Investor's Corner

Tesla investors want Elon Musk to discuss these things at Q3 Earnings

Tesla investors (NASDAQ: TSLA) want CEO Elon Musk to discuss these things on Wednesday as the company will report earnings for the third quarter of 2024.

Fresh off the heels of the “We, Robot” event, where Tesla unveiled the Cybercab, its version of a robotaxi, the Robovan, which could be named something completely different, and used the Optimus bot to serve drinks and entertain, the company will report earnings tomorrow.

Investors and analysts submit questions to Say, an investor relations platform, to ask Musk and other executives.

Here are the five things investors want to know about it:

Tesla $25k affordable model

Tesla has yet to shed any light on whether it will build a $25,000 EV apart from the Cybercab, which Musk said would be priced below $30,000.

Investors and analysts are well aware the vehicle could help Tesla break into an entirely new consumer base and help expand sales and deliveries, which are expected to be level with 2023 levels this year at 1.8 million.

Several of the top questions on Say ask about the $25k model and whether Tesla plans to bring this type of vehicle at this lower price point to market.

Unfortunately, Musk will likely deflect this question as he usually refuses to reveal any prospective vehicle plans on earnings calls.

Tesla Service

It is no secret Tesla Service has been a real bottleneck of the company in recent years, and with more vehicles on the road than ever, more service is needed.

Unfortunately, this is still a pain point for Tesla as it continues to struggle with reasonable wait times for owners, and although it has tried to streamline the process in the past, it has come up remarkably short.

It was not long ago that we reported on some owners complaining of service wait times of nearly two months. Imagine having a car that is in need of service, only to be told it will be two months before you can get an appointment.

Tesla owners complain about extended Service waits of nearly two months

Tesla wanted to streamline service with an F1-style pit-stop approach, but it truly never came to fruition. Although there are more service centers and mobile service vehicles nearly every quarter, Tesla is falling behind on creating an efficient maintenance model for owners.

Tesla Roadster

For years, we’ve been hearing the Tesla Roadster is coming.

This year was no different, as Musk said the vehicle would be unveiled at the end of 2024, but there are no current plans as of now, and there has not even been a hint. Tesla could have unveiled it at We, Robot, and it would have been a huge development.

(Credit: Tesla)

Musk said earlier this year that “most of the engineering” has been completed already, and production would begin next year.

Literally any clarification on whether this is still the plan would be massive for those who are waiting to drop $250,000 on the car.

Tesla Cybertruck AWD Tax Credit

Perhaps one of the most important questions that does not seem to be as important as the aforementioned topics is that of the Cybertruck AWD qualifying for the EV tax credit.

The IRS does not have the Cybertruck as a currently qualifying vehicle, which disqualifies owners who take delivery from the $7,500 credit, which is now available at the point of sale.

Ryan McCaffrey even brought up the issue:

I cannot believe that the #1 question isn’t, “What can you tell us about the individual tax credit eligibility on the Dual Motor Cybertruck? Is the issue with regulatory procedure on the IRS side or is there an element to the truck’s battery cells that disqualifies it?”

— Ryan McCaffrey (@DMC_Ryan) October 22, 2024

Tesla could clear the air significantly here and help bring some more information to owners or even prospective buyers who want to buy the Cybertruck but would like the help from the tax credit.

Tesla will report its earnings tomorrow at market close, 4 p.m. on the East Coast.

Need accessories for your Tesla? Check out the Teslarati Marketplace:

- https://shop.teslarati.com/collections/tesla-cybertruck-accessories

- https://shop.teslarati.com/collections/tesla-model-y-accessories

- https://shop.teslarati.com/collections/tesla-model-3-accessories

Please email me with questions and comments at joey@teslarati.com. I’d love to chat! You can also reach me on Twitter @KlenderJoey, or if you have news tips, you can email us at tips@teslarati.com.

Tesla (NASDAQ: TSLA) is set to hold its Earnings Call for the first quarter of 2026 on Wednesday, and there are a lot of interesting things that are swirling around in terms of speculation from investors.

With the company’s executives, including CEO Elon Musk, answering a handful of questions that investors submit through the Say platform, fans want to know a lot of things about a lot of things.

These five questions come from Retail Investors, who are normal, everyday shareholders:

- When will we have the Optimus v3 reveal? When will Optimus production start, since we ended the Model S and Model X production earlier than mid-year? What’s the expected Optimus production rate exiting this year? What are the initial targeted skills?

- What milestones are you targeting for unsupervised FSD and Robotaxi expansion beyond Austin this year, and how will that drive recurring revenue?

- How will Hardware 3 cars reach Unsupervised Full Self-Driving?

- When do you expect Unsupervised Full Self-Driving to reach customer cars?

- When will Robotaxi expand past its current limited rollout?

Additionally, these are currently the three questions that are slated to be answered by Institutional Firms, which also answer a handful of questions during the call:

- Now that FSD has been approved in the Netherlands and is expected to launch across Europe this summer, can you discuss your Robotaxi strategy for the region?

