News

Elon Musk pegs SpaceX BFR program at $5B as NASA’s rocket booster nears $5B in cost overruns

At the same time as NASA’s overrun-stricken Space Launch System (SLS) continues to limp towards its continuously delayed launch debut, now tentatively expected no earlier than (NET) 2021, SpaceX is forging ahead with the development of an equivalently capable launch vehicle known as BFR, comprised of a spaceship (BFS) and booster (BFB).

During a September 17th update to the next-gen SpaceX rocket’s steady progress, CEO Elon Musk offered a rough cost estimate of $5B to complete its development – no less than $2B and no more than $10B. According to NASA’s Office of the Inspector General (OIG), Boeing – primary contractor for NASA’s SLS “Core Stage” or booster – is all but guaranteed to burn through a minimum of $8.9B between 2012 and the rocket’s tentative 2021 launch debut.

NASA is finally (officially) acknowledging that EM-1, the maiden launch of SLS, will slip until at least June 2020. Sources tell us to expect another slip to 2021, official or not.https://t.co/CYf9SqbhBY

— Eric Berger (@SciGuySpace) October 3, 2018

Originally contracted in 2014 to complete SLS booster development, production, and preparation by 2018 at a cost of $4.2B, Boeing has overrun its budget by a bit less than 50% (up to $6.2B) and overshot its scheduled launch debut by more than 2.5 years. Per an October 10th audit of the SLS booster program, NASA OIG has reasonably concluded that Boeing will pass that $6.2B expenditure estimate – meant to last until 2021 – in December 2018, meaning that at least an additional $2.7B will be required from NASA between now and 2021 if SLS is to have a chance at launching that year.

In other words, compared to Boeing’s first serious 2014 contract for the SLS Core Stages – $4.2B to complete Core Stages 1 and 2 and launch EM-1 in Nov. 2017 – the company will ultimately end up 215% over-budget ($4.2B to $8.9B) and ~40 months behind schedule (42 months to 80+ months from contract award to completion). Meanwhile, as OIG notes, NASA has continued to give Boeing impossibly effusive and glowing performance reviews to the tune of $323 million in “award fees”, with grades that would – under the contracting book NASA itself wrote – imply that Boeing SLS Core Stage work has been reliably under budget and ahead of schedule (it’s not).

-

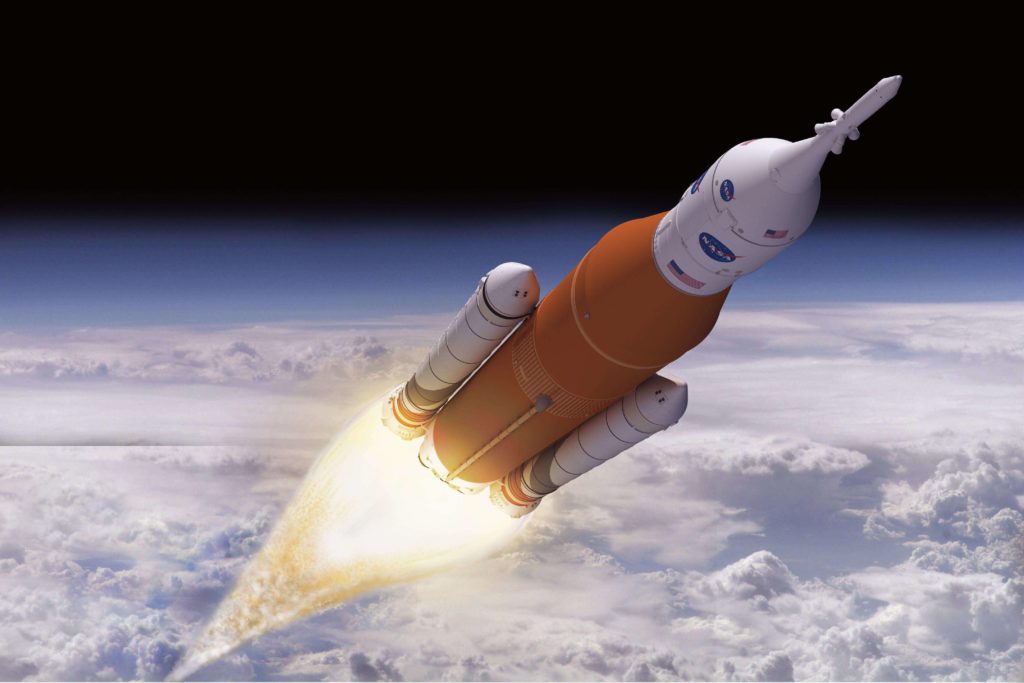

- SLS Block 1. (NASA)

