Investor's Corner

Tesla Model 3 VIN registrations rocket past 100k mark as production approaches 6k/week

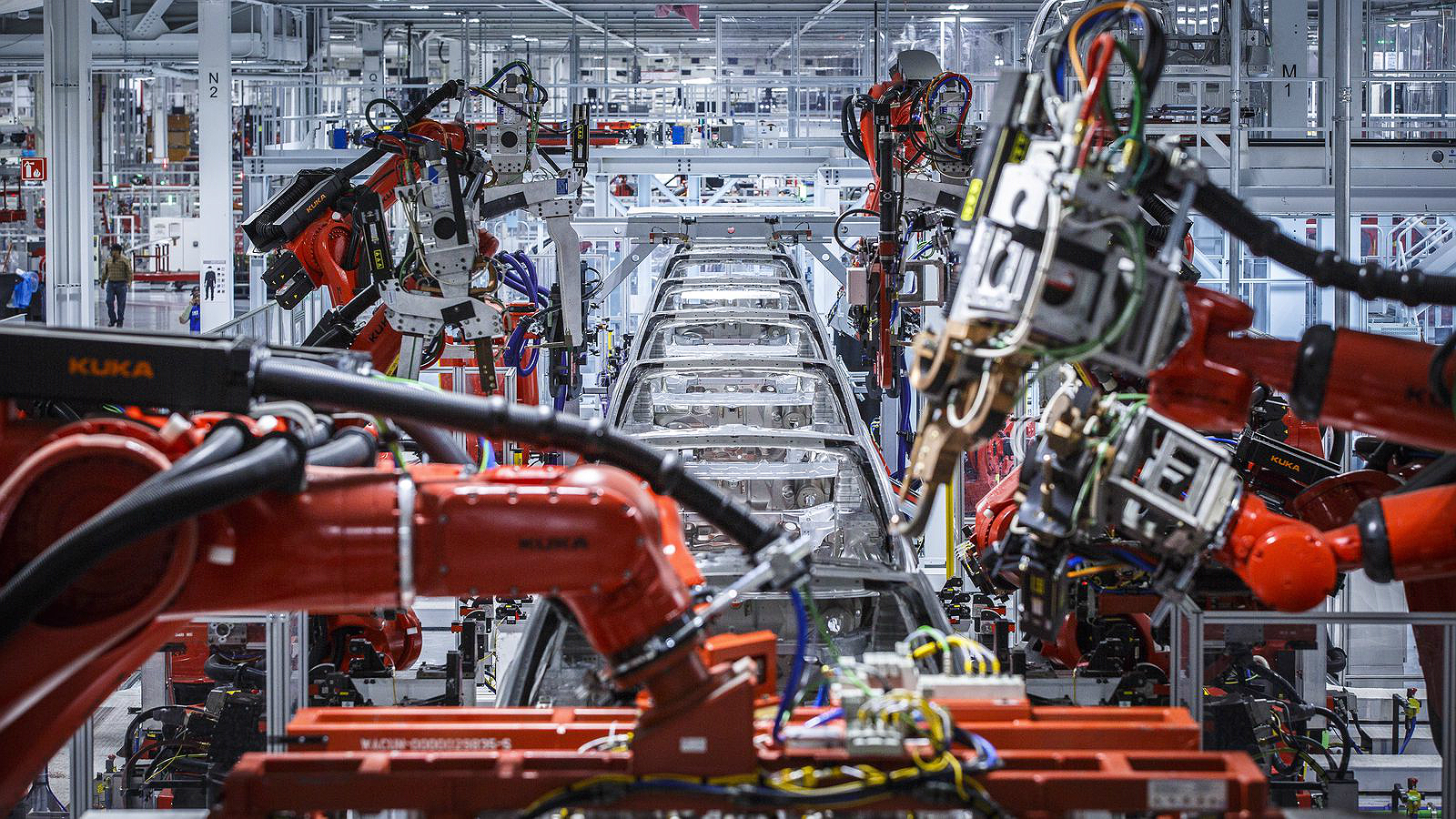

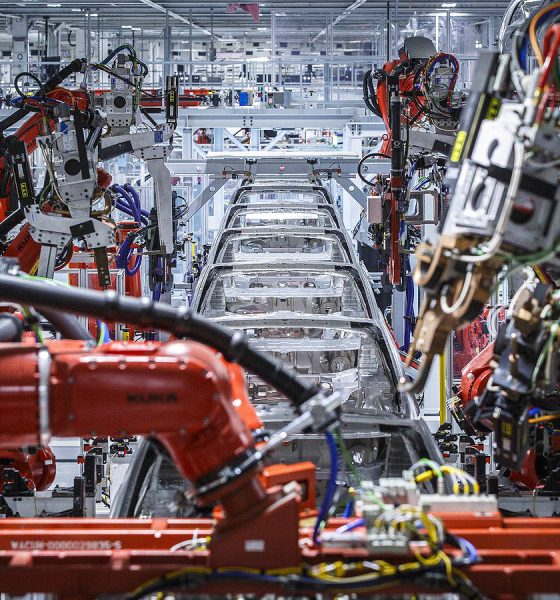

After spending more than a year deep in “manufacturing hell,” Tesla passed a milestone in its Model 3 production. The company registered two large batches of Model 3 VINs this weekend, effectively passing the 100,000-mark for the electric sedan’s filings.

Tesla’s 100,000 Model 3 VIN milestone comes roughly a week after the company registered a record 16,000 new VINs in a seven-day period. With the addition of the 2,207 registered this Saturday and 6,836 VINs registered on Sunday, Tesla has now filed a total of 108,188 Model 3 VINs since starting the production of the electric car last July.

#Tesla registered 2,207 new #Model3 VINs. ~100% estimated to be dual motor. Highest VIN is 101352. https://t.co/IKvPZI3hqC

— Model 3 VINs (@Model3VINs) August 18, 2018

#Tesla registered 6,836 new #Model3 VINs. ~73% estimated to be dual motor. Highest VIN is 108188. https://t.co/Wq0Y0kJLkL

— Model 3 VINs (@Model3VINs) August 19, 2018

The Model 3 ramp was an ambitious goal for Tesla, and it came at a great cost for the company and its CEO. In an interview last month, Elon Musk dubbed the Model 3 ramp was a “bet-the-company” situation, where the vehicle’s failure would have resulted in the fall of Tesla. The production ramp of the Model 3 has been anything but smooth as well, with Tesla facing bottleneck after bottleneck as it attempted to hit the hyper-aggressive manufacturing goals set forth by Elon Musk.

-

-

