News

Tesla, SpaceX, Elon Musk ventures cleared by SEC for private fundraising after tweet controversy

Tesla, SpaceX, The Boring Company (TBC), and Neuralink have all been granted waivers allowing them to continue raising capital by privately selling restricted securities (typically private equity or debt), heading off potential barriers that would increase the difficulty of raising capital through the sale of securities.

Cued by the commission’s settled suit over CEO Elon Musk’s improper and misleading dissemination of information material to Tesla shareholders, the United States Securities and Exchange Commission (SEC) has granted investment disqualification waivers – specifically “waivers of disqualification under Rule 506 of Regulation D” – to each of the four major companies owned by Elon Musk.

-

- Building giant factories like Gigafactory 2 demands major capital investments that often require private equity sales. (Tesla)

-

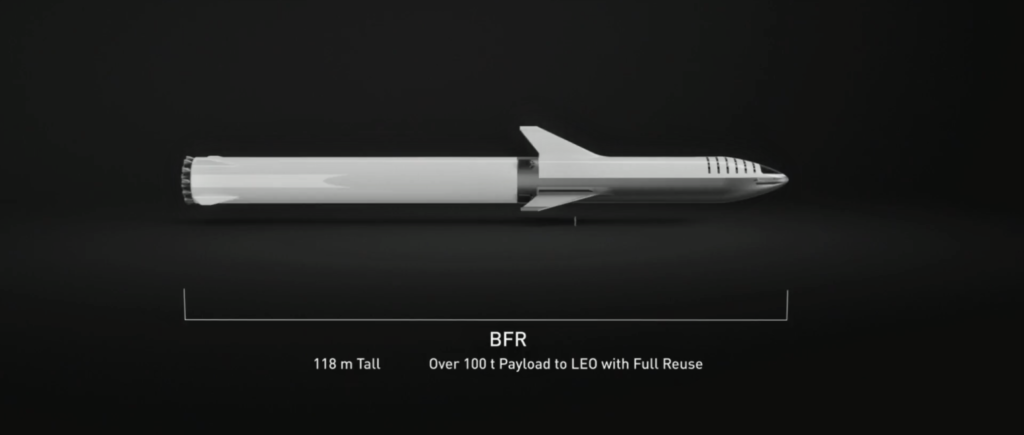

- Rockets are perhaps even more capital intensive. (SpaceX)

Losing the ability to raise funds in this manner would make it much harder for companies like Tesla and SpaceX to raise the money frequently needed for expansions and major R&D projects, described in the waiver requests as “extremely capital intensive.” However, the bulk of the arguments provided by each company’s legal representatives can be largely ignored. Arguing to the contrary – i.e. failing to make a strong case that the given company may need private equity investment – could close critical doors that each company may not need right this moment but would like to preserve as an option.

Still, each waiver request offers a slight glimpse into the inner-workings of SpaceX, TBC, and Neuralink, typically hidden from the public eye as privately held entities.

Tesla

Tesla, being a publicly-traded company, offered few secrets in its waiver request. However, it did publicize the best overview yet of what exactly the SEC’s demand for the regulation of Elon Musk’s Tesla-material communications might translate to inside the company. According to Tesla’s legal representatives, the company is arranging the creation of “new, permanent committee…of independent directors only [that] will provide an additional check on the procedures and processes for overseeing Mr. Musk’s Tesla-related public statements.” Tesla will also reportedly task “another experienced securities lawyer…to undertake an enhanced review of communications made through Twitter and other social media by the [sic] Tesla’s senior officers.”

The hope is that this new arrangement will prevent a recurrence of the misconduct that led to the SEC’s suit and the subsequent settlement. More likely, however, is that the threat of the modification or withdrawal of these four waivers will prevent Musk from stepping outside the bounds of the SEC’s binding settlement agreement, as doing so could truly harm the potential of all four companies.

SpaceX

In SpaceX’s waiver request, the company’s legal representatives confirmed that it has raised “more than $2 billion in [eleven separate] securities offerings” that fell under the purview of activities SpaceX would be disqualified from pursuing without a waiver from the SEC. The total value of investments on the public record currently hovers around $2.27 billion, including a partially-finished Series I round that has likely raised that to value to ~$2.5 billion since it surfaced in April 2018.

“The design and manufacture of launch vehicles and spacecraft is extremely capital intensive. SpaceX needs sufficient [and may need to raise additional] capital to fund its ongoing operations and future expansions, for example: development of its BFR launch vehicle and Crew Dragon spacecraft, continuing research and development projects, and making investments in tooling and manufacturing”

The Boring Company & Neuralink

As for TBC and Neuralink, the waivers didn’t offer anything unexpected, although they did provide great, brief overviews of what exactly the two companies are currently working towards. Although it was announced in late 2017 that Musk would sell stock to fund initial operations at TBC and Neuralink, both companies’ legal representatives confirmed the exact amount of funding raised by “Musk and various other third-party investors”: $112.5 million and $100.2 million, respectively.

