Energy

IER Claims Tesla Powerwall Has 38 Year Payback Time

The Institute for Energy Research reports the payback time for a Tesla PowerWall is 38 years. Tesla disagrees, setting off a war of words.

The Institute for Energy Research (IER) issued a report on January 5 claiming the payback on a Tesla PowerWall is 38 years. The IER is no stranger to those involved in energy policy considerations. The CEO is Robert Bradley, a former director of policy analysis at Enron, where he once wrote speeches for Ken Lay. Lay was the man who many regarded as the person that led the corruption scandal that would ultimately bring down Enron. In a 2003 book, Bradley wrote that carbon dioxide “is not a pollutant but a building block of a living and vibrant biosphere.” That is correct, as far as it goes.

Carbon is indeed a basic building block of all life on Earth. It is flooding the atmosphere with excess carbon that has been trapped in the form of fossil fuels for millions of years that is the problem. Elon Musk made this point with precision when he addressed the Sorbonne in Paris in December. IER is also partially funded by the Koch Brothers reports AutoBlog, citing a story in Mother Jones.

One does not attack Tesla without expecting a vigorous response. The IER report provoked this response from Tesla:

“The report done by the Institute for Energy Research is elementary, at best, and completely misses the value of the Powerwall. For one, IER assumes a fabricated rate structure without citing any source. Transparently, if a consumer were to have a rate structure defined in the article, then the payback calculation is indeed correct.

“However, very few people with this sort of rate structure are interested in Powerwall for financial reasons. They are interested for energy independence, backup security, environmental reasons and tech early adoption, none of which are taken into account.”

Tesla suggested a more accurate way to calculate the payback time for a Powerwall is to focus on regions that have renewable energy policies like feed-in tariffs. That way “the consumer can utilize a Powerwall to consume more of their solar generation and the payback is less than 10 years, while providing the non-economic benefits as well.”

The IER is having none of it, accusing Engadget who first reported on the story of “the most fawning media treatment of any public figure since Pravda covered Stalin.” Which leaves people with a choice — whether to believe a former shill for Ken Lay or the professionally trained engineers who work for Tesla. It shouldn’t be a hard choice to make.

Photo credit: Tesla Motors

In a notable intersection of Big Tech powerhouses, Meta, led by Mark Zuckerberg, has partnered with Canadian energy infrastructure giant Enbridge on a significant renewable energy initiative that will rely on battery technology from Elon Musk’s Tesla.

The project, which was announced this week, marks another step in Meta’s aggressive push to power its expanding data center operations with clean energy, dispelling many of the complaints people have about them.

This new development is located near Cheyenne, Wyoming, and will feature a 365-megawatt (MW) solar farm paired with a 200 MW/1,600 megawatt-hour (MWh) battery energy storage system, also known as BESS. Tesla is providing the batteries for the project, valued at roughly $200 million.

The story was originally reported by Utility Dive.

This Wyoming project represents the first phase of Enbridge and Meta’s joint “Cowboy Project.” Once operational, it will deliver power to Meta’s regional data centers through Cheyenne Light, Fuel, and Power under Wyoming’s Large Power Contract Service tariff.

This tariff, originally developed in collaboration with Microsoft and Black Hills Energy, is designed specifically for large loads like data centers. It ensures that the renewable supply serves hyperscale customers without impacting retail electricity rates for other users.

The battery system will operate under a long-term tolling agreement, providing dispatchable capacity that enhances grid reliability. During periods of high demand, the utility can access the backup generation, addressing one of the key challenges of integrating large-scale renewables with the explosive growth of data center electricity demand driven by artificial intelligence.

This latest collaboration builds on prior joint efforts between Enbridge and Meta in Texas, including the 600 MW Clear Fork Solar, 152 MW Easter Wind, and 300 MW Cone Wind projects. Together with the Wyoming initiative, the companies have now partnered on roughly 1.6 gigawatts (GW) of combined solar, wind, and storage capacity.

The deal highlights the intensifying demand for reliable, low-carbon power from technology giants. Meta has committed to supporting its data center growth with renewable energy, joining peers like Microsoft and Google in seeking large-scale solutions. Enbridge’s Allen Capps described the project as “one of the larger utility-scale battery installations supporting U.S. data center operations and growth.”