-

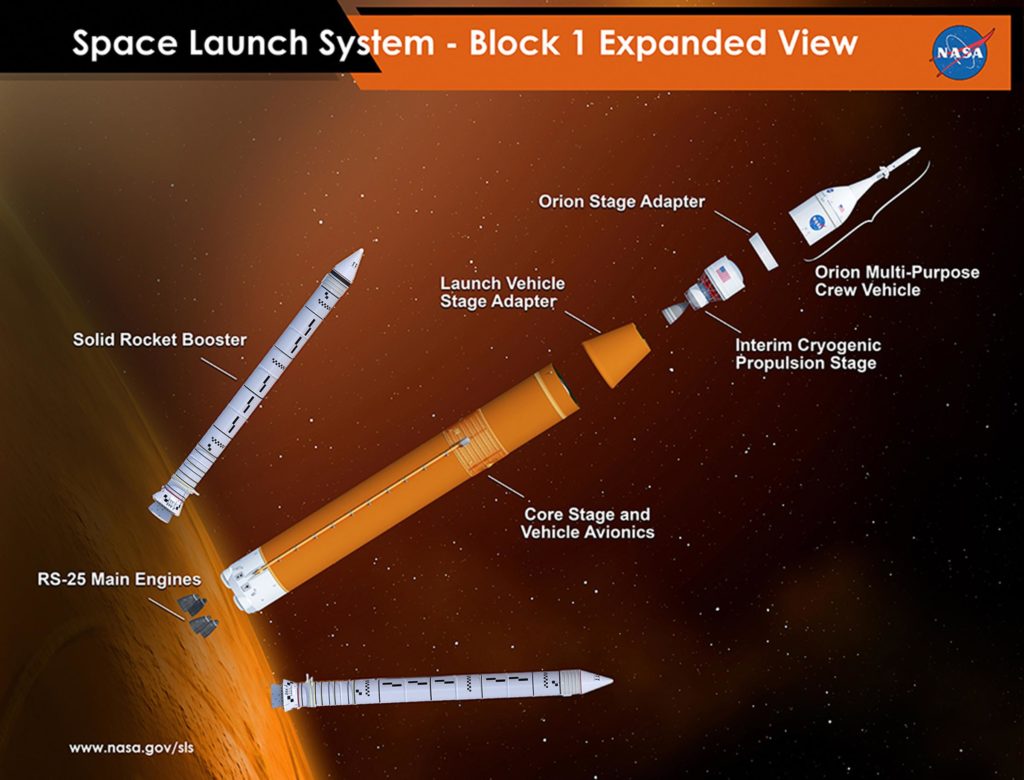

- An overview of SLS. (NASA)

