Investor's Corner

Tesla (TSLA) bull projects massive growth in 2020 even with conservative estimates

This year has been one of Tesla’s most historic yet, with the company’s shares dropping to over two-year lows before recovering and reaching new all-time highs. As 2019 ends with Tesla showing its strength in terms of vehicle production and deliveries, an ardent TSLA bull has stated that the company is on the cusp of even more dramatic growth next year. What’s more, Tesla seems poised for this growth even with conservative estimates.

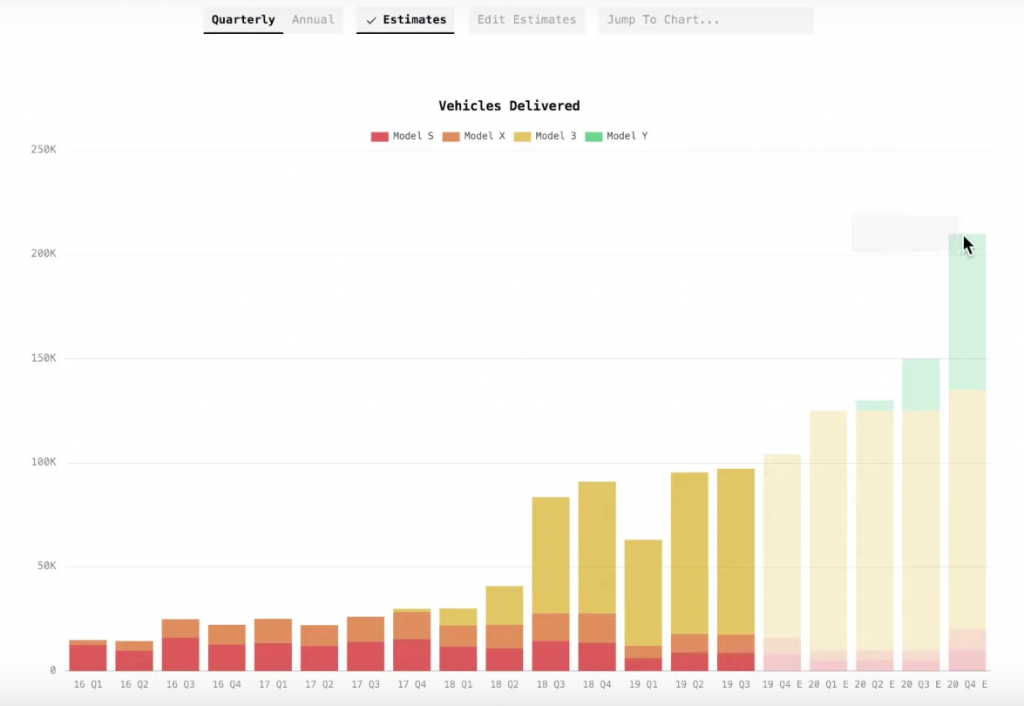

Forecasts from Tesla investor-enthusiast Galileo Russell of YouTube’s Hyperchange channel have always been on the more conservative side. For his 2020 financial projections, the investor adopted the same stance. Despite this, results from the Hyperchange host’s research points to Tesla potentially delivering around 600,000 electric cars in 2020, provided that Model Y production hits its stride at the latter half of the year. That’s around a quarter of a million more than the vehicles Tesla will likely deliver this year.

In a video outlining his thesis, Russell explained that Tesla is now at a point where its core business is seemingly headed towards more stable waters. Cash flow continues to show strength, and the company is sitting on $5 billion in cash. Demand for its vehicles like the Model 3 is validated by sales in the United States, Europe, and China as well, putting the “demand problem” short thesis to rest. Apart from this, Tesla has returned to profitability, and these sentiments are pretty much reflected in the company’s stock, which has broken the $400 per share barrier while hitting all-time-highs.

In a way, Tesla is in a great place to start producing a vehicle that has the potential to carry it higher: the Model Y. The Model Y is a crossover, which means that it is targeted towards one of the auto industry’s most lucrative segments. If the Model 3, a vehicle that competes in a segment that is showing a decline in several regions, can push Tesla so far up, one can only imagine what the Model Y can do to boost the electric car maker further. Tesla, after all, expects the Model Y to outsell the Model S, Model X, and Model 3 combined.

