Tesla has made price cuts across its entire lineup this year, effectively waging a “price war” against other automakers. According to new registration data in the U.S., the strategy seems to have boosted overall electric vehicle (EV) sales, with Tesla remaining the dominant market share leader.

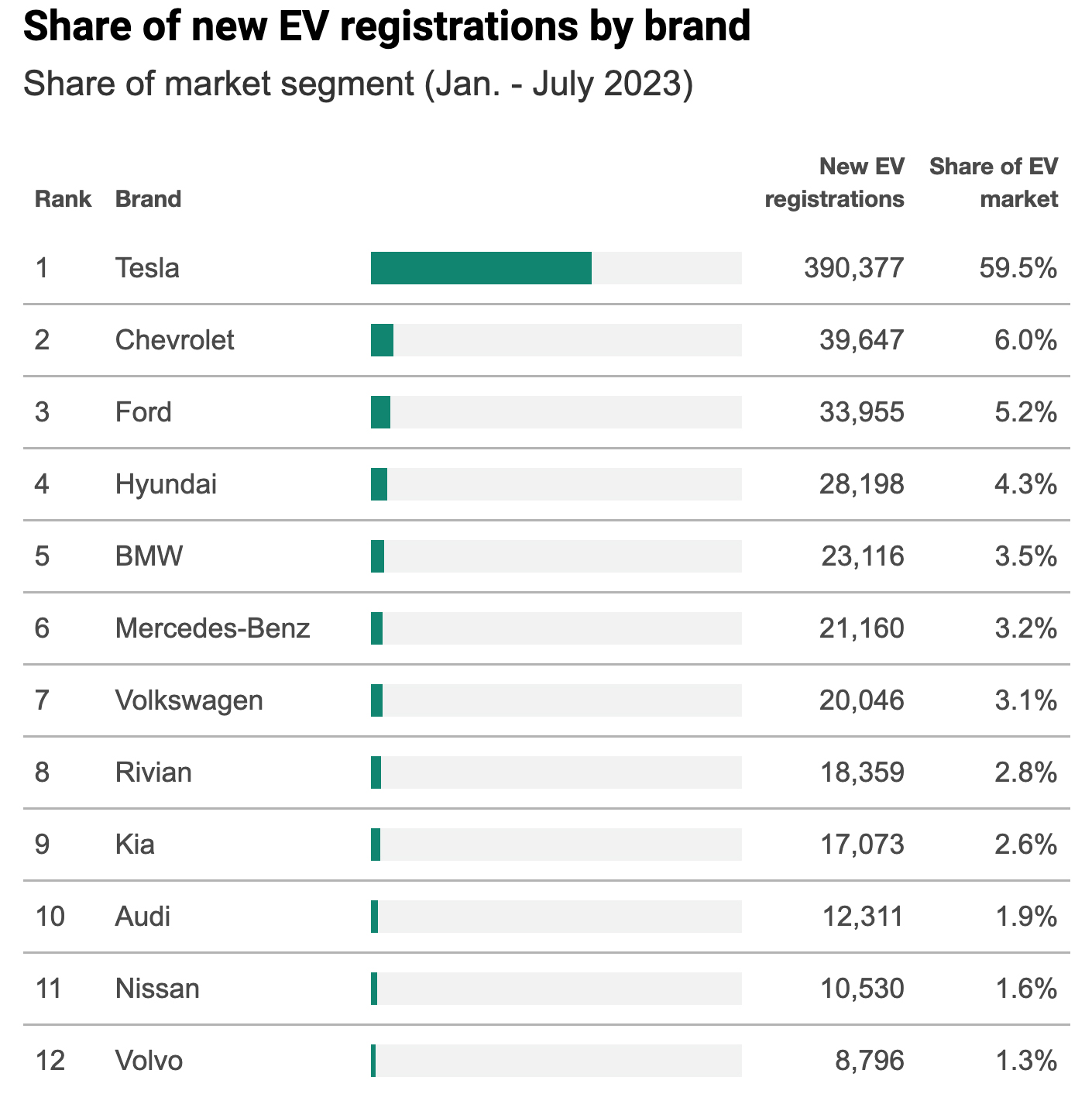

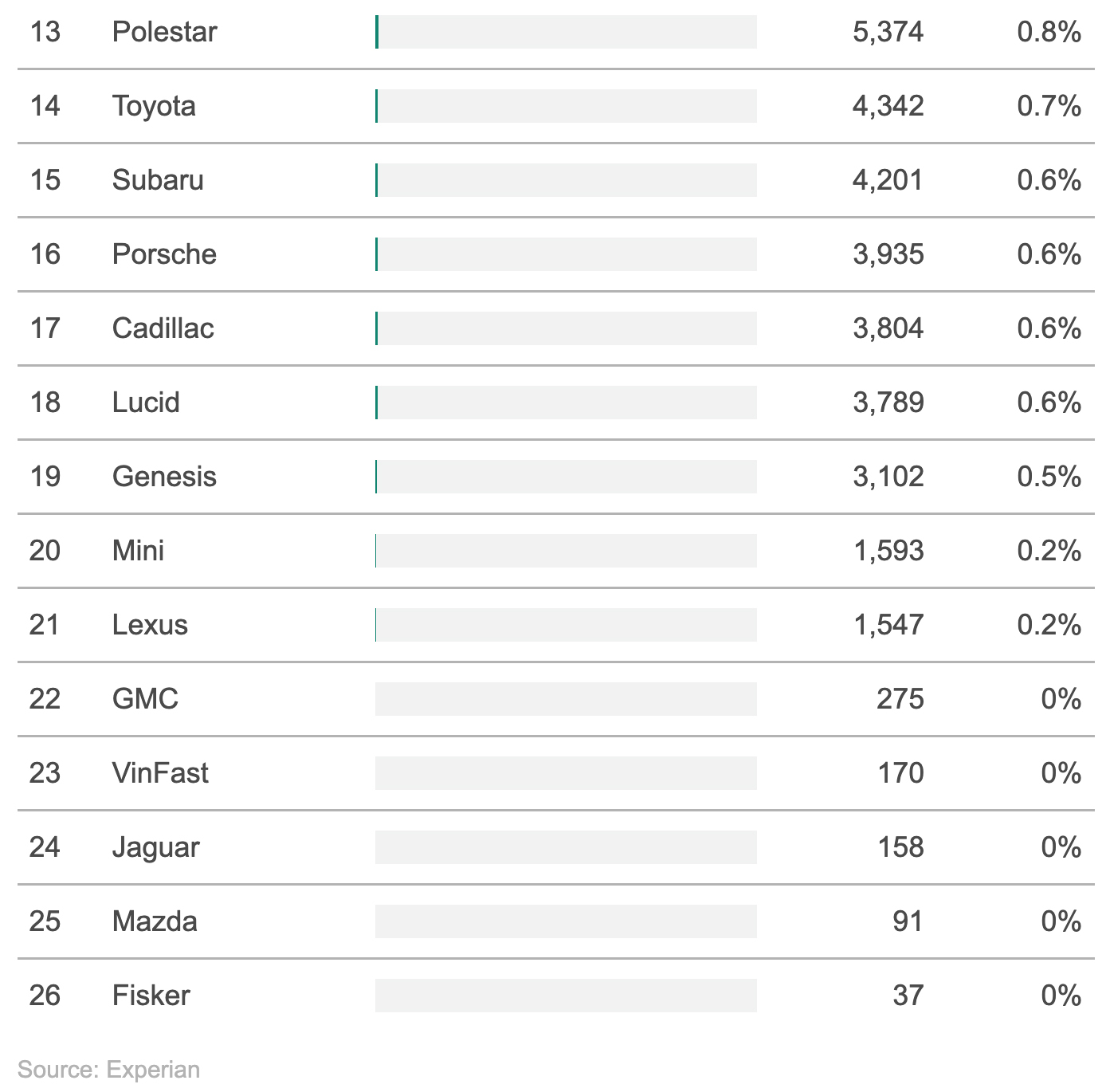

As shown in new registration data from Experian, the auto market share of EVs has risen to 7.2 percent this year in the period from January to July, with overall EV registrations jumping to 655,986 total for a 67 percent year-over-year increase (via Automotive News). During the same period, Tesla had 390,377 vehicles registered for a 50-percent jump from 2022, capturing a 59.5-percent share of the EV market.

Following Tesla’s registrations were offerings from Chevrolet (39,647), Ford (33,955), Hyundai (28,198) and BMW (23,116) to make up the rest of the top five registered EV brands in the U.S. Notable EVs sold by Chevy and Ford included the Chevy Bolt EV and Bolt EUV, the brand-new Silverado, the Ford Mustang Mach-E and the F-150 Lightning.