- What enabled you to finish the AI5 tapeout early and were there any changes to the original vision? Last week, Elon said AI5 will go into Optimus and the Supercomputer, but one month ago said it would go into the Robotaxi. Has AI5 been dropped from the vehicle roadmap?

- Given the recent NHTSA incident filings, can you update us on the Robotaxi safety data? If safety validation remains the primary bottleneck, why not deploy thousands of vehicles to accelerate the removal of the safety driver?

The questions range through every current Tesla project, including FSD expansion and Optimus. However, many of the answers we will get will likely be repetitive answers we’ve heard in the past.

This is especially pertinent when the questions about when Unsupervised FSD will reach customer cars: we know Musk will say that it will happen this year. Is Tesla capable of that? Maybe. But a more transparent answer that is more revealing of a true timeline would be appreciated.

Hardware 3 owners are anxiously awaiting the arrival of FSD v14 Lite, which was promised to them last year for a release sometime this year.

The Earnings Call is set to take place on Wednesday at market close.

Elon Musk

Tesla FSD in Europe vs. US: It’s not what you think

Tesla FSD is approved in the Netherlands, but the European version differs from what US drivers use.

On April 10, 2026, the Dutch vehicle authority RDW granted Tesla the first European type approval for Full Self-Driving Supervised, making the Netherlands the first country on the continent to authorize Tesla’s semi-autonomous system for customer use on public roads.

As Teslarati reported, the RDW approval followed 18 months of testing, more than 1.6 million kilometers driven on EU roads, 13,000 customer ride-alongs, and documentation covering over 400 compliance requirements. Tesla Europe had been running public demo drives through cities like Amsterdam and Eindhoven since early 2026, giving passengers their first experience of the system on European streets.

The European version of FSD is not the same software US drivers use. The RDW’s own statement is direct, noting that the software versions and functionalities in the US and Europe “are therefore not comparable one-to-one.” We’ve compile a table below that captures the most significant differences between US-based Tesla FSD vs. European Tesla FSD that’s based on what regulators and Tesla have publicly confirmed.

| Feature | FSD US | FSD Europe (Netherlands) |

| Regulatory framework | Self-certification, post-market oversight | Pre-market type approval required (UN R-171 + Article 39) |

| Hands requirement | Hands-off permitted on highway | Hands must be available to take over immediately |

| Auto turning from stop lights | Available — navigates intersections, turns, and traffic signals autonomously | Available in EU build — confirmed in Amsterdam demo footage handling unprotected turns and signalized intersections |

| Driving modes | Multiple profiles including a more aggressive “Mad Max” mode | EU build is more conservative by default and errs on the side of restraint when it cannot confirm the limit |

| Summon | Available — Smart Summon navigates parking lots to driver | Status unclear — not confirmed as part of the RDW-approved feature set; urban FSD approval targeted separately for 2027 |

| Driver monitoring | Camera-based eye tracking | Stricter continuous monitoring with more frequent intervention alerts |

| Software version | FSD v14.3 | EU-specific builds that must be separately validated by RDW |

| Geographic restriction | US, Canada, China, Mexico, Australia, NZ, South Korea | Netherlands only; EU-wide vote pending summer 2026 |

| Subscription price | $99/month | €99/month |

| Full urban FSD scope | Available | Partial — separate urban application planned for 2027 |

The approval comes as Tesla is under real pressure to grow FSD subscriptions globally. Musk’s 2025 CEO compensation package, approved by shareholders, includes a milestone requiring 10 million active FSD subscriptions as one condition for his stock awards to vest. Tesla hit one million subscriptions during its Q4 2025 earnings call, which is a meaningful start, but still a long way from the target. Opening Europe as a market for subscriptions, rather than just hardware sales, directly accelerates that number.

Tesla has said it anticipates EU-wide recognition of the Dutch approval during summer 2026, which would extend FSD access to Germany, France, and other major markets through a mutual recognition process without each country repeating the full 18-month review. That timeline is Tesla’s projection, not a confirmed regulatory outcome. As Musk acknowledged at Davos in January 2026, “We hope to get Supervised Full Self-Driving approval in Europe, hopefully next month.”