During the midsize electric car’s handover ceremony, Musk stated that Tesla would be aiming to hit a production rate of 5,000 Model 3 per week by the end of December 2017. This goal was eventually met, though it happened six months late. All this has exhausted Elon Musk, who noted in a recent interview with the New York Times that the past 12 months had been the most “difficult and painful” year of his career.

Even when Tesla hit its then-elusive goal of manufacturing 5,000 Model 3 in one week, reservations were abounding about the company’s capability to sustain its optimum production rate for the electric sedan. Despite these reservations, signs emerged in July that Tesla might be capable of maintaining its 5,000/week Model 3 ramp. Tesla started test drives for the Model 3 and introduced programs designed to deliver as many vehicles as possible, such as the 5-Minute Sign & Drive system. VIN registrations for the Model 3 picked up as well, with Tesla registering 19,000 new Model 3 VINs during the first half of the month.

Tesla’s capability to sustain its 5,000/week Model 3 production rate was highlighted by the company during its Q2 2018 earnings call, when Elon Musk mentioned that the Model 3 line sustained its 5000/week rate during “multiple weeks” in July. Since then, Tesla’s Model 3 ramp has exhibited even more encouraging signs. Bloomberg‘s production tracker, which has gotten more accurate over the past months (it was only ~2% off its Q2 estimates), now shows that Tesla is pacing to hit a production rate of 6,000 Model 3 weekly. As of writing, the publication’s tracker estimates that Tesla is producing 5,942 Model 3 per week.