The involvement of Tesla’s battery technology adds an intriguing layer, linking two of the world’s most prominent tech leaders—Zuckerberg and Musk—in the clean energy transition.

As data centers continue to drive unprecedented electricity load growth across the United States, projects like this one illustrate how hyperscalers are turning to strategic partnerships with traditional energy players and innovative storage solutions to meet both sustainability goals and reliability needs.

Elon Musk

Why SpaceX just made a $60 billion bet on AI coding ahead of historic IPO

SpaceX has secured an option to acquire Cursor AI for $60 billion ahead of its historic IPO.

SpaceX announced today it has struck a deal with AI coding startup Cursor, securing the option to acquire the company outright for $60 billion later this year, while committing $10 billion for joint development work in the interim. The announcement described the partnership as building “the world’s best coding and knowledge work AI,” and comes just days after Cursor was separately reported to be raising $2 billion at a valuation above $50 billion.

The move makes strategic sense given where each company currently stands. Cursor currently pays retail prices to Anthropic and OpenAI to the same companies competing directly against it with Claude Code and Codex. That means every dollar of revenue Cursor earns partially funds its own competition. With SpaceX bringing computational infrastructure to the Cursor platform, that could reduce Cursor’s dependence on OpenAI and Anthropic’s Claude AI as its providers. Access to SpaceX’s Colossus supercomputer, with compute equivalent to one million Nvidia H100 chips, gives Cursor the infrastructure to run and train its own models at a scale it could never afford independently. That one change restructures the entire unit economics of the business.

Elon Musk teases crazy outlook for xAI against its competitors

Cursor’s $2 billion in annualized revenue and enterprise reach across more than half of Fortune 500 companies gives SpaceX something its xAI subsidiary currently lacks, which is a proven, fast-growing software business with real enterprise distribution.

For Cursor, SpaceX’s $10 billion in joint development funding is transformational. Cursor raised $3.3 billion across all of 2025 to reach that $2 billion in revenue. A single $10 billion commitment from SpaceX, even as a development payment rather than an acquisition, dwarfs everything Cursor has raised in its entire existence. That capital accelerates product development, enterprise sales infrastructure, and proprietary model training simultaneously.

The timing is deliberate. SpaceX filed confidentially with the SEC on April 1, 2026, targeting a June listing at a $1.75 trillion valuation, in what would be the largest public offering in history. The company is expected to begin its roadshow the week of June 8, with Bank of America, Goldman Sachs, JPMorgan, and Morgan Stanley serving as underwriters. Adding Cursor to the portfolio before that roadshow gives IPO investors a concrete enterprise software revenue story to price in, alongside rockets and satellite internet.

The deal also addresses a weakness that became visible after February’s xAI merger. Several xAI co-founders departed following that acquisition, and SpaceX had already hired two Cursor engineers, signaling where its AI talent strategy was heading. Cursor, for its part, faces a pricing disadvantage competing against Anthropic’s Claude Code.

Whether SpaceX exercises the full acquisition option before its IPO or after remains the open question. Either way, this deal reshapes what investors will be buying into when SpaceX goes public.

Elon Musk

Tesla Supercharger for Business exposes jaw-dropping ROI gap between best and worst locations

Tesla’s new Supercharger for Business calculator reveals an eye-opening all-in cost and location-based ROI projections.

Tesla has launched an online calculator for its Supercharger for Business program, giving property owners their first transparent look at what it really costs to install Superchargers on site and what kind of return they can expect.

The program itself launched in September 2025, allowing businesses to purchase and operate Supercharger hardware on their own property while Tesla handles installation, maintenance, software, and 24/7 driver support. As Teslarati reported at launch, hosts also get their logo placed on the chargers and their location integrated into Tesla’s in-car navigation, meaning drivers are actively routed there. The stalls are open to all EVs, not just Teslas.

We launched Supercharger for Business in 2025 to help companies get charging right. We found simplicity and transparency to be a problem in this industry.

