SpaceX

SpaceX competitor Arianespace criticized for lackluster response to Falcon 9’s success

Best known for the commercial success of its Ariane 5 workhorse rocket, European aerospace cooperative Arianespace was heavily critiqued in the latest annual report from France’s Cour des comptes (Court of Auditors) for what is perceived as an unsustainable and overly cautious response to the swift rise of SpaceX’s affordable and reusable Falcon 9 rocket.

The Ariane 6 rocket is at least a year from launch, but already French auditors are asking how it's going to compete with SpaceX.https://t.co/7jCpGBrSXx

— Eric Berger (@SciGuySpace) February 6, 2019

First spotted and discussed by Ars Technica’s Eric Berger, the French auditor’s 2019 report featured a full volume – 1 of 30 – dedicated to Ariane 6, a prospective next-gen Arianespace rocket selected for development by the EU in 2014. Despite the fact that Ariane 6 is at least a full year away from its first launch, Cour des comptes is already questioning the rocket’s ability to successfully make headway into an increasingly competitive market, competition that has already had a direct and tangible impact on Arianespace’s Ariane 5 launch vehicle.

“More than 50% of Falcon 9’s lifetime launches occurred in the last ~12% (24 months) of the rocket’s operational career.”

While other competitors certainly do exist, the fact remains that that said increase in launch market competition can be almost singlehandedly attributed to the rapid entrance of SpaceX’s Falcon 9 rocket onto the commercial launch scene. Despite major stumbles in 2015 and 2016 as a result of Falcon 9’s CRS-7 and Amos-6 failures, SpaceX appears to have dealt with the organizational faults that allowed them to occur, culminating in an auspicious launch cadence over the course of 2017 and 2018. While Falcon 9 has technically been flying since mid-2010, a full 38 of the rocket’s 64 successful launches were completed in the last 24 months, meaning that more than 50% of Falcon 9’s launches have occurred in the last ~12% of the rocket’s operational life.

Critically, a number of European nations settled on Ariane 6 as the successor to Ariane 5 in 2014, at which point Falcon 9 had launched just 13 times (7 times commercially) and SpaceX was more than 12 months away from its first successful rocket recovery and ~30 months from its first commercial reuse. To the credit of Arianespace and the EU nations that supported the prospective Ariane 5 successor, Ariane 6 may have actually been able to reliably compete with Falcon 9’s pricing if it had begun launching within 12-24 months of the 2014 decision to build it and if SpaceX had simply sat on its laurels and ended development programs.

-

-

“This new launcher does not constitute a sustainable response in order to be competitive in a commercial market in stagnation,” the auditor’s report states. The Ariane 6 rocket design is too “cautious,” according to the report, relying on mostly traditional technologies.

— Eric Berger (@SciGuySpace) February 6, 2019

Coasting on the race track

Of course, neither of those prerequisites to Ariane 6’s success occurred. SpaceX successfully reused the same Falcon 9 booster three times in just six months by the end of 2018, while Falcon Heavy is set to attempt its first two operational launches just a few months from now. Ariane 6 is still targeting a launch debut no earlier than (NET) 2020, while a handful of extremely limited reusable rocket R&D programs continue to limp towards nebulous targets with minimal funding. Meanwhile, thanks to Arianespace’s French heritage and the major financial support of French space agency CNES, Cour des comptes is in the right to be highly critical of a ~$3.9B rocket development program likely to cost France at least $600M before the first launch.

-

- SpaceX has now been routinely reusing Falcon 9 rockets on commercial missions for nearly two years. (SpaceX)

-

- As of January 2019, flight-proven Falcon 9 boosters have performed 19 commercial launches since March 2017. (SpaceX)

-

- Nearly 60% of SpaceX’s 2018 launches were flown on flight-proven Falcon 9 boosters. (SpaceX)

-

- Falcon 9 B1046 became the first SpaceX booster to launch three separate times in early-December 2018. (Pauline Acalin)

Once Ariane 6 is ready to launch, it’s aspirational pricing will all but guarantee an inability to compete on an even global playing field. Divided into two versions, A62 and A64, Ariane 6 will cost at least 75 million Euros (~$85M) for performance equivalent to SpaceX’s Falcon 9 in its reusable configuration (base price: $62M), while the heavier A64 variant – capable of placing two heavy satellites (11,500 kg) into geostationary transfer orbit – will cost at least 90 million Euros (~$102M) per launch. Admittedly, $102M to launch a duo of large geostationary satellites would be easily competitive with Falcon 9 with per-customer costs around $50M, but this only holds true if the imminent commercial introduction of Falcon Heavy (list price: $90M) is ignored.

However, the market for large geostationary satellites has plummeted into the ground in the last two years, over the course of which just 12 have been ordered. Arianespace thus faces a conundrum where its cheaper Ariane 62 rocket is already too expensive to compete commercially and the potentially competitive Ariane 64 variant is only competitive for a commercial launch market that has withered to barely a third of its nominal demand in just two years time. Acknowledged by France’s auditors (and noted by Mr. Berger), the most probable outcome for Ariane 6 is one in which the very existence of the rocket will be predicated upon continual annual subsidies from the European Space Agency (ESA) in order to make up for the rocket’s inability to sustain commercial orders beyond a handful of discounted shoo-in contracts.