That being said, the TSLA investor expects Tesla Model Y production to be fairly gradual. Russell was optimistic in his projection that a few Model Y can enter production as early as Q1, but he remained conservative for the first half of the year. Overall, the Hyperchange host expects Model Y to hit its stride in the third quarter with a production of about 25,000 units. If Tesla accomplishes this, Russell noted that the crossover’s production could go as high as 75,000 in Q4. This is despite the investor’s prediction that Model S and X sales will drop to their lowest levels as buyers wait for the vehicles’ Plaid variants, and that the Model 3 will see some cannibalization from its crossover sibling.

It should be noted that Russell’s expectations don’t account for several factors that Tesla could still improve, including efficiencies in its vehicle production process and its gross margins. Considering these factors, Tesla may very well remain profitable while allowing the company to pursue other high-profile projects such as the establishment of the Megacharger Network for the Semi, or the buildout of massive projects such as Gigafactory 4 in Europe.

It should also be noted that the Hyperchange host’s models do not account for any additional revenue streams that Tesla can tap into, such as its batteries and powertrains that could be sold to OEMs for their own electric cars. Elon Musk has stated that he is open to such ideas, and Fiat-Chrysler, which already buys credits from Tesla, has expressed interest in tapping into the Silicon Valley-based company’s technology. Considering the lead that Tesla continues to establish in terms of range and efficiency, the idea of a veteran automaker utilizing the company’s batteries and powertrains is more than feasible.

Tesla stock has been on a massive rally lately, and as shares hit a record high, speculations were abounding that the rise was due to shorts covering, or sentiments improving from investors. Russell argues that the recent stock movement for TSLA is also driven, if not primarily, by the steady improvement in Tesla’s fundamentals. Little by little, Tesla is becoming more and more like a full-fledged business, and as it rakes in the profits amidst its growth, the company may very well be headed towards even more milestones in the near future.

Watch the Hyperchange host’s full forecasts for Tesla in 2020 in the video below.

For years, there have been images and videos across social media platforms that have reminded me of when I was a 15-year-old kid teased by “Xbox 720” videos on YouTube. These videos are of the supposed “Tesla Phone” that Elon Musk was secretly developing in between leading Tesla with its electric cars and SpaceX with its reusable rockets.

Would you buy a Tesla phone ? pic.twitter.com/aaTwvvIJit

— Tesla Owners Silicon Valley (@teslaownersSV) October 6, 2023

Although Musk has put those rumors to bed several times, it was never completely out of the realm that he could get involved in cell phones in some capacity. Think outside the box and more macro-level, though. Instead of reinventing the computer, Musk reinvented connectivity by developing Starlink with SpaceX.

It could be something similar, TD Cowen analyst Gregory Williams said in a note last week, where he hinted SpaceX could be gathering some steam to acquire T-Mobile.

Williams said it would be the “clear choice” for SpaceX if it decided to go through with a network acquisition. He also suggested AT&T.

The move would be possible through selling more of its own stock, which would help SpaceX raise the money to purchase T-Mobile, which would cost roughly $300 billion. It could be one of the moves SpaceX makes post-IPO in terms of an acquisition: it already acquired Cursor AI for $60 billion.

Other analysts, like Dan Ives of Wedbush, believe SpaceX and Tesla will eventually merge into one anyway, and that conglomeration could come as soon as this year, some have said.

The implications of SpaceX purchasing T-Mobile are massive. A combined entity would create a truly ubiquitous network: T-Mobile’s terrestrial 5G towers and Starlink’s growing constellation of Direct-to-Cell satellites. This would essentially eliminate dead zones across the U.S. and potentially globally.

SpaceX would instantly become a full-scale facilities-based carrier with satellite differentiation; a huge advantage. This would pressure AT&T and Verizon heavily.

There are also concerns like a potential reduction in long-term competition, and of course, a deal of that size would face intense scrutiny from government agencies.

The strategic fit is compelling due to the existing Starlink–T-Mobile partnership and complementary technologies (space + terrestrial). It could create a dominant integrated communications player. However, the regulatory, financial, and execution hurdles are enormous — this remains highly speculative with no indication SpaceX is actively pursuing it right now.

Elon Musk

SpaceX’s newest Starmind will make earth data centers obsolete

Elon Musk confirmed Starmind as SpaceX’s AI satellite constellation name, targeting one million orbital compute nodes.

Elon Musk confirmed that Starmind will be the official name of SpaceX’s planned AI satellite constellation, following a trademark filing by xAI that surfaced earlier this week. Starmind is what’s being described to the FCC as a constellation of up to one million AI satellites

It’s worth noting that SpaceX’s Starlink communication satellite and Starmind are built on the same orbital infrastructure concept but serve entirely different purposes. Starlink is a connectivity network, with satellites receiving and relaying data between points on Earth, and functioning as a high-speed internet backbone in space. The satellites themselves do not process or think, and move information from one place to another, the same function a fiber cable performs underground.