![]()

The Model 3 production ramp is starting to win over Wall Street. Last week, even noted Tesla bear Toni Sacconaghi from Sanford C. Bernstein, who previously had a $265 price target for Tesla, raised his price target to $325 per share. Jefferies Financial Group, which also had a conservative $250 price target for the company, also raised its price target to $360 per share.

Perhaps the most notable vote of confidence for the Model 3 production ramp came from George Galliers of Evercore ISI, who was given an extensive tour of the Fremont factory, including the sprung structure-based GA4 set up on the facility’s grounds. According to Galliers, Tesla appears to be “well on the way” to hitting a sustained weekly production rate of 5,000-6,000 Model 3 per week. The Evercore ISI analyst also noted that Tesla’s current facilities appear to be fully capable of hitting 8,000 Model 3 per week in the future.

“Tesla seems well on the way to achieving a steady weekly production rate of 5,000 to 6,000 units per week. We are incrementally positive on Tesla following our visit. We have confidence in their production. We did not see anything to suggest that Model 3 cannot reach 6k units per week and 7k to 8k with very little incremental capital expenditure. Focusing on the fundamentals and setting aside talk of privatization, we are incrementally positive on Tesla following our visit,” the Evercore ISI analyst noted.

-

-

SpaceX (NASDAQ: SPCX) reported a beat in revenues and EBITDA in its first earnings call report while also minimizing losses as its business continues to gain momentum.

After its IPO in July, SpaceX saw some tough losses on Wall Street due to a major selloff after a delay in its 13th Starship test flight. The ship launched later that week and completed what was arguably the most successful IFT operation in the Starship program’s history.

Nevertheless, the company is continuing on and reported some encouraging financials while also promoting what appears to be a robust outlook moving forward in its Space, AI, and Connectivity divisions.

SpaceX to report first-ever earnings today: here’s what to expect

Earnings Results

- Revenues: $7.8 billion reported vs. $6.7 billion expected

- Adjusted EBITDA: $3.5 billion vs. $2 billion expected

- Net loss of $541 million, an improvement of $467 million from net loss of $1.0 billion

Additionally, CFO Bret Johnsen had these comments:

“2026 has been a momentous year so far, and the second quarter demonstrated the true power of SpaceX. Revenue growth accelerated across all our business segments and we delivered strong operating leverage, with significant margin expansion led by our new AI compute agreements. Our unparalleled leadership in launch, Starlink subscriber growth, new enterprise and government partnerships, and best-in-class AI infrastructure underscore our ability to drive meaningful scale and deliver attractive returns. As a newly public company, we are delighted to welcome our broad base of shareholders and bondholders. We ended the second quarter with $100 billion of cash, cash equivalents, and marketable securities, and $47.5 billion in backlog. This financial strength gives us substantial capacity to invest in Starship, Starlink Broadband and Mobile satellites, and our AI platform, while maintaining a disciplined long-term capital allocation framework.”

Space Business Highlights

SpaceX shared some of its biggest Space Business Highlights for Q2:

- Space revenues grew 55% sequentially and 29% year-over-year to $962 million, driven by a higher number of large customer launches and a favorable customer shift compared to the prior year

- Total costs and expenses for the Space segment were up by $389 million year-over-year, as we continued to accelerate R&D investments in our Starship program, which we believe will reduce the cost to orbit by 99% or more relative to the historical average, and unlock significant revenue potential across all business segments

- Leading launch provider for the world with 78 launches and 1,041 metric tons of mass to orbit deployed over the six months ended June 30, 2026, primarily allocated to Connectivity for the deployment of our Starlink constellation

- Starship V3 development continued to advance towards full and rapid reusability:

- Completed Starship V3’s first suborbital mission in May, Flight 12, which achieved a successful lift off from our new Starbase pad, a precision landing of Starship’s upper stage, and deployment of modified V2 Starlink satellites

- Subsequent to the second quarter, completed Starship Flight 13 in July, which achieved all flight objectives including deploying 20 production V3 satellites, demonstrating in-space relight of a Raptor engine, and executing the softest ever splashdown of Starship, providing critical views of an intact heatshield

SpaceX will report its earnings today at 4:30 P.M. EDT.