-

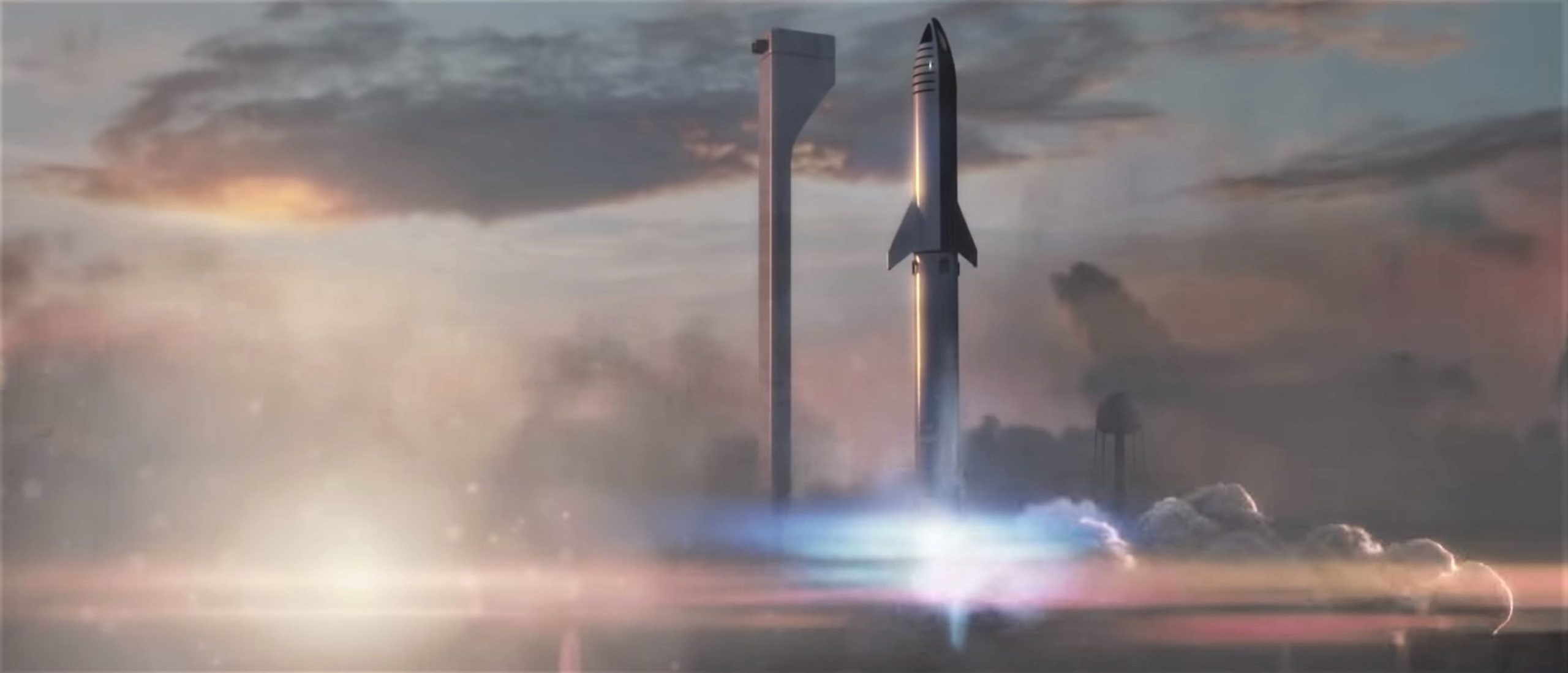

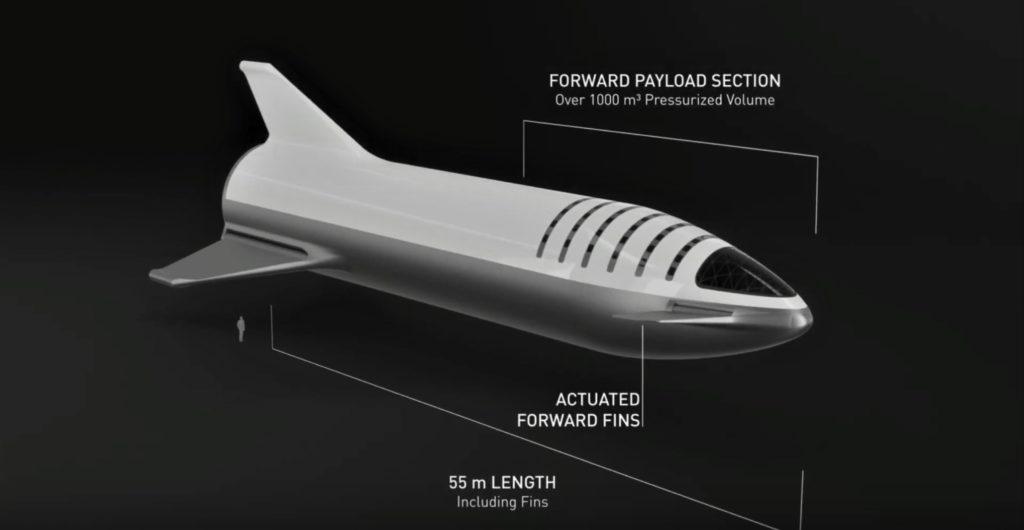

- Rockets are perhaps even more capital intensive. (SpaceX)

