Investor's Corner

Tesla (TSLA) receives “Buy” rating, $450 price target from Jefferies Financial Group

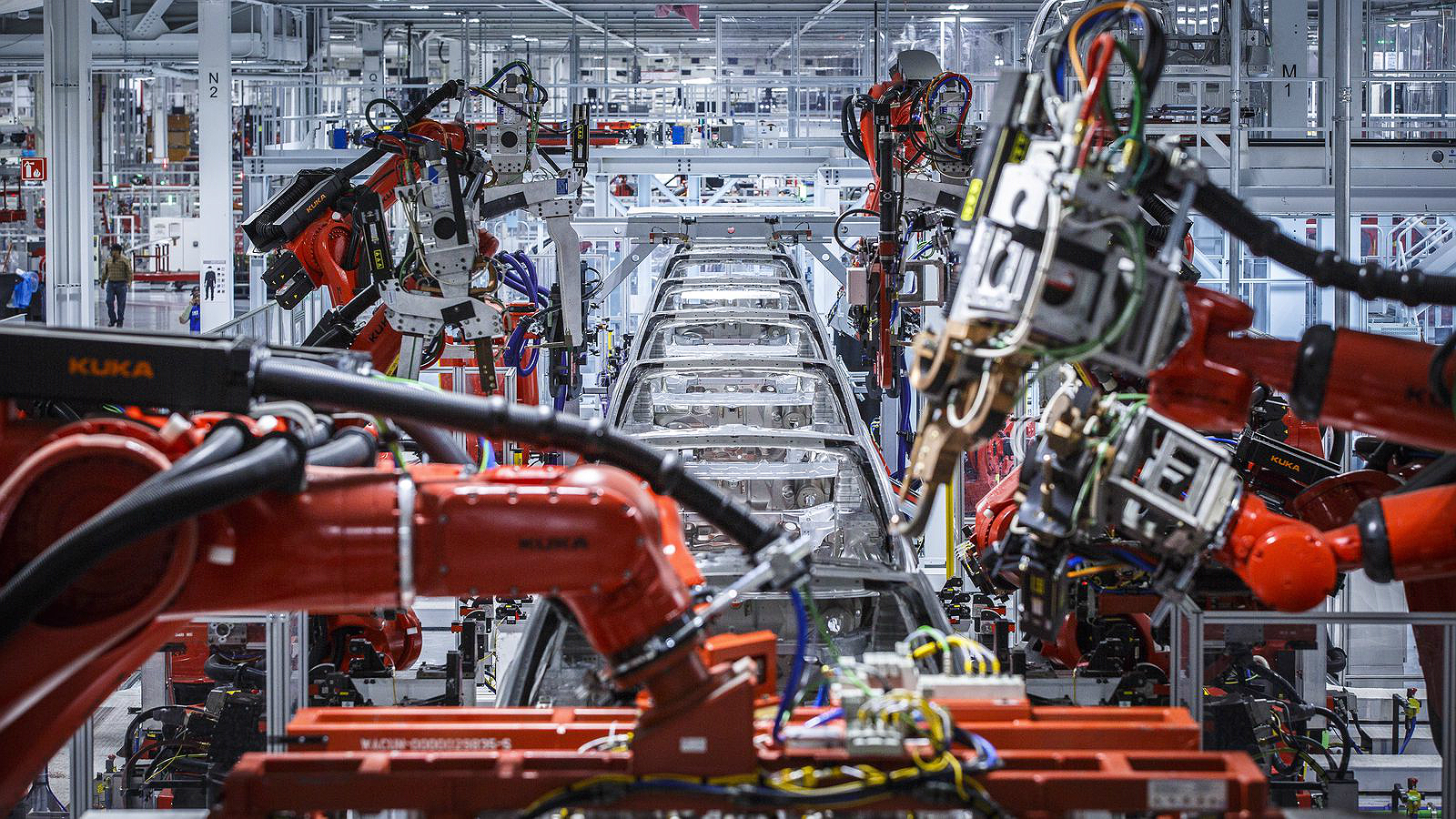

Just days after receiving a higher price target from CFRA and a vote of approval from New Street Research, Tesla (NASDAQ:TSLA) has received yet another round of support from Wall Street. In a recent note to its clients, Jefferies upgraded Tesla from “Hold” to “Buy,” while raising the company’s price target from $360 to $450, representing a 24% gain from the stock’s $363.06 closing price on Thursday.

