News

Tesla market share explodes in Q1, overtaking BMW, Mercedes, and others

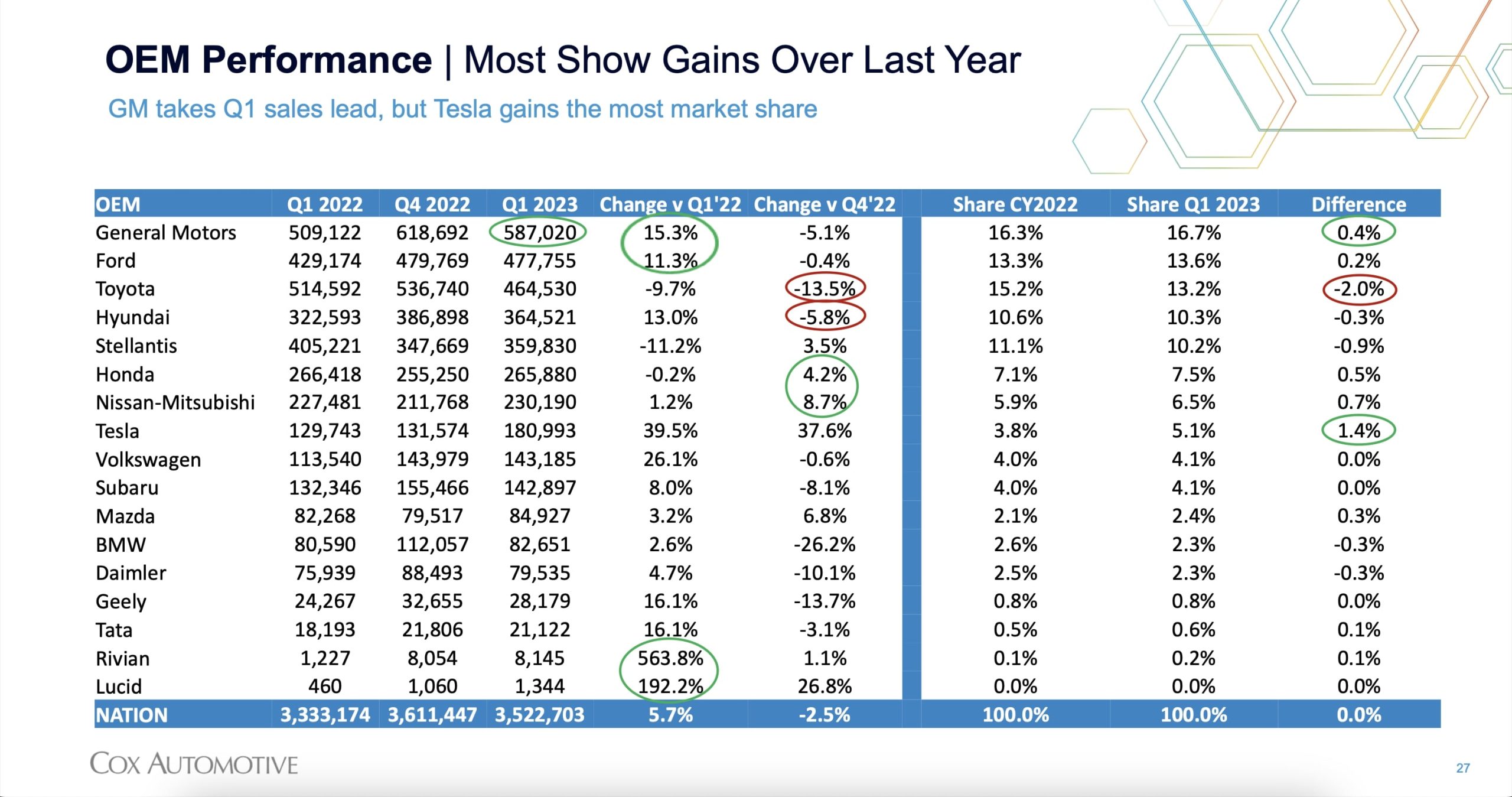

New data from Cox Automotive found that Tesla was the fastest-growing automaker in the industry regarding market share during Q1.

U.S. EV market share has almost always been dominated by Tesla, but in terms of the broader market, the EV leader has lagged behind legacy automakers. However, that standing has quickly changed as Tesla ramps production and EVs increasingly become more popular. Now, according to new data from Cox Automotive, Tesla was the fastest-growing automaker in terms of market share in the United States during Q1, even overtaking many legacy brands.

Cox Automotive found that during Q1, Tesla controlled roughly 5.1% of the overall market, placing it above brands like BMW, Mercedes, Mazda, Subaru, and even Volkswagen within the United States. This is a 1.4% jump compared to last year’s average, making Tesla the fastest-growing brand in this metric.