-

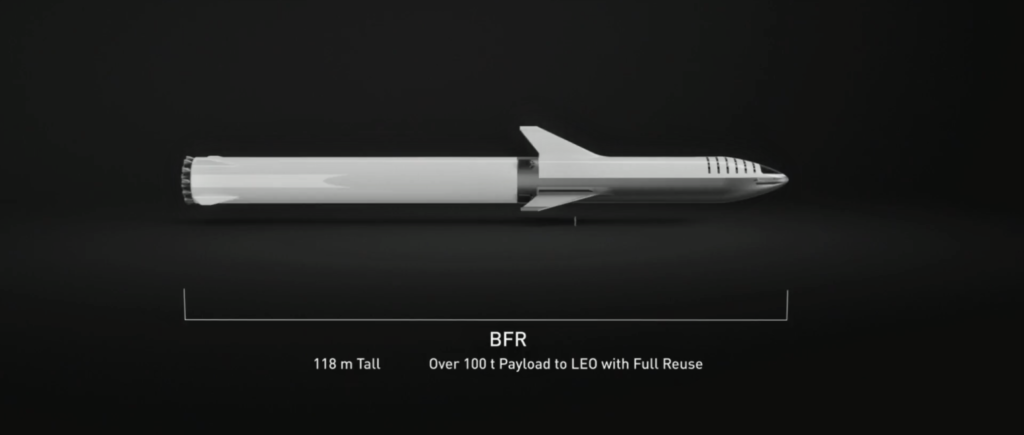

- BFR 2018’s Spaceship, BFS. (SpaceX)

The “Satisfactory” Stuff

In reality, Boeing has not once been under budget or ahead of schedule during any of 6+ NASA performance reviews.

-

-

“Boeing should have received a “satisfactory” rating for [two review periods]; a “good” rating for [one review period]; and an “unsatisfactory” rating (no award fee) for [the 2017 review period].”

Instead, NASA has given Boeing three “Very Good” (nearly perfect) reviews and three “Excellent” (perfect) reviews over the last 6 years, ultimately dispersing $323M of pure-profit “award fees” thanks to those grades, while the OIG firmly disputes Boing’s worthiness for at least $65M of that sum.

It is pretty pathetic when the only response that @BoeingSpace can muster via @BKingDC at its #politicospace PR effort in response to a damning @NASA_SLS report by @NASAOIG is to dump on the Saturn V – a rocket that actually flew – and worked – half a century ago. https://t.co/daN91bzwpC

— NASA Watch (@NASAWatch) October 12, 2018

Boeing – recently brought to light as the likely source of a spate of egregiously counterfactual op-eds published with the intention of dirtying SpaceX’s image – also took it upon itself to sponsor what could be described as responses to NASA OIG’s scathing October 10th SLS audit. Hilariously, a Politico newsletter sponsored by Boeing managed to explicitly demean and belittle the Apollo-era Saturn V rocket as a “rickety metal bucket built with 1960s technology”, of which Boeing was the core stage’s prime contractor.

At the same time, that newsletter described SLS as a rocket that will be “light years ahead of thespacecraft [sic] that NASA astronauts used to get to the moon 50 years ago.” At present, the only clear way SLS is or will be “light years” ahead – as much a measure of time as it is of distance – of Saturn V is by continuing the rocket’s trend of endless delays. Perhaps NASA astronomers will soon be able to judge exactly how many “light years ahead” SLS is by measuring the program’s redshift or blueshift with one of several ground- and space-based telescopes.

Ultimately, this is a particularly effective bit of self-mockery in the context of rationale lately used by Boeing and NASA to shrug off the jaw-dropping Core Stage contract’s underperformance, missteps, schedule slips, and budget overruns, namely that building big, complex rockets is hard. NASA and Boeing, neither of which have any meaningful experience building big, complex rockets – aside from Saturn IB, Saturn V, and the Space Shuttle – thus should be given a break for reliably and dramatically underestimating the difficulties of doing so in the 21st century.

-

One of the most breathtaking things about the new SLS report is the response by NASA's Gerstenmaier. Essentially, he says, this a is a big, complex rocket. And it's hard to build this stuff.https://t.co/ou8SFhji6a

— Eric Berger (@SciGuySpace) October 10, 2018

Simultaneously, Boeing and NASA still continue to act as if they are the foremost global experts of building extremely large rockets and continue to throw pile upon pile of taxpayer billions at overpromised attempts to prove as much. It’s no more than a masochistic dream to imagine what could have been or might be if NASA instead redirected those billions towards US aerospace companies with track records of success through fixed-cost contracts or straight-up private funding (SpaceX and Blue Origin, primarily), but it’s often hard not to at least think about the possibilities.

For prompt updates, on-the-ground perspectives, and unique glimpses of SpaceX’s rocket recovery fleet check out our brand new LaunchPad and LandingZone newsletters!

Elon Musk

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it

The Boring Company’s new tunnel vehicle runs on Tesla Model 3 batteries and drive units.