In a note to clients on Friday, Jefferies analyst Philippe Houchois stated that Tesla’s strengthening balance sheet, its resilient growth relative to the rest of the auto industry, as well as the company’s improving productivity, bodes well for the electric car maker as a whole. Houchois noted that among the carmakers in the industry today, Tesla might be the only one that would avoid a “volume zero-sum game” or “negative margin trade-off in EVs.”

“Tesla should continue to stand out with broader price points, battery security of supply, product edge and a brand that transcends the volume/premium divide. In short, in the year ahead we think only Tesla will avoid a volume zero-sum-game or negative margin trade-off in EVs,” Houchois said.

While Houchois remains optimistic about Tesla’s chances as a self-sustaining business, the Wall Street analyst nevertheless stated that it might be better for Elon Musk to reduce his direct involvement with the company’s day-to-day operations. Instead, the Jefferies analyst noted that Musk should consider focusing on projects such as “product/vision/other ventures.”

“Elon Musk’s erratic behavior makes us wonder if he might be considering reducing his direct involvement in Tesla to focus on product/vision/other ventures. We think such a move might be better suited to Mr. Musk’s talents than driving manufacturing efficiency and would benefit Tesla,” Houchois wrote.

Apart from Jefferies’ upgrade to a “Buy” rating, Tesla also received a higher price target from another Wall Street firm, Wolfe Research. In a recent note, Wolfe analyst Rod Lache gave TSLA an “Outperform” rating while raising the company’s price target from $410 to $430 per share, on account of the electric car maker’s capability to sustain the impressive performance it displayed in the third quarter.

Jefferies Upgrades Tesla to Buy from Hold; Raises PT to $450 from $360$TSLA #Tesla pic.twitter.com/98NO10BERr

— vincent (@vincent13031925) December 7, 2018

-

-

As Wall Street adopts a friendlier stance on Tesla, the company’s shares have proven resilient on the stock market. On Thursday alone, TSLA shares ended at $363.06, even trading as high as $371.25 on Friday’s pre-market. The stock’s price as of Friday’s pre-market places it above a critical milestone, higher than the $359.88 conversion price on $920 million in convertible bonds that are due this coming March. The recent levels of Tesla stock also places it close to levels that were last seen back in August, during the first phases of Elon Musk’s “funding secured” fiasco.

Tesla seems to be preparing itself for yet another delivery and production blitz this December, as the company attempts to deliver as many vehicles as it can to customers in the United States, whose $7,500 federal tax credit is set to expire by the end of the month. Amidst the company’s plans to bring the Model 3 to international markets, as well as its aim of producing the $35,000 base variant of the electric sedan, Tesla’s coming quarters would likely be even more historic.

Disclosure: I have no ownership in shares of TSLA and have no plans to initiate any positions within 72 hours

Elon Musk

Tesla AI boss reveals how big Optimus is going to get

Tesla’s Optimus chief corrected himself on X, confirming a staggering 10 million robot production target.

![Tesla Optimus Gen 3 [Credit: Tesla]](https://www.teslarati.com/wp-content/uploads/2026/03/tesla-optimus-gen3-diner.jpg)

Tesla’s Optimus program has a new number attached to it, after Ashok Elluswamy, the executive who has run the humanoid robot program since June 2025, posted a three word correction on X Thursday, “Correction, 10 million robots.”

The line clarifies the long term annual capacity Tesla is building toward its planned second Optimus production line at Gigafactory Texas, a figure Musk has cited repeatedly since last year’s shareholder meeting.

The scale is worth noting, because ten million robots a year would mean Tesla building more units annually than most countries sell in new cars. Tesla has framed this as a second line, not the first. The buildout is happening in two phases: a roughly one million unit per year line inside Tesla’s Fremont factory, installed on the floor space vacated when Model S and Model X production ended earlier this year, and a much larger dedicated facility under construction at Giga Texas that broke ground on its first steel structure in May. That Texas facility is the one Elluswamy’s correction refers to, and is expected to reach volume production sometime in 2027.

Correction, 10 million robots https://t.co/0z4nyQNTzp

— Ashok Elluswamy (@aelluswamy) July 30, 2026

Tesla Optimus project fires up as Musk sees production line progress

Elluswamy took over Optimus from Milan Kovac last summer and has spent the months since talking up the program’s trajectory. Elon Musk has also floated the ten million figure at Tesla’s 2025 shareholder meeting.