-

Elon Musk issued a second pointed warning to SpaceX short sellers on Tuesday, just hours before the company was set to release its first quarterly earnings as a publicly traded firm. Responding to a report highlighting elevated short interest, Musk wrote on X: “I try to warn them, but they just double down …”

The comment came as data from S3 Partners showed roughly 95 percent of available SPCX shares to borrow were on loan, translating to about 34 percent short interest as a percentage of the float. The stock has traded under pressure since its record-breaking IPO in June 2026, declining significantly from early peaks.

I try to warn them, but they just double down … 🤷♂️

— Elon Musk (@elonmusk) August 4, 2026

This marks the second such message from Musk in under three weeks.

On July 17, amid post-IPO volatility, he stated: “The survival probability of firms who maintain a significant short position in SpaceX over time is very low.” At that time, SPCX had fallen roughly 30 percent from its peak above a $2.6 trillion valuation, with short sellers reportedly realizing gains of about $8.7 billion.

-

Musk’s warning aligned with optimistic analyses projecting that Starship-driven cost reductions could enable a multi-trillion-dollar space economy through applications such as orbital solar power, asteroid mining, data centers, and Mars-related projects, positioning SpaceX as critical infrastructure.

SpaceX is scheduled to report second-quarter results after the market close later today, followed by a webcast. Analysts anticipate revenue near $6.9 billion, reflecting growth in Starlink, launch services, and AI-related segments. The earnings release precedes a major lockup expiration on August 6 that could free hundreds of millions of insider shares.

Musk has a long track record of confronting short sellers, particularly regarding Tesla, where he has argued that persistent bearish positions underestimate transformative technologies. Critics view his optimism as overly ambitious given near-term stock fluctuations, while supporters see temporary dips as opportunities in a longer-term expansion of the space economy.

As SpaceX opens its books to public scrutiny for the first time, the high short interest and Musk’s repeated cautions set the stage for heightened market attention on the results and management’s commentary.

Elon Musk’s space exploration company, SpaceX (NASDAQ: SPCX), is set to report its earnings for the second quarter today in what will be its first-ever earnings call since going public in July.

SpaceX is trading down roughly 25 percent from its IPO. These early stock signals are usually a bit tumultuous, and considering this is the first company actively launching rockets that is available on the stock exchange, investors might have a tendency to be a bit skittish.

However, there are going to be some details that investors will hear for the first time today on the earnings call. Here’s what to look for:

Wall Street Expectations

Revenue is expected to fall somewhere around $6.8 billion, and will be heavily driven by Starlink, which is SpaceX’s widely popular satellite internet platform that has been adopted by numerous airlines, cruise ships, and other maritime operations. It is also available for consumers at home or in their cars.

Earnings Per Share (EPS) expectations fall at a net loss of $0.23 per share. Wall Street sees this as a total net loss of roughly $1.9 billion.

EBITDA is expected to come in between $2 billion and $2.1 billion.

What Investors Want to Know

Tesla uses the Say platform to help work with both retail and institutional investors to answer relevant and quality questions that address concerns or questions that they might have.

-

However, SpaceX is doing things differently, as the company launched its own Investor Relations website where these questions are being fielded. Just like the Tesla questions, they seem to be less focused on the operational tasks and overall progress of the company, and more novelty.

Here are the top five:

- Has the team thought about what possibilities there are with your mascot Asteroid? Whether it’s starting additional foundations for kids in its name, helping kids learn about space, etc. Kids are our future, and Asteroid would be a fun and easy way to help.

- Baby Asteroid is already making a difference through charity around the world. Could SpaceX take it even further with programs that inspire kids to explore space?

- SpaceX has some legendary vehicle names. Would you ever allow the public to name a Starship, even knowing there is a 99% chance it becomes Shipy McShipface?

- When can we expect to see more footage of the Human Landing System?

- Will Asteroid (your mascot) go to Mars?

SpaceX will report its earnings today, August 4, at 4:30 P.M. EDT.

SpaceX reports beat in first earnings while minimizing losses

Elon Musk sends second warning to SpaceX shorts ahead of first earnings