The Boring Company just introduced a new piece of hardware, and it runs on parts pulled straight from a Tesla showroom. Liner Truck 3, unveiled in a post from the tunneling company’s official X account, is an all electric vehicle built around Tesla Model 3 battery packs and drive units, purpose built to move concrete tunnel segments to the boring machine face without a single person underground.

Introducing Liner Truck 3 — our latest fully electric tunnel vehicle.

– Tesla Model 3 battery and drive units

– Transports 22,000+ lb of concrete segments to the boring machine

– 28 miles of range

– 12 mph max operating speed

– Remotely piloted from Global OCC in Texas, with… pic.twitter.com/XB7FgSXnpy— The Boring Company (@boringcompany) August 7, 2026

The job itself is unglamorous but critical. Each precast segment run weighs more than 22,000 pounds, roughly the load of a full cement mixer, and Liner Truck 3 hauls that weight repeatedly between the surface staging area and wherever the Prufrock machine happens to be cutting.

The Boring Company said Liner Truck 3 is piloted remotely out of its Global Operations Control Center in Texas, extending the Zero-People-In-Tunnel approach the company has spent years building toward. An earlier version of a ZPIT liner truck was already tested at the company’s Bastrop, Texas research tunnels, and a factory tour released last month showed an employee flying a fully loaded liner truck with a PlayStation controller. Liner Truck 3 looks like the production version of that same idea, cleaned up and pushed into daily use.

The timing lines up with a company digging in more places than it ever has before. The Boring Company now has multiple Prufrock machines active or arriving in Nashville, where Music City Loop construction has been accelerating since February, and its Vegas Loop network keeps adding tunnel mileage on a near monthly basis. Every one of those projects depends on getting concrete segments to the cutting face fast enough to keep the boring machine from idling, which is exactly the bottleneck Liner Truck 3 is designed to remove.

-

It also reinforces something Tesla owners have watched happen gradually across Musk’s companies: passenger car hardware finding a second life in heavy equipment. Model 3 drive units already move people through the Vegas Loop, and now the same components are hauling concrete underground in Nashville and wherever The Boring Company digs next. Whether that kind of component reuse extends further into TBC’s equipment lineup, or into other Musk owned industrial hardware, is the next thing worth watching.

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

-

News

The Boring Company’s newest Vegas Station has a permit quietly waiting behind it

Sahara Las Vegas opened a new Vegas Loop station, joining an exclusive two resort transit club.

Sahara Las Vegas opened a new Vegas Loop station Thursday, giving The Boring Company’s underground transit system its northernmost stop yet on the Strip. The station sits at Sahara’s Paradise Road entrance, on the southeast corner of Las Vegas Boulevard and Sahara Avenue, and connects riders to the Las Vegas Convention Center, other Strip resorts on the network and, eventually, Harry Reid International Airport.

The addition makes Sahara the second resort, after Fontainebleau opened its own station in January, to get a stop built at street level rather than tucked into the property itself. Sahara now joins Westgate as the only two Strip resorts offering both a Vegas Loop station and a stop on the Las Vegas Monorail, giving guests two separate ways to get around without leaving the property.

The Boring Company just doubled its tunneling power in Nashville

The bigger news buried in Thursday’s announcement is what comes next. Boring Company has already secured its first permit to tunnel north of Sahara Avenue, extending the network beyond where it currently ends, even though permits to push the Loop toward downtown Las Vegas still haven’t been granted. Crews are also working on a two mile dual tunnel line running from Westgate to a planned station at 4744 Paradise Road, just north of Tropicana Avenue, that Las Vegas Convention and Visitors Authority CEO Steve Hill has said the company hopes to open in time for November’s Las Vegas Grand Prix.

Ridership has grown alongside the buildout. The Loop moved roughly 82,000 passengers during CONEXPO in early March, a total the company highlighted on its own X account at the time, and the system has now carried more than 4 million passengers through 11 open stations since it began running in 2021. The airport connector tunnels, meant to give the Loop a direct link to Harry Reid, have slipped past their original first quarter target and remain under construction, with Boring Company director Mike Baier saying that a full opening is still a few months out.

For Sahara, the calculation is straightforward. Convention traffic drives a large share of Loop ridership, and a station at the property’s front door gives conventiongoers one more reason to book rooms on the Strip’s north end instead of closer to the convention center itself.

-

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it

Elon Musk and SpaceX shrugs off the trading day Wall Street feared most