Investor's Corner

Tesla Q2 2018 earnings preview: Layoffs, auto revenue, cost of Model 3 ramp

All eyes will be on Tesla’s pace toward profitability on Wednesday, August 1 when the Silicon Valley company, led by CEO Elon Musk, releases its second quarter financial results after the closing bell. With the electric car maker meeting Musk’s self-imposed Model 3 weekly production target for the second quarter practically by the skin of its teeth, there is a good chance that Q2’s financial results will trigger even more volatility in Tesla’s stock (NASDAQ:TSLA). Here then, is a preview of what we can expect for Tesla’s Q2 2018 financial report and earnings call.

Automotive Deliveries and Revenue Impact

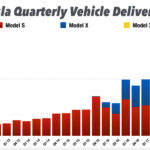

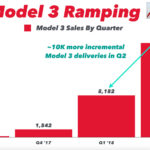

Tesla revealed Q2 deliveries totaling 40,740 vehicles, of which 18,440 were Model 3, 10,930 were Model S, and 11,370 were Model X when it released its production and delivery report earlier this month. Based on the company’s figures, the second quarter results are set to highlight the record deliveries for the Model 3, 10,000 more units compared to Q1. Charts displaying these could be viewed below, courtesy of Galileo Russell of YouTube’s HyperChange TV.

-

- Tesla’s vehicle deliveries. [Credit: Galileo Russell]

-

- Tesla’s Model 3 deliveries. [Credit: Galileo Russell]

Tesla posted revenue of $2.56B in Q1 for vehicle sales, including 8,182 Model 3s that were delivered to customers during the three-month period. Assuming that the additional 10,000 Model 3 delivered in Q2 averaged $55,000 per unit, Tesla could post an additional ~$550 million in earnings from the electric car. Revenue from Tesla’s vehicle leasing business likely remained flat considering that the lending option is not available yet for the Model 3. Service revenue could see a spike in Q2, however, as a result of more Model 3 vehicles being on the road.

The Price of the Model 3 Ramp

Tesla focused largely on the Model 3 ramp during Q2 2018, with the company pulling out all stops to hit its milestone of producing 5,000 Model 3 per week by the end of June. In order to achieve its target production rate, Tesla adopted unorthodox measures such as air-freighting robots and equipment from Europe and setting up an entirely new Model 3 assembly line on the grounds of the Fremont factory. These strategies likely resulted in additional expenses for the company in the second quarter. With the Model 3 ramp as a priority, Tesla’s other sources of income, such as its battery storage and solar business likely remained flat compared to Q1 as a result.

The company’s operational expenditure would likely see a slight bump in the second quarter due to the 9% layoffs that Tesla implemented to organize its workforce, considering that the restructuring included severance pay packages to employees who were terminated. In a video outlining his expectations for Tesla’s Q2 2018 results, the HyperChange TV host noted that he believes Tesla would post an estimated $4B in revenue with losses in the ~$500 million range. That’s a 43% increase in revenue compared to Q2 2017, when Tesla posted earnings of $2.8B, but also double the losses of the company’s losses in 2017’s second quarter.

Looking Past Q2’s Aftermath

Overall, Tesla’s Q2 2018 quarter financial results would likely feature similarities with Q1, in the way that the company would show strong growth but post substantial losses and negative cash flow. Nevertheless, it is pertinent to note that while Q2 2018’s numbers could be discouraging, the quarter could be seen as a turning point for Tesla, especially with regards to its Model 3 ramp. The past quarters, Q2 2018 included, have been focused on bringing the vehicle’s manufacturing up to 5,000 per week, resulting in the company investing heavily in resources to help scale the vehicle’s production.

With the 5,000/week milestone attained and with Tesla now more focused on sustaining its Model 3 production rate, Q3 2018 would most likely feature a pathway to profitability in the form of more encouraging financials than the second quarter. Provided that Tesla adopts a deliberate, realistic plan for the further ramp of the Model 3, the next few quarters could very well prove to be profitable.

Watch Galileo Russell’s take on Tesla’s Q2 2018 financial results in the video below.

Investor's Corner

Tesla gets its latest short from Michael Burry: ‘Happy it jumped back to this level’

Tesla short seller Michael Burry, the subject of the film “The Big Short,” where he was portrayed by Steve Carell, has revealed he has opened a new bet against the stock.

In a new update to his Substack newsletter in a post titled “Trading Post June 30, 2026,” Burry revealed a new set of bets against Tesla, Caterpillar, NVIDIA, Applied Materials Inc., and the iShares Semiconductor ETF.

In regard to Tesla, Burry wrote:

“And finally I shorted Tesla at 416.22. Happy it jumped back to this level.”

This means Burry likely opened his new short position after the company’s recent rally on Wall Street, which saw Tesla shares sink in mid-May, only to recover to well over the $400 mark. Currently, shares trade at around $427.

The company saw a big Tuesday as shares climbed considerably, over 10 percent. The size of the Tesla short was not provided, nor did Burry give any information on the position’s structure, the number of shares, dollar value, or whether options were used in the short.