Check out Teslarati’s newsletters for prompt updates, on-the-ground perspectives, and unique glimpses of SpaceX’s rocket launch and recovery processes!

-

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

-

Elon Musk

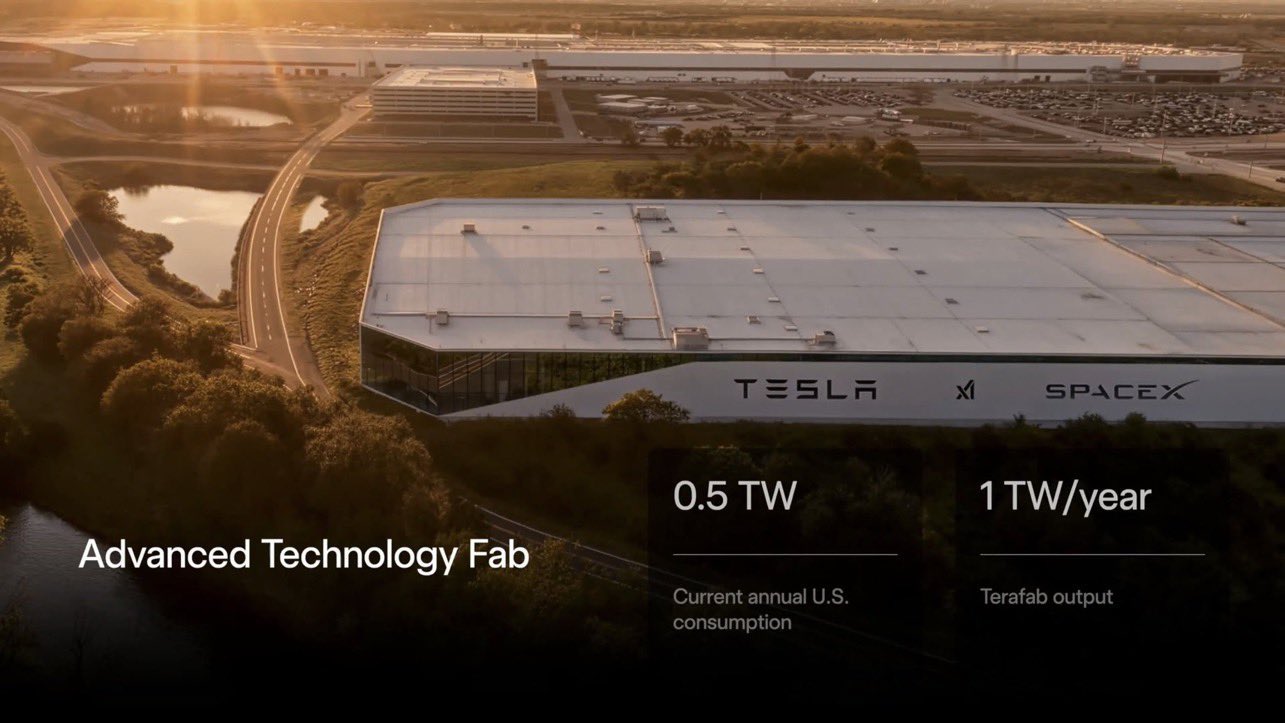

Tesla’s mysterious Robovan makes a sneak peek with Optimus in Terafab video

Elon Musk shared a new Terafab video showing Optimus, Robovans, and a stunningly futuristic campus.

Elon Musk posted a new video of Terafab on X Thursday morning, and the most eye-catching details in it were not the building itself, but two products still awaiting production: Optimus and the Robovan.

The concept render, credited to SpaceX, shows Optimus robots working the grounds of the roughly 2.5-mile-long facility planned for the Gibbons Creek site in Grimes County, while a Robovan glides along an elevated roadway cutting through the building itself, sharing the frame with a Tesla Semi and a Cybercab.

Robovan is the boxy, driverless people and cargo mover Musk unveiled alongside Cybercab at Tesla’s “We, Robot” event in October 2024. He pitched it as a way to move up to 20 passengers at once, or handle freight instead, at a target cost he claimed could fall under a dollar a mile, with no steering wheel or pedals, the same layout as Cybercab. Nearly two years later, Robovan still has no confirmed production timeline and has not shown up in any factory footage, which makes Thursday’s render one of the only recent looks at the vehicle in any form.

Terafab Texas will be the largest and most valuable building on Earth by far.

