. The two should not be confused. We did go too far in the automation front, and automated some pretty silly things.

“One example would be, we have these fiberglass mats on top of the battery pack. They’re basically fluff. We tried to automate the placement and bonding of fluff to the top of the battery pack, which was ridiculous. ‘Flufferbot,’ which was really an incredibly difficult machine to make work. Machines are not good at picking up pieces of fluff. Hands are way better at doing that.

“So we had this super-complicated machine, using a vision system to try and put a piece of fluff on a battery pack. The line kept breaking down because Flufferbot would frequently fail to pick up the fluff, or put it in a random location. So, that was one of the silliest things we’ve found.”

The revelations about the improvements in the pace of Model 3 battery pack production are in line with Elon Musk’s recent statements about relying too much on automation. Musk mentioned this in an interview with Gayle King of CBS This Morning, and later in a tweet, where he coyly stated that humans are “underrated.”

Nevertheless, Tesla pointed to strategic automation as key in its Q1 Update Letter. The company, for one, credits the quality improvements in the Model 3 line to the automation that is involved in manufacturing the vehicles. Tesla expects the Model 3 line to be optimized once more after a planned 10-day shutdown in production during the second quarter. With a hiring ramp underway, Tesla is aiming to adjust overtime hours and staffing levels to meet its production goals even further.

Tesla’s first-quarter earnings for 2018 saw the electric car maker posting $3.4 billion in revenue and beating earnings estimates with a loss of $568 million. Losses per share was listed at -$3.35 per share, lower than Wall Street estimates of -$3.58 per share.

Lucid CEO Silvio Napoli responded to rumors of an imminent bankruptcy that was reportedly being mulled after a report stated the automaker was working with the firm AlixPartners to iron out its next steps.

The company felt a massive loss on Wall Street yesterday, as the report essentially pushed the stock down as much as 55 percent on Tuesday.

The report, published initially by Eletric-Vehicles.com, claimed Lucid was essentially in dire straits and was told by AlixPartners, a commonly used restructuring advisor, to either take shares private or file for Chapter 11 bankruptcy protection.

Lucid’s head of Communications, Nick Twork, immediately challenged the report and stated the company “has sufficient liquidity to carry its operations well into next year.”

Now, the company’s CEO is chiming in as well, stating that the report is “so far from the facts that they require a direct response.”

Napoli said:

“Lucid is not considering bankruptcy or a transaction to take the company private. Those reports are false. The Board did not explore either scenario. Period.

As disclosed in our most recent quarterly filing, Lucid has sufficient liquidity to fund its operations well into next year.

We work with outside advisors to improve operational performance and execution. They are not advising Lucid on a take-private transaction or bankruptcy, and any suggestion that they have recommended either course of action to management or the Board is false.

My priority is clear: turn this company around. That is where the leadership team and I are focused.

I look forward to providing a full update during our quarterly earnings call on August 4th.”

🚨 Lucid CEO Silvio Napoli calls rumors of financial issues “so far from the facts that they require a direct response.”

Read his full remarks here: https://t.co/t3Pg1NHvzy pic.twitter.com/LvHUPhO4Qf

— TESLARATI (@Teslarati) July 15, 2026

It seems pretty clear that Lucid is confident things will be okay, and, to be honest, they should not have much to worry about, especially considering the company has been backed by the Saudi Public Investment Fund (PIF) for years. It has solid financial backing, and its sales, while weak, are pretty much right on par with a company of this age.

Lucid also sent a Cease & Desist letter to the publication for their report.

Lucid shares have rebounded nicely and are up nearly 21 percent at the time of publication. As soon as the company dispelled the rumors of bankruptcy yesterday, the stock began to climb back toward more reasonable levels.

Electric vehicle maker Lucid Group has denied rumors of an imminent bankruptcy after a report from this morning sent the stock on a dramatic drop on Wall Street, seeing losses of more than 40 percent during trading hours.

Lucid’s Director of Communications, Nick Twork, responded to the report from Eletric-Vehicles.com, which stated the company’s restructuring advisor, AlixPartners, was asked to review two decisions: taking Lucid shares private or filing for Chapter 11 bankruptcy protection.

The report also claims AlixPartners told the Lucid board to “concentrate on Gravity production while improving its quality, and to temporarily hold back the Lucid Air, the sedan that has defined the company since its launch.”

Twork said:

$LCID The rumors are completely false. The company has sufficient liquidity to carry its operations well into next year, as recently published in its last quarterly filings, and it has not formed any special Board committee to explore the scenarios reported today. Our focus is…

— Nick Twork (@ntwork) July 14, 2026

Shares rebounded after the response to the report, halving its losses as the trading day neared 3 p.m. Eastern.

Lucid has struggled to get its sales off the ground and into more respectable numbers, but the company is in its early years, when things are hard to begin with. It is also backed by several notable investors, including the Saudi Public Investment Fund (PIF), which has nearly limitless money and likely would not ditch an investment of this size so soon.

Lucid shares were down just 14 percent at the time of publication, a far cry from the 55 percent its losses topped out at during the day.

Tesla received a price target upgrade just on the heels of what was a crazy successful quarter for its automotive business, as the company reported a delivery beat of over 15 percent for Q2.

Jefferies analysts are upping Tesla’s price target (NASDAQ: TSLA) to $400 from $375, while maintaining their “Hold” rating on shares, and the strong automotive deliveries from Q2 is a big reason. However, there are some other catalysts that Jefferies believes position Tesla for a strong position in the second half of the year.

Strong Deliveries

Tesla reported 480,000 deliveries for Q2, while Wall Street was between 395,000 and 405,000, as an overall consensus. It was an incredibly strong quarter from a delivery perspective, and Tesla sold well more than it produced during the three months.

Tesla crushes Wall Street expectations, beats delivery estimates by over 15 percent

While vehicle deliveries are not necessarily looked at in the light that they used to be, Tesla still maintains a lot of advantages for keeping deliveries strong. With the loss of the $7,500 EV Tax Credit last year, Tesla still maintains a strong demand case for its EVs.

Robotaxi Performance

Tesla has been operating Robotaxi for over a year now, as it launched in Austin in mid-2025. That program has expanded to Houston and Dallas, the San Francisco Bay Area, and, most recently, Miami, Florida, the suite’s first appearance in the Sunshine State.

While the Robotaxi suite is still in its early phases and Tesla is working through things like fleet size and wait times, the company has been able to undercut the pricing of its competitors and has a great safety record.

Merger Speculation with Tesla and SpaceX

This is perhaps the biggest topic that many are speaking about with Tesla and SpaceX, and it is the one thing that seems to be on the mind of every investor.

Jefferies warns that growing talk of a Tesla-SpaceX merger could cause Tesla stock to trade more like a SpaceX proxy, which may disconnect it from underlying automotive fundamentals. SpaceX has a lot going for it, especially its compute deals that have been widely publicized as of late.

Profitability in New Projects Could Take Some Time

Tesla has a few long-term ventures in the pipeline, most notably the Optimus project and Robotaxi, which is launched but will take several years to expand to a meaningful level that resonates with everyday people.

This is something that investors need to be careful of. Tesla’s projects could take some time to round out, so Jefferies advises that these may carry initial losses, rather than immediate profit. Seasoned Tesla investors have echoed something like this for a long time; they knew going in it would not be an open-and-shut strategy. It was going to take time.

These new projects are no different.

NTSB findings on fatal Tesla crash tell a very different story

Elon Musk’s Texas ranch to showcase the lifelong work that changed the world