-

Ending Model S and Model X production to make room for the first Optimus line was one of the more consequential manufacturing decisions in the company’s recent history, retiring two flagship vehicles in favor of a robot that has yet to enter mass production. Musk has previously estimated per unit production costs at $20,000 to $25,000 once Tesla reaches a million units a year, though he hasn’t said what that cost looks like at ten times the volume.

SpaceX just picked up another $1.6 billion from the Pentagon, with the U.S. Space Force awarding two task orders worth $1.6 billion to fly 18 Falcon 9 missions from Vandenberg Space Force Base in California through the end of 2027. The launches will carry satellites for the Space Based Sensing and Targeting portfolio, a set of programs meant to help the military detect and track airborne threats and relay that information across forces in near real time.

The award falls under National Security Space Launch Phase 3 Lane 1, the Space Force’s faster, commercial style procurement track for missions that do not require the military’s most demanding certification process. It is also the largest single order publicly disclosed under that program so far, and the first task order issued since the Space Force nearly tripled Lane 1’s contract ceiling from $5.6 billion to $17 billion on July 17.

SpaceX to become America’s Military data backbone for missiles, drones, and warfighters

Eric Zarybnisky, the Space Force’s acting portfolio acquisition executive for space access, said the entire process, from identifying the requirement to signing the contract, took about two months, including a month set aside for companies to prepare proposals.

SpaceX is not just launching these satellites. It already holds the contracts to build two of the programs within the same portfolio, $4.16 billion for the Space Based Airborne Moving Target Indicator system and $2.29 billion for the Space Data Network Backbone, which Teslarati covered in May. That means SpaceX is now responsible for both building key pieces of the military’s next generation sensing network and getting them into orbit.

With this latest award, SpaceX’s Pentagon contract total for 2026 alone tops $8 billion, adding to a defense portfolio that already includes the Golden Dome missile defense software group SpaceX joined in April and a string of GPS launches it inherited after ULA’s Vulcan rocket ran into a booster anomaly, which we detailed in March.

Lane 1’s vendor pool technically includes seven companies: SpaceX, ULA, Blue Origin, Rocket Lab, Stoke Space, Impulse Space, and Relativity Space. In practice, SpaceX remains the only provider with the combination of launch cadence, flight proven Falcon 9 hardware, and West Coast infrastructure to support a campaign requiring roughly one Vandenberg launch a month for the next year and a half.

-

Some lawmakers have flagged the growing concentration of national security launches with one company as a risk worth watching. For now, the Space Force keeps backing SpaceX, with it being the company that shows up ready to launch.

SpaceX (NASDAQ: SPCX) got an absolutely crazy price target rating from Raymond James after the company experienced a tough first few weeks following its Initial Public Offering (IPO).

Despite the tumultuous start, SpaceX has plenty of believers, and the company’s massively successful Starship launch last Friday, its 13th test flight of the massive rocket, went so smoothly that Raymond James analysts pushed its price target on the company to roughly 7 times its current trading level.

SpaceX Starship just nailed something it’s never done before

The firm officially put a “Strong Buy” rating and an $800 price target on the stock. It currently trades at around $113. Its all-time high is $225.64, reaching this trading level shortly after shares first went public.

Raymond James’ price target is tied to the firm’s confidence after Starship’s 13th test flight. Analysts at the firm said it was an incremental step that reduces engineering risks, citing the widely successful heat shield test that CEO Elon Musk recently detailed, the smooth deployment of Starlink V3 satellites, and a successful in-space engine relight.

SpaceX also managed to see Starship splash down safely in the Indian Ocean, while the Super Heavy Booster fell down to the Gulf of America with no incidents.

It is interesting to see these launches have such a tremendous impact on the stock and what investors think of it. After SpaceX initially delayed the Starship launch last week, shares fell tremendously. Most probably did not realize that the stand-down is a standard practice, especially if everything is not perfect.

-

The mission was initially aborted due to an issue with Raptor engines. This was resolved, and Starship launched last Friday after another delay on Thursday, which was caused by weather.

Now that analysts have seen what SpaceX launches are capable of and how impressive the feat is, firms are adjusting their price targets accordingly, making it known that they have high expectations for the space exploration company.

Tesla Model Y L’s new features flexed at unveiling event at Diner

Tesla CEO Elon Musk denies ridiculous Gigafactory Shanghai rumor

![Tesla Optimus Gen 3 [Credit: Tesla]](https://www.teslarati.com/wp-content/uploads/2026/03/tesla-optimus-gen3-diner-80x80.jpg)