Elon Musk

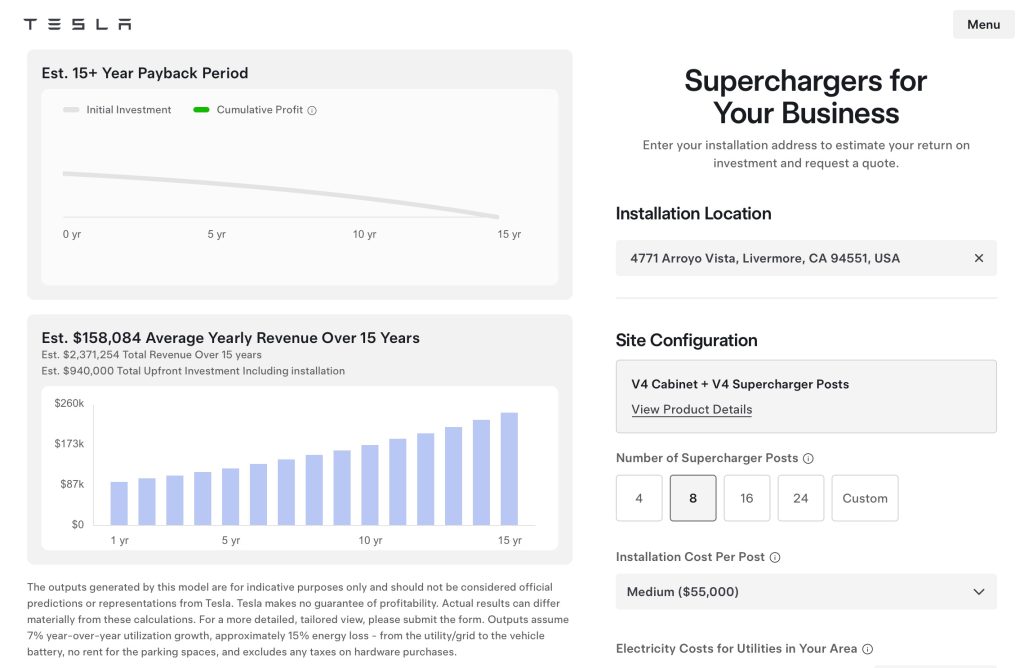

Tesla Supercharger for Business exposes jaw-dropping ROI gap between best and worst locations

Tesla’s new Supercharger for Business calculator reveals an eye-opening all-in cost and location-based ROI projections.

Tesla has launched an online calculator for its Supercharger for Business program, giving property owners their first transparent look at what it really costs to install Superchargers on site and what kind of return they can expect.

The program itself launched in September 2025, allowing businesses to purchase and operate Supercharger hardware on their own property while Tesla handles installation, maintenance, software, and 24/7 driver support. As Teslarati reported at launch, hosts also get their logo placed on the chargers and their location integrated into Tesla’s in-car navigation, meaning drivers are actively routed there. The stalls are open to all EVs, not just Teslas.

We launched Supercharger for Business in 2025 to help companies get charging right. We found simplicity and transparency to be a problem in this industry.

We’re now sharing pricing and a financial calculator to help make informed decisions. The goal is to accelerate investments,…

— Tesla Charging (@TeslaCharging) April 8, 2026

The new online calculator, announced by Tesla on Wednesday with the note that “simplicity and transparency” have been a problem in the industry, lets any business enter a U.S. address and get a real cost and revenue model. A standard 8-stall V4 Supercharger site runs approximately $500,000 in hardware and $55,000 per post for installation, bringing an all-in price just shy of $1 million. Tesla charges a flat $0.10 per kWh fee to cover software, billing, and network operations. Businesses set their own retail price and keep the margin above that fee.

Taking a look at Tesla’s Supercharger for Business online calculator, we can see that ROI is not uniform, and the gap between a strong location and a poor one can stretch the breakeven point by several years.

The biggest driver is foot traffic and how long people stay. A busy rest station, hotel, or outlet mall brings in repeat visitors who need to charge while they’re already stopped, pushing utilization numbers higher and shortening payback time.

Tesla Supercharger for Business ROI calculator

Local electricity rates matter just as much on the cost side. Markets like California carry some of the highest commercial electricity rates in the country, which eats into the margin between what a host pays per kWh and what they charge drivers. At the same time, dense urban areas with high EV adoption tend to support higher retail charging prices, which can offset that cost if demand is strong enough. Weather also plays a role. Cold climates reduce battery efficiency and increase charging frequency, but they can also suppress utilization in winter months if drivers avoid stopping in exposed outdoor locations. Suburban and rural sites face a different problem: lower baseline EV traffic, which means a site with cheaper power and lower operating costs can still take longer to pay back simply because the stalls sit idle more often. Tesla’s calculator uses real fleet data to pre-fill utilization estimates by ZIP code, so businesses can run their specific address against these variables rather than relying on averages.

The program has seen real adoption. Wawa, already the largest host of Tesla Superchargers with over 2,100 stalls across 223 locations, opened its first fully owned and branded site in Alachua, Florida earlier this year. Francis Energy of Oklahoma and the city of Alpharetta, Georgia have also deployed branded stations through the program, as Teslarati covered in January.

Tesla now exceeds 80,000 Supercharger stalls worldwide, and the calculator makes the economic case for accelerating that number through private investment rather than company-owned sites alone.

Tesla Q1 Earnings: What Elon Musk and Co. will answer during the call

Elon Musk reveals shocking Tesla Optimus patent detail