The Tesla and SpaceX merger everyone is talking about is quietly building

Over the years, Burry has been one of the more vocal critics of Tesla, calling its share price “media inflated,” and saying it was “ridiculously overvalued” as recently as December.

The company has largely transitioned away from being known as an automotive company and instead is much more widely regarded as an AI play, mostly due to its Full Self-Driving efforts, Optimus robot development, and data collection related to both.

This has not pulled those skeptics away from being vocal about their distaste for how Tesla is valued, but there’s no denying that the company is a global force in many things, including sustainable energy, automotive, and AI.

Wedbush Securities is initiating stock coverage on SpaceX (NASDAQ: SPCX), marking the first comments on the company since it went public several weeks ago. Wedbush and its analyst handling coverage, Dan Ives, are widely bullish on fellow Musk company Tesla (NASDAQ: TSLA).

Ives wrote his first note initiating coverage of SpaceX shares on Wednesday with a $190 price target and an ‘Outperform’ rating. The firm believes the company is well positioned off of its IPO because of its wide array of projects, including AI compute power and infrastructure, connectivity projects, and launches.

“We view SpaceX as one of the most differentiated assets within the tech market with a strong footprint across its three core markets, with Starlink driving success with connectivity,” Ives wrote, “Starship launches leading to a demand flywheel and increasing deal flow for its Colossus clusters.”

Elon Musk called it Epic: The full story of SpaceX’s Starship Flight 12

Wedbush leans heavily on Starlink, which they say is the “profitability driver given the strength of its recurring revenue base of ~12 million subscribers as of June 5th.” Ives believes Starlink is still in the “early innings” of penetrating the global telecommunications and broadband market, as it only holds less than a 1 percent share. However, this number is sure to increase over time.

It also highlights the importance of Starship, which it says is an “essential layer” of SpaceX’s overall success. SpaceX developing and displaying the ability to reuse rockets is a major cost and reliability advantage “as it reduces the necessary hardware launch costs while generating a feedback loop for future flights to improve their launch flight rate without accelerating capex spend.”

Finally, SpaceX’s recent AI/Compute projects are also very elementary, Ives writes. It is worth mentioning Wedbush said its $190 price target is derived from a valuation forecast that sees the company yielding roughly $2.48 trillion of implied enterprise value.

There are also some factors that Wedbush did not take into account with its initial coverage. The firm wrote in the note:

“We note that there is optional value coming from Starship’s accelerating scale towards sub-$200/kg unit economics, orbital data centers, and enterprise AI monetization as these factors could drive meaningful upside but these face major hurdles, so we do not take that into account with our valuation.”

SpaceX shares are down just over 2 percent today, trading at around $167 at the time of publication.

For years, there have been images and videos across social media platforms that have reminded me of when I was a 15-year-old kid teased by “Xbox 720” videos on YouTube. These videos are of the supposed “Tesla Phone” that Elon Musk was secretly developing in between leading Tesla with its electric cars and SpaceX with its reusable rockets.

Would you buy a Tesla phone ? pic.twitter.com/aaTwvvIJit

— Tesla Owners Silicon Valley (@teslaownersSV) October 6, 2023

Although Musk has put those rumors to bed several times, it was never completely out of the realm that he could get involved in cell phones in some capacity. Think outside the box and more macro-level, though. Instead of reinventing the computer, Musk reinvented connectivity by developing Starlink with SpaceX.

It could be something similar, TD Cowen analyst Gregory Williams said in a note last week, where he hinted SpaceX could be gathering some steam to acquire T-Mobile.

Williams said it would be the “clear choice” for SpaceX if it decided to go through with a network acquisition. He also suggested AT&T.

The move would be possible through selling more of its own stock, which would help SpaceX raise the money to purchase T-Mobile, which would cost roughly $300 billion. It could be one of the moves SpaceX makes post-IPO in terms of an acquisition: it already acquired Cursor AI for $60 billion.

Other analysts, like Dan Ives of Wedbush, believe SpaceX and Tesla will eventually merge into one anyway, and that conglomeration could come as soon as this year, some have said.

The implications of SpaceX purchasing T-Mobile are massive. A combined entity would create a truly ubiquitous network: T-Mobile’s terrestrial 5G towers and Starlink’s growing constellation of Direct-to-Cell satellites. This would essentially eliminate dead zones across the U.S. and potentially globally.

SpaceX would instantly become a full-scale facilities-based carrier with satellite differentiation; a huge advantage. This would pressure AT&T and Verizon heavily.

There are also concerns like a potential reduction in long-term competition, and of course, a deal of that size would face intense scrutiny from government agencies.

The strategic fit is compelling due to the existing Starlink–T-Mobile partnership and complementary technologies (space + terrestrial). It could create a dominant integrated communications player. However, the regulatory, financial, and execution hurdles are enormous — this remains highly speculative with no indication SpaceX is actively pursuing it right now.

Tesla Optimus project fires up as Musk sees production line progress

Tesla gets its latest short from Michael Burry: ‘Happy it jumped back to this level’