Cox had more good news for Tesla. While General Motors remains the leader in overall sales, controlling 16.7% of the market, Tesla was the fastest growing automaker in sales growth among brands, with over 2% market share, growing by 39.5% year over year, and by 37.6% compared to Q4 2022. However, it should be noted that Rivian was the fastest-growing automaker in sales overall, growing by 563.8% year over year.

Cox calculated that Tesla sold 180,993 vehicles in Q1 of this year.

Surprisingly, most brands saw sales contract in the first quarter of the year, particularly compared to Q4 of last year, which was a sales boom for many top brands. Nonetheless, General Motors, Ford, and Volkswagen saw some of the most significant year-over-year growth out of major brands, minus Tesla, growing by 15.3%, 11.3%, and 26.1%, respectively.

On the flip side, many brands had some of their worst performance in a long time, particularly Toyota, which saw its market share collapse by 2%. This aligns with previous results and is likely influenced by the fact that Toyota and Honda customers are some of the most likely to buy a Tesla.

-

-

Other brands that saw sales contract include Hyundai and Stellantis brands, which saw their market share drop by 0.3% and 0.9%. However, results from last year were not great indicators, as both brands saw growth in either year over year or compared to Q4 2022, but the reverse in the opposing metric.

What do you think of the article? Do you have any comments, questions, or concerns? Shoot me an email at william@teslarati.com. You can also reach me on Twitter @WilliamWritin. If you have news tips, email us at tips@teslarati.com!

-

-

News

The Boring Company’s newest Vegas Station has a permit quietly waiting behind it

Sahara Las Vegas opened a new Vegas Loop station, joining an exclusive two resort transit club.

Sahara Las Vegas opened a new Vegas Loop station Thursday, giving The Boring Company’s underground transit system its northernmost stop yet on the Strip. The station sits at Sahara’s Paradise Road entrance, on the southeast corner of Las Vegas Boulevard and Sahara Avenue, and connects riders to the Las Vegas Convention Center, other Strip resorts on the network and, eventually, Harry Reid International Airport.

The addition makes Sahara the second resort, after Fontainebleau opened its own station in January, to get a stop built at street level rather than tucked into the property itself. Sahara now joins Westgate as the only two Strip resorts offering both a Vegas Loop station and a stop on the Las Vegas Monorail, giving guests two separate ways to get around without leaving the property.

The Boring Company just doubled its tunneling power in Nashville

The bigger news buried in Thursday’s announcement is what comes next. Boring Company has already secured its first permit to tunnel north of Sahara Avenue, extending the network beyond where it currently ends, even though permits to push the Loop toward downtown Las Vegas still haven’t been granted. Crews are also working on a two mile dual tunnel line running from Westgate to a planned station at 4744 Paradise Road, just north of Tropicana Avenue, that Las Vegas Convention and Visitors Authority CEO Steve Hill has said the company hopes to open in time for November’s Las Vegas Grand Prix.

Ridership has grown alongside the buildout. The Loop moved roughly 82,000 passengers during CONEXPO in early March, a total the company highlighted on its own X account at the time, and the system has now carried more than 4 million passengers through 11 open stations since it began running in 2021. The airport connector tunnels, meant to give the Loop a direct link to Harry Reid, have slipped past their original first quarter target and remain under construction, with Boring Company director Mike Baier saying that a full opening is still a few months out.

For Sahara, the calculation is straightforward. Convention traffic drives a large share of Loop ridership, and a station at the property’s front door gives conventiongoers one more reason to book rooms on the Strip’s north end instead of closer to the convention center itself.

-

Elon Musk

Tesla’s mysterious Robovan makes a sneak peek with Optimus in Terafab video

Elon Musk shared a new Terafab video showing Optimus, Robovans, and a stunningly futuristic campus.

Elon Musk posted a new video of Terafab on X Thursday morning, and the most eye-catching details in it were not the building itself, but two products still awaiting production: Optimus and the Robovan.

The concept render, credited to SpaceX, shows Optimus robots working the grounds of the roughly 2.5-mile-long facility planned for the Gibbons Creek site in Grimes County, while a Robovan glides along an elevated roadway cutting through the building itself, sharing the frame with a Tesla Semi and a Cybercab.

Robovan is the boxy, driverless people and cargo mover Musk unveiled alongside Cybercab at Tesla’s “We, Robot” event in October 2024. He pitched it as a way to move up to 20 passengers at once, or handle freight instead, at a target cost he claimed could fall under a dollar a mile, with no steering wheel or pedals, the same layout as Cybercab. Nearly two years later, Robovan still has no confirmed production timeline and has not shown up in any factory footage, which makes Thursday’s render one of the only recent looks at the vehicle in any form.

Terafab Texas will be the largest and most valuable building on Earth by far.