Both expressly confirmed no intentions to pursue initial public offerings (IPOs) anytime soon, although Neuralink’s waiver indicated that it may invest in or acquire other companies pursuing brain-computer interfaces.

-

- Musk believes that TBC will finish its first test-tunnel in roughly six weeks, in early December. (TBC)

-

- The Boring Company’s next-gen tunnel-boring machine seen in its early stages, October 5th. [Credit: Tom Cross/Teslarati]

-

- While we have no clue what Neuralink’s stealthed work has produced, it’s perhaps the most long-term venture Musk has started. The path to market for medical devices is very long and even more expensive.

The Boring Company

“The Boring Company (TBC) is a fast-growing infrastructure and transportation company focused on developing cost effective, and fast tunneling technology, along with electric mass transportation systems to alleviate the massive problem of traffic and congestion within cities. The research, development, design, manufacture, testing, and construction of tunnels and mass transit systems is a capital intensive business. TBC needs sufficient capital to fund its ongoing operations and future expansions, for example: continued development and improvement of Tunnel Boring Machines (“TBMs”) and electric skates, the construction of mass transit tunnels including publicly announced projects in Chicago, Los Angeles, and Washington D.C..”

Neuralink

“Neuralink is a fast-growing bio-technology and medical device company focused on developing high bandwidth, long term, brain computer interfaces (“BCI”). The research, development, design, manufacture, testing, and certification of medical devices and BCI’s is purely capital intensive business requiting deep investment for years prior to any initial revenue. Neuralink needs sufficient capital to fund its ongoing operations and eventually bringing products to marked, for example: continued development of BCI’s, continued testing of implantable devices, financing of multi-year FDA trials and certifications, and the construction of FDA-approved manufacturing facilities. Neuralink will need to raise capital for these operations and expansions, and given the development stage of the company, it is most likely that such financing will be through private securities offerings in reliance on Rule 506 of Regulation D.”

Elon Musk

Why Tesla’s Q3 could be one of its biggest quarters in history

Tesla could stand to benefit from the removal of the $7,500 EV tax credit at the end of Q3.

Tesla has gotten off to a slow start in 2025, as the first half of the year has not been one to remember from a delivery perspective.

However, Q3 could end up being one of the best the company has had in history, with the United States potentially being a major contributor to what might reverse a slow start to the year.

Earlier today, the United States’ House of Representatives officially passed President Trump’s “Big Beautiful Bill,” after it made its way through the Senate earlier this week. The bill will head to President Trump, as he looks to sign it before his July 4 deadline.

The Bill will effectively bring closure to the $7,500 EV tax credit, which will end on September 30, 2025. This means, over the next three months in the United States, those who are looking to buy an EV will have their last chance to take advantage of the credit. EVs will then be, for most people, $7,500 more expensive, in essence.

The tax credit is available to any single filer who makes under $150,000 per year, $225,000 a year to a head of household, and $300,000 to couples filing jointly.

Ending the tax credit was expected with the Trump administration, as his policies have leaned significantly toward reliance on fossil fuels, ending what he calls an “EV mandate.” He has used this phrase several times in disagreements with Tesla CEO Elon Musk.

Nevertheless, those who have been on the fence about buying a Tesla, or any EV, for that matter, will have some decisions to make in the next three months. While all companies will stand to benefit from this time crunch, Tesla could be the true winner because of its sheer volume.

If things are done correctly, meaning if Tesla can also offer incentives like 0% APR, special pricing on leasing or financing, or other advantages (like free Red, White, and Blue for a short period of time in celebration of Independence Day), it could see some real volume in sales this quarter.

You can now buy a Tesla in Red, White, and Blue for free until July 14 https://t.co/iAwhaRFOH0

— TESLARATI (@Teslarati) July 3, 2025

Tesla is just a shade under 721,000 deliveries for the year, so it’s on pace for roughly 1.4 million for 2025. This would be a decrease from the 1.8 million cars it delivered in each of the last two years. Traditionally, the second half of the year has produced Tesla’s strongest quarters. Its top three quarters in terms of deliveries are Q4 2024 with 495,570 vehicles, Q4 2023 with 484,507 vehicles, and Q3 2024 with 462,890 vehicles.

Elon Musk

Tesla Full Self-Driving testing continues European expansion: here’s where

Tesla has launched Full Self-Driving testing in a fifth European country ahead of its launch.

Tesla Full Self-Driving is being tested in several countries across Europe as the company prepares to launch its driver assistance suite on the continent.

The company is still working through the regulatory hurdles with the European Union. They are plentiful and difficult to navigate, but Tesla is still making progress as its testing of FSD continues to expand.