We’re now sharing pricing and a financial calculator to help make informed decisions. The goal is to accelerate investments,…

— Tesla Charging (@TeslaCharging) April 8, 2026

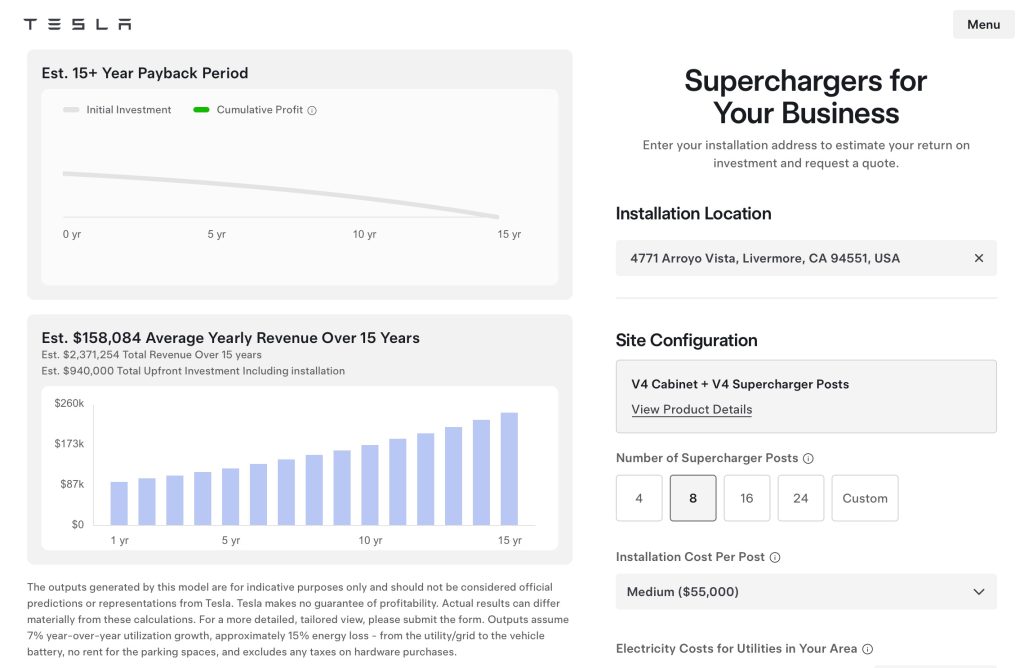

The new online calculator, announced by Tesla on Wednesday with the note that “simplicity and transparency” have been a problem in the industry, lets any business enter a U.S. address and get a real cost and revenue model. A standard 8-stall V4 Supercharger site runs approximately $500,000 in hardware and $55,000 per post for installation, bringing an all-in price just shy of $1 million. Tesla charges a flat $0.10 per kWh fee to cover software, billing, and network operations. Businesses set their own retail price and keep the margin above that fee.

Taking a look at Tesla’s Supercharger for Business online calculator, we can see that ROI is not uniform, and the gap between a strong location and a poor one can stretch the breakeven point by several years.

The biggest driver is foot traffic and how long people stay. A busy rest station, hotel, or outlet mall brings in repeat visitors who need to charge while they’re already stopped, pushing utilization numbers higher and shortening payback time.

Tesla Supercharger for Business ROI calculator

Local electricity rates matter just as much on the cost side. Markets like California carry some of the highest commercial electricity rates in the country, which eats into the margin between what a host pays per kWh and what they charge drivers. At the same time, dense urban areas with high EV adoption tend to support higher retail charging prices, which can offset that cost if demand is strong enough. Weather also plays a role. Cold climates reduce battery efficiency and increase charging frequency, but they can also suppress utilization in winter months if drivers avoid stopping in exposed outdoor locations. Suburban and rural sites face a different problem: lower baseline EV traffic, which means a site with cheaper power and lower operating costs can still take longer to pay back simply because the stalls sit idle more often. Tesla’s calculator uses real fleet data to pre-fill utilization estimates by ZIP code, so businesses can run their specific address against these variables rather than relying on averages.

The program has seen real adoption. Wawa, already the largest host of Tesla Superchargers with over 2,100 stalls across 223 locations, opened its first fully owned and branded site in Alachua, Florida earlier this year. Francis Energy of Oklahoma and the city of Alpharetta, Georgia have also deployed branded stations through the program, as Teslarati covered in January.

Tesla now exceeds 80,000 Supercharger stalls worldwide, and the calculator makes the economic case for accelerating that number through private investment rather than company-owned sites alone.

Tesla Full Self-Driving is taking over Europe: fourth country gets FSD approval

Tesla revises FSD transfer policy on new Cybertruck trim, causing cancellations