And it will be stunningly beautiful. pic.twitter.com/4NweOqTL7y

— Elon Musk (@elonmusk) August 6, 2026

Optimus has moved further along. Tesla began converting Fremont’s old Model S and Model X assembly line into a Gen 3 Optimus production line earlier this year, and Musk visited the site on July 1 to mark the changeover. A second, larger Optimus plant is under construction at Giga Texas, targeting volume production in summer 2027 and eventual capacity of 10 million units a year. Tesla AI lead Ashok Elluswamy said this month the robot has “big shoes to fill” in replacing the S and X line, while Musk has repeatedly called Optimus the company’s biggest product of any kind, with a long-term price he has pegged between $20,000 and $30,000.

-

Check out the “Robovan” from @Tesla

📸: @Teslarati pic.twitter.com/D4es2i9NUe

— TESLARATI (@Teslarati) October 11, 2024

“Terafab Texas will be the largest and most valuable building on Earth by far,” Musk wrote alongside the clip. “And it will be stunningly beautiful.”

One quote post summed up the reaction: “Futuristic scene with RoboVan + Cybercab + Tesla Semi + Optimus.”

Beyond the vehicles, the architecture wrapped around them stands out too. The building’s facade is canted at sharp angles, with illuminated horizontal bands running through what appears to be a multi level interior visible from outside. Below the elevated roadway, pedestrians walk along a plaza next to a reflecting pool, and the skyline behind the campus is dotted with angular spires that read more like sculpture than infrastructure, a departure from the strictly utilitarian look of Gigafactory Texas or Starbase.

The timing tracks with what Terafab representative Riley Trennell told Grimes County residents on Wednesday, when he said renderings of the facility would be released “within days.” Musk’s post followed less than 24 hours later, and Texas Governor Greg Abbott’s office sent out its own release Thursday confirming the project. As Teslarati reported this morning, Terafab’s tax abatement agreements with Grimes County are now signed and active, and SpaceX has sent the county its first $10 million payment under that deal. The dollar figure tied to this phase of construction, per Reuters, is $16.8 billion, one of the first hard capital expenditure numbers attached to Terafab since Musk unveiled the joint Tesla-SpaceX-xAI venture in March.Reaction on X ranged from enthusiastic to skeptical. “God Bless Texas! Everything is bigger and better in Texas!” one reply read. Another was more measured: “Terafab in a decade…..”

Whether the finished building matches the render is a separate question from whether Musk wanted people talking about the render itself. Less than a day after posting, the video had already crossed 5.5 million views.

-

Cybertruck

Tesla Cybertruck production snaps back after ugly supplier fight

Cybertrucks are piling up again at Giga Texas after Tesla’s court win against a parts supplier.

Cybertruck production at Giga Texas is showing its first visible recovery since Tesla sued a supplier last month over withheld manufacturing tooling.

Aerial observer Joe Tegtmeyer flew over the Austin factory Wednesday morning and counted roughly 100 or more Cybertrucks filling the outbound lot, a sharp jump from the thin numbers seen in recent weeks. The flyover came a day after a judge granted Tesla a temporary restraining order against Angstrom Automotive Group, the parts supplier at the center of the dispute.

Tesla filed an emergency lawsuit in late July after Angstrom told the automaker it planned to close the Troy, Texas facility where Tesla’s die-cast tools, trim dies and other Cybertruck stamping equipment were housed. According to Tesla’s complaint, a shipment of 700 finished parts never left the building, and when Tesla sent representatives to retrieve its equipment, accompanied by law enforcement, they were turned away. Angstrom allegedly then asked for an extra $250,000 a week to keep operating, which Tesla’s filing described as holding its own property for ransom.

TESLA: U.S. District Judge Christopher R. Wolfe of the U.S. District Court for the Western District of Texas, Waco Division granted Tesla a Temporary Restraining Order and Writ of Replevin in its dispute with Angstrom Automotive (Case No. 6:26-cv-00477).

The order authorizes… https://t.co/E1DKcQSxMn pic.twitter.com/LR8aAiV2Og

— S.E. Robinson, Jr. (@SERobinsonJr) August 5, 2026

-

The restraining order gives Tesla immediate right of entry to Angstrom’s facility to recover the tooling. It is temporary, with a fuller hearing still to come, but the speed of Wednesday’s rebound suggests the Angstrom shortage was indeed the main bottleneck limiting Cybertruck output. Outbound lot counts are an imperfect measure of actual production, since finished trucks can sit for days before shipping, but a lot that full after a lean stretch is a meaningful signal.

Cybertruck output at Giga Texas has fluctuated all year as Tesla worked through supply issues and introduced new trims, including a cheaper Dual Motor AWD version that drew strong early demand.

The Boring Company’s newest Vegas Station has a permit quietly waiting behind it

Tesla’s mysterious Robovan makes a sneak peek with Optimus in Terafab video