And it will be stunningly beautiful. pic.twitter.com/4NweOqTL7y

— Elon Musk (@elonmusk) August 6, 2026

Optimus has moved further along. Tesla began converting Fremont’s old Model S and Model X assembly line into a Gen 3 Optimus production line earlier this year, and Musk visited the site on July 1 to mark the changeover. A second, larger Optimus plant is under construction at Giga Texas, targeting volume production in summer 2027 and eventual capacity of 10 million units a year. Tesla AI lead Ashok Elluswamy said this month the robot has “big shoes to fill” in replacing the S and X line, while Musk has repeatedly called Optimus the company’s biggest product of any kind, with a long-term price he has pegged between $20,000 and $30,000.

-

Check out the “Robovan” from @Tesla

📸: @Teslarati pic.twitter.com/D4es2i9NUe

— TESLARATI (@Teslarati) October 11, 2024

“Terafab Texas will be the largest and most valuable building on Earth by far,” Musk wrote alongside the clip. “And it will be stunningly beautiful.”

One quote post summed up the reaction: “Futuristic scene with RoboVan + Cybercab + Tesla Semi + Optimus.”

Beyond the vehicles, the architecture wrapped around them stands out too. The building’s facade is canted at sharp angles, with illuminated horizontal bands running through what appears to be a multi level interior visible from outside. Below the elevated roadway, pedestrians walk along a plaza next to a reflecting pool, and the skyline behind the campus is dotted with angular spires that read more like sculpture than infrastructure, a departure from the strictly utilitarian look of Gigafactory Texas or Starbase.

The timing tracks with what Terafab representative Riley Trennell told Grimes County residents on Wednesday, when he said renderings of the facility would be released “within days.” Musk’s post followed less than 24 hours later, and Texas Governor Greg Abbott’s office sent out its own release Thursday confirming the project. As Teslarati reported this morning, Terafab’s tax abatement agreements with Grimes County are now signed and active, and SpaceX has sent the county its first $10 million payment under that deal. The dollar figure tied to this phase of construction, per Reuters, is $16.8 billion, one of the first hard capital expenditure numbers attached to Terafab since Musk unveiled the joint Tesla-SpaceX-xAI venture in March.Reaction on X ranged from enthusiastic to skeptical. “God Bless Texas! Everything is bigger and better in Texas!” one reply read. Another was more measured: “Terafab in a decade…..”

Whether the finished building matches the render is a separate question from whether Musk wanted people talking about the render itself. Less than a day after posting, the video had already crossed 5.5 million views.

-

Elon Musk

Space finally faced the people living next to its next Terafab mega-project

SpaceX confirmed Terafab’s Grimes County site is locked in, with construction starting within months.

SpaceX and Terafab representatives sat across from Grimes County residents for the first time on Wednesday, telling a packed Commissioners Court room that the $55 billion chip manufacturing project is now a done deal at the Gibbons Creek Reservoir site.

The meeting followed a $10 million check SpaceX sent the county earlier this week, satisfying a payment deadline built into the tax abatement agreement both sides signed in June. Elon Musk shared a post on X confirming the payment, and County Judge Joe Fauth told the San Antonio Express-News his office deposited the check after it beat its deadline.

Wednesday’s session, first reported by KBTX, moved the project from paperwork to construction. Terafab representative Riley Trennell told residents the JETI tax break agreements with Iola ISD and Anderson-Shiro CISD are signed and active, and that civil work and foundation prep are starting almost immediately. Renderings of the facility could be released within days, he said, with construction beginning within months.

The foundations for an exciting future are being built in Texas. Next up: Terafab → https://t.co/jGg52Zhn5I pic.twitter.com/SNfSXNr2tb

— SpaceX (@SpaceX) August 6, 2026

Elon Musk launches TERAFAB: The $25B Tesla-SpaceXAI chip factory that will rewire the AI industry

Musk first announced Terafab in March as a joint venture between Tesla, SpaceX and xAI aimed at producing over a terawatt of AI compute annually, an amount that dwarfs the roughly 20 gigawatts the entire global chip industry produces today. Intel joined as a manufacturing partner in April. Musk has said the project needed its own day in the spotlight rather than being squeezed into an earnings call, and for months the Grimes County site remained unconfirmed even as reporting pointed there.

-

SpaceX attorney Buck Brannon used Wednesday’s meeting to note that the company’s abatement is roughly 78 percent, not the 100 percent some earlier reports suggested. In exchange, SpaceX will pay Grimes County a fixed $20 million a year for 35 years, a total of $710 million, which Brannon said exceeds the $14 million Tesla paid Travis County in 2025.

SpaceX also addressed environmental concerns that have followed the project since Musk’s Terafab partnership with Intel was announced. Representatives said Terafab will not raise electric bills for other ratepayers, will not deplete local water supplies and will not draw down the Navasota River. SpaceX confirmed it owns the Navasota River pumping station, which it plans to use to divert stormwater into the Gibbons Creek Reservoir, and said it will build its own natural gas plants to power the facility rather than pulling from the ERCOT grid.

Grimes County commissioners also approved an addendum letting county employees use ten approved AI chatbots for work, including Grok.

The real reason Elon Musk wants every car connected to space

Inside Tesla’s secretive $10 Billion “Project Crystal Sun” filing