Today, it officially began testing in a new country, as more regions open their doors to Tesla. Many owners and potential customers in Europe are awaiting its launch.

On Thursday, Tesla officially confirmed that Full Self-Driving testing is underway in Spain, as the company shared an extensive video of a trip through the streets of Madrid:

Como pez en el agua …

FSD Supervised testing in Madrid, Spain

Pending regulatory approval pic.twitter.com/txTgoWseuA

— Tesla Europe & Middle East (@teslaeurope) July 3, 2025

The launch of Full Self-Driving testing in Spain marks the fifth country in which Tesla has started assessing the suite’s performance in the European market.

Across the past several months, Tesla has been expanding the scope of countries where Full Self-Driving is being tested. It has already made it to Italy, France, the Netherlands, and Germany previously.

Tesla has already filed applications to have Full Self-Driving (Supervised) launched across the European Union, but CEO Elon Musk has indicated that this particular step has been the delay in the official launch of the suite thus far.

In mid-June, Musk revealed the frustrations Tesla has felt during its efforts to launch its Full Self-Driving (Supervised) suite in Europe, stating that the holdup can be attributed to authorities in various countries, as well as the EU as a whole:

Tesla Full Self-Driving’s European launch frustrations revealed by Elon Musk

“Waiting for Dutch authorities and then the EU to approve. Very frustrating and hurts the safety of people in Europe, as driving with advanced Autopilot on results in four times fewer injuries! Please ask your governing authorities to accelerate making Tesla safer in Europe.”

Waiting for Dutch authorities and then the EU to approve.

Very frustrating and hurts the safety of people in Europe, as driving with advanced Autopilot on results in four times fewer injuries!

Please ask your governing authorities to accelerate making Tesla safer in Europe. https://t.co/QIYCXhhaQp

— Elon Musk (@elonmusk) June 11, 2025

Tesla said last year that it planned to launch Full Self-Driving in Europe in 2025.

Elon Musk

xAI’s Memphis data center receives air permit despite community criticism

xAI welcomed the development in a post on its official xAI Memphis account on X.

Elon Musk’s artificial intelligence startup xAI has secured an air permit from Memphis health officials for its data center project, despite critics’ opposition and pending legal action. The Shelby County Health Department approved the permit this week, allowing xAI to operate 15 mobile gas turbines at its facility.

Air permit granted

The air permit comes after months of protests from Memphis residents and environmental justice advocates, who alleged that xAI violated the Clean Air Act by operating gas turbines without prior approval, as per a report from WIRED.

The Southern Environmental Law Center (SELC) and the NAACP has claimed that xAI installed dozens of gas turbines at its new data campus without acquiring the mandatory Prevention of Significant Deterioration (PSD) permit required for large-scale emission sources.

Local officials previously stated the turbines were considered “temporary” and thus not subject to stricter permitting. xAI applied for an air permit in January 2025, and in June, Memphis Mayor Paul Young acknowledged that the company was operating 21 turbines. SELC, however, has claimed that aerial footage shows the number may be as high as 35.

Critics are not giving up

Civil rights groups have stated that they intend to move forward with legal action. “xAI’s decision to install and operate dozens of polluting gas turbines without any permits or public oversight is a clear violation of the Clean Air Act,” said Patrick Anderson, senior attorney at SELC.

“Over the last year, these turbines have pumped out pollution that threatens the health of Memphis families. This notice paves the way for a lawsuit that can hold xAI accountable for its unlawful refusal to get permits for its gas turbines,” he added.

Sharon Wilson, a certified optical gas imaging thermographer, also described the emissions cloud in Memphis as notable. “I expected to see the typical power plant type of pollution that I see. What I saw was way worse than what I expected,” she said.

Why Tesla’s Q3 could be one of its biggest quarters in history

Tesla Full Self-Driving testing continues European expansion: here’s where

xAI’s Memphis data center receives air permit despite community criticism

-

Elon Musk3 days ago

Elon Musk3 days agoTesla investors will be shocked by Jim Cramer’s latest assessment

-

News1 week ago

News1 week agoTesla Robotaxi’s biggest challenge seems to be this one thing

-

News2 weeks ago

News2 weeks agoTexas lawmakers urge Tesla to delay Austin robotaxi launch to September

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoFirst Look at Tesla’s Robotaxi App: features, design, and more

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoxAI’s Grok 3 partners with Oracle Cloud for corporate AI innovation

-

News2 weeks ago

News2 weeks agoSpaceX and Elon Musk share insights on Starship Ship 36’s RUD

-

News2 weeks ago

News2 weeks agoWatch Tesla’s first driverless public Robotaxi rides in Texas

-

News2 weeks ago

News2 weeks agoTesla has started rolling out initial round of Robotaxi invites