SpaceX just forced Verizon, AT&T and T-Mobile to team up for the first time in history

Starmind, on the other hand, is something completely different, and tather than moving data, its satellites would compute data through artificial intelligence and directly in orbit using onboard processors powered by large solar arrays. Where a Starlink satellite is essentially a very fast pipe, a Starmind satellite is a server. The practical implication is that Starmind would allow AI models to run inference, process queries, and generate outputs from space, then beam results down to users anywhere on Earth within milliseconds, and without the data ever needing to travel to a terrestrial data center.

Starship will be able to carry 30 to 50 AI1 satellites per launch, delivering the equivalent of dozens of server racks per flight, with no land acquisition, no power grid approval, and no cooling infrastructure required on the ground.

SpaceX is pursuing this new technology as terrestrial data centers are running into hard limits such as lack of physical space, community opposition, and power and water consumption at a scale that is increasingly difficult to permit. Space has unlimited solar power, natural vacuum cooling, and no zoning boards. Musk said in a June 8 video presentation that he expects space to become the lowest-cost location to deploy AI compute within two to three years. Two AI1 prototypes are scheduled to launch in early 2027, with volume production targeted for the end of that year at a new facility called Gigasat.

The real world applications Starmind enables extend well beyond powering Grok. A constellation of orbiting AI processors could run inference workloads for any paying customer, anywhere on Earth, with latency measured in milliseconds rather than the seconds associated with ground-based cloud routing across continents. Starmind, if it scales as described, would make SpaceX the landlord of AI compute the same way Starlink made it the landlord of satellite internet.

SpaceX announced today that it commenced its first-ever public bond offering, marking a significant step in the newly public company’s capital markets strategy.

The company announced an offering of senior unsecured notes expected to raise at least $20 billion.

The move comes just a short time after SpaceX completed one of the largest initial public offerings in history. In mid-June, the company priced shares at $135 and raised more than $85 billion, propelling founder Elon Musk’s net worth past the trillion-dollar mark and giving the firm substantial liquidity.

🚨 SpaceX has announced its inaugural offering of senior unsecured notes.

The net proceeds will be used to repay outstanding loans under its bridge loan facility in full.

This inaugural debt offering represents a financing milestone for SpaceX, which previously depended… pic.twitter.com/pcOZuVbTRv

— TESLARATI (@Teslarati) June 22, 2026

According to the company’s SEC filing, the net proceeds from the notes will be used primarily to repay in full the outstanding borrowings under its existing bridge loan facility, cover related fees and expenses, and fund general corporate purposes. The offering is being conducted under Rule 144A, as well as Regulation S, targeting qualified institutional buyers and non-U.S. investors. Notes will be unsecured obligations ranking equally with other unsubordinated debt.

The $20 billion bridge loan was used to refinance approximately $17.5 billion in higher-cost “junk” debt tied to X and xAI. SpaceX had merged with xAI in February 2026 in an all-stock deal. The bridge facility, which matures in September 2027, had represented the bulk of SpaceX’s long-term debt.

SpaceX officially acquires xAI, merging rockets with AI expertise

In connection with the bond launch, SpaceX disclosed it held approximately $100.8 billion in cash and cash equivalents as of June 19. Investor calls began on the announcement date, with pricing and launch expected shortly thereafter. Rating agencies have assigned investment-grade ratings to the proposed bonds, reflecting confidence in SpaceX’s dominant position in commercial launches and the growth trajectory of its Starlink internet offering.

The debt raise also allows SpaceX to optimize its balance sheet by replacing short-term, higher-cost bridge financing with longer-date, lower-cost fixed-income securities. This provides greater financial flexibility to support capital-intensive initiatives, including the development of Starship, the expansion of the Starlink constellation, and the integration of AI capabilities following the xAI combination.

SpaceX shares (NASDAQ: SPCX) fell sharply on the news, dropping over 16 percent overall on the market on Monday. The stock had surged initially after debuting but pulled back amid profit-taking and broader market dynamics.

Overall, the bond offering underscores SpaceX’s transition to a mature public company with access to diverse funding sources. It positions the firm to pursue its long-term vision of multiplanetary expansion and AI infrastructure, while maintaining a disciplined approach to its capital structure in a high-growth but capital-heavy industry.

Tesla expands massive safety feature worldwide in latest update

Tesla sends production Cybercab with no steering wheel, pedals to on-road testing