Credit: Automotive News Credit: Automotive News

The data shows that Model Y registrations reached 236,041 in the seven months, more than double those of last year. Tesla had 131,381 registrations of the Model 3 in the period ending July, ahead of its launch of the forthcoming Highland Model 3. The Model S saw registration figures drop by 51 percent during the same period, landing at just 8,493, while the Model X fell 14 percent to 14,462 registered units.

Tesla cut prices on its vehicles in January, forcing some other automakers to follow suit. J.D. Power guessed that the overall EV market share had jumped to 8.5 percent in July, pointing to Tesla’s price cuts as a major catalyst in making EVs more affordable.

In one index, the organization also compares EVs to gas cars, rating them on a scale of 100 points. J.D. Power VP of EV practice Elizabeth Krear pointed out the price cuts from Tesla as a driver of increased market share in one analysis of the index last month.

“Affordability remains the highest-scoring factor at 97, driven by aggressive pricing from Tesla,” Krear said. “Although the affordability factor is approaching parity, it is skewed by the premium market, driven largely by Tesla’s 63 percent EV market share.”

It’s worth noting that Tesla doesn’t disclose global sales by region or country, so the Experian data is more of an estimate of sales than anything. In addition, many automakers do not report EV sales separately from their gas cars, and some don’t share their monthly sales.

-

-

What are your thoughts? Let me know at zach@teslarati.com, find me on X at @zacharyvisconti, or send your tips to us at tips@teslarati.com.

Elon Musk

Another Tesla SpaceX merger prediction by ARK Invest has Elon Musk talking

Elon Musk again denies a Tesla China split as new SpaceX merger speculation resurfaces quickly.

Elon Musk restated that Tesla has no plans to separate its China business from the rest of the company, responding to a new round of merger speculation from ARK Invest.

On the firm’s “Brainstorm” podcast, Cathie Wood’s team, including chief futurist Brett Winton and research director Nick Grous, argued a Tesla and SpaceX combination remains likely, with an announcement possible before the end of the year even if the deal itself would not close that quickly. Winton called Tesla’s Shanghai operations a “small ish wrinkle” for a merger rather than a real obstacle, since SpaceX’s national security work with the U.S. government sits uneasily next to Tesla’s manufacturing base in China.

Musk pushed back on the framing directly. “China is awesome. I strongly encourage people to visit,” he wrote on X. He also repeated language he first used in late July, when the Wall Street Journal reported that Tesla executives had been told to prepare for a possible spinoff, sale, or closure of the China business ahead of a SpaceX tie up. Musk called that report “absurdly fake news” at the time, adding that a separation had “never even come up in a discussion ever,” a line he echoed again this week.

The repeated denial has not settled the underlying question, because Shanghai’s role in Tesla’s business is exactly what makes a merger complicated. Gigafactory Shanghai still ships more than half of Tesla’s global deliveries and functions as the company’s main export hub for Europe and Asia. Teslarati previously reported on Musk’s initial denial, and the merger conversation itself has been building since SpaceX’s IPO gave it public shares to use as acquisition currency.

Wedbush’s Dan Ives has pegged the odds of a Tesla SpaceX merger at 80 to 90 percent by early 2027, and ARK’s prediction of a year end announcement adds another data point to that timeline, even as Musk keeps rejecting the specific mechanics reporters have described. Neither position rules out the other. Musk can deny a China spinoff was ever discussed while analysts still expect some form of combination to move forward, since ARK and Ives are both describing convergence at the corporate level, not necessarily the internal restructuring the Journal described in July.

For now, Tesla’s China business remains intact, and Musk’s comments this week make clear he has no interest in publicly walking that position back, no matter how often the merger question resurfaces.

-

Elon Musk

The real reason Elon Musk wants every car connected to space

Elon Musk says all cars will eventually need Starlink to handle massive AI bandwidth demand.

Elon Musk is making the case that satellite internet, not fiber or cellular towers, will end up wired into every car on the road. In a string of posts on X, the SpaceX CEO wrote that all cars will have Starlink in the future and called satellite connectivity the only way to get super high bandwidth to billions of vehicles.

The posts started with Musk endorsing a Cloudflare forecast that traffic generated by autonomous AI agents will soon dwarf traffic generated by humans browsing the internet, a shift he described as not a close call at all. From there he narrowed the argument to infrastructure, writing that the only system that can support the insanely fast bandwidth growth needed by AI is Starlink, before extending the logic to cars specifically.

AI agentic Internet traffic will obviously VASTLY exceed human usage. Not a close call at all.

Cloudflare’s forecast is accurate. https://t.co/VztgrinN5k pic.twitter.com/Wo4FiRKjPU

— Elon Musk (@elonmusk) August 9, 2026

The timing lines up with Tesla’s own hardware decisions. On July 20, Tesla confirmed the Cybercab would ship with a Starlink V5 terminal built into its roof, the first time the company had put satellite hardware in a production vehicle. A day later, Tesla’s head of AI, Ashok Elluswamy, explained the connection wasn’t there for safety and that Cybercab’s driving stack runs entirely on onboard cameras and compute, while the satellite link exists for navigation, customer service, and fleet management instead. Musk followed with his own post about the feature, saying riders would be able to watch 4K streaming video during rides.

By July 22, Musk had already said Starlink would extend beyond Cybercab to Tesla’s full lineup. Sunday’s posts push that same logic outward again, this time framed as a requirement across the industry rather than a feature specific to Tesla, and tied directly to the bandwidth AI systems are expected to consume.

SpaceX’s newest Starmind will make earth data centers obsolete

-

The AI argument has been building on SpaceX’s side for months. The company has an FCC filing pending for a third generation Starlink constellation, and it has separately proposed Starmind, a constellation of up to a million satellites designed to run AI computation directly in orbit rather than just relay data. Musk has said he expects space to become the cheapest place to deploy AI compute within two to three years. Starlink and Starmind serve different jobs inside that vision, one moving data and the other processing it, but Sunday’s posts treat vehicles as one more category of hardware that will eventually need both.

None of this changes anything for Tesla owners today. Cars already on the road keep running on LTE and Wi-Fi, and Tesla hasn’t outlined a retrofit path for existing vehicles. The July 22 commitment applies to future production, not the fleet already delivered. What Musk added on Sunday is the reasoning: satellite connectivity isn’t a Cybercab novelty, it’s a bet that ground based networks won’t keep up with how much data cars, robots, and AI systems are about to generate.

Elon Musk

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it

The Boring Company’s new tunnel vehicle runs on Tesla Model 3 batteries and drive units.

The Boring Company just introduced a new piece of hardware, and it runs on parts pulled straight from a Tesla showroom. Liner Truck 3, unveiled in a post from the tunneling company’s official X account, is an all electric vehicle built around Tesla Model 3 battery packs and drive units, purpose built to move concrete tunnel segments to the boring machine face without a single person underground.

Introducing Liner Truck 3 — our latest fully electric tunnel vehicle.

– Tesla Model 3 battery and drive units

– Transports 22,000+ lb of concrete segments to the boring machine

– 28 miles of range

– 12 mph max operating speed

– Remotely piloted from Global OCC in Texas, with… pic.twitter.com/XB7FgSXnpy— The Boring Company (@boringcompany) August 7, 2026

The job itself is unglamorous but critical. Each precast segment run weighs more than 22,000 pounds, roughly the load of a full cement mixer, and Liner Truck 3 hauls that weight repeatedly between the surface staging area and wherever the Prufrock machine happens to be cutting.

The Boring Company said Liner Truck 3 is piloted remotely out of its Global Operations Control Center in Texas, extending the Zero-People-In-Tunnel approach the company has spent years building toward. An earlier version of a ZPIT liner truck was already tested at the company’s Bastrop, Texas research tunnels, and a factory tour released last month showed an employee flying a fully loaded liner truck with a PlayStation controller. Liner Truck 3 looks like the production version of that same idea, cleaned up and pushed into daily use.

The timing lines up with a company digging in more places than it ever has before. The Boring Company now has multiple Prufrock machines active or arriving in Nashville, where Music City Loop construction has been accelerating since February, and its Vegas Loop network keeps adding tunnel mileage on a near monthly basis. Every one of those projects depends on getting concrete segments to the cutting face fast enough to keep the boring machine from idling, which is exactly the bottleneck Liner Truck 3 is designed to remove.

-

It also reinforces something Tesla owners have watched happen gradually across Musk’s companies: passenger car hardware finding a second life in heavy equipment. Model 3 drive units already move people through the Vegas Loop, and now the same components are hauling concrete underground in Nashville and wherever The Boring Company digs next. Whether that kind of component reuse extends further into TBC’s equipment lineup, or into other Musk owned industrial hardware, is the next thing worth watching.

Another Tesla SpaceX merger prediction by ARK Invest has Elon Musk talking

The real reason Elon Musk wants every car connected to space