Investor's Corner

Tesla Semi-truck: What will be the ROI and is it worth it?

Elon Musk’s announcement that a Tesla Semi will be arriving as early as September is the first step to what will eventually be a reinvention of an entire industry. We’ve discussed before what, exactly, that means, but given that the man in charge of the Tesla truck program is Jerome Guillen who has a history with Daimler (specifically Freightliner) and large Class 8 semi-trucks, it’s not hard to see where Tesla plans to go with this. That leaves only the question of how far, literally, they plan to take it. In tractor-trailer operations, there are two basic types of freight moving: short-haul and long-haul.

We’re going to look at each of these types of freight hauling and how the return on investment (ROI) for a battery-electric rig (such as that we expect Tesla to unveil) would be. If there is any. We’ll also consider what type of equipment this might entail, in a broad sense, and how that compares to current paradigms in tractor-trailer freight hauling.

Before we dive into that, a few words on what the trucking industry is like are needed. About 69.5 percent of the freight moved in the United States is moved on a commercial truck. The U.S. Department of Transportation (USDOT) also says that a staggering 92 percent of prepared foods are moved by trucks and 82.7 percent of agricultural products are moved by truck, as are 65 percent of pharmaceuticals. However you measure it, that’s a lot of goods being moved on highways and surface roads nationally.

Currently, the trucking industry is seeing a lot of change, internally, as technology improves the way that freight hauling operates. The Internet and faster communications, for example, has begun to erode the traditional consignee-broker-hauler paradigm in which someone with goods to haul contacted a freight broker who then contracted a freight hauler to move the goods, skimming a percentage off the top for the connection. The middleman is often cut out in today’s trucking, with many trucking companies having load brokers on staff.

Electronics and global positioning have also changed how trucks operate, with computers more efficiently organizing load and truck movements to minimize empty movement. The USDOT says that about 29 percent of all truck movement is pulling an empty trailer to or from a freight drop-off point, costing about $30 billion annually. That number, while high, has been dropping for some time and drops exponentially as networks of computers get more efficient at organizing trucking and trucking companies consolidate into larger and larger fleets.

Finally, we should note that the longer the average trip (load to delivery) is for a tractor-trailer, the faster the truck’s ROI for the owner. Shorter hauls have higher per-mile maintenance costs than do longer hauls. Even discounting the cost of fuel, that becomes true as equipment maintenance costs beyond engine and fuel are still higher with shorter distances. There are several reasons for this, including how often brakes are used, how much time is spent not working (idling or sitting), and higher incidences of accidents. To name a few. Many short-haul operations are undertaken on less than ideal roads and in areas where any kind of breakdown, including a flat tire, can mean hours wasted waiting for repair.

Knowing those things, we can look at potential ROI for both short-haul and long-haul Tesla electric semi-trucks.

-

-

Short Haul

Conventionally, short-haul operations are defined as being tractor-trailer shipments moving 250 miles or less and long-haul is defined as being those same types of shipments moving more than 250 miles. Each of these has sub-categories, of course, but in the main, those are the two major markets for large Class 8 semi-trucks pulling freight. It should be noted that the overlap between short-haul and long-haul is large, as many short-haul shipments are being carried to a distribution location where it’s reassembled for longer distance hauling.

Of the two operations, short-haul has the most diversity in terms of machines used and types of freight carried. It’s in this category that we find items as aggregate as grain freshly harvested from fields to stones to specialized equipment being carried. Sometimes by the same truck and driver over the course of a year’s work. It’s also in this category that we find specialized rigs meant for entering pit mines, climbing steep grades on primitive dirt roads, moving overweight and outsized items, and so forth. For the most part, trucks in this category are “day cabs” meaning they have no sleeper unit attached for the driver to use as a rest quarters when not at the wheel.

So far, the electrified Class 8 vehicles we’ve seen actually enter the market have nearly all fallen into the short-haul category. These have included battery-electric, hydrogen fuel cell, and hybrid units working as “yard dogs” moving trailers around a dock area, as portage trucks moving containers and freight out of port to staging areas or local distribution centers, and local area urban and suburban delivery vehicles. Currently, there is a large push in California to make all port vehicles (including container-moving trucks) as zero-emissions as possible.

The good news for battery-electric truck makers and those who aspire to become them is that, according to the USDOT, about half of all of the shipments (by value) is moved less than 250 miles. That accounts for about 80 percent of the weight being moved around the country. The bad news is that in this segment, less is paid per ton for that freight to be moved and, according to the American Transportation Research Institute, this segment only accounts for about 25 percent of the trucks on the road. Equipment age also tends to be higher in this category, with trucks being used for more years (and generally fewer miles) than compared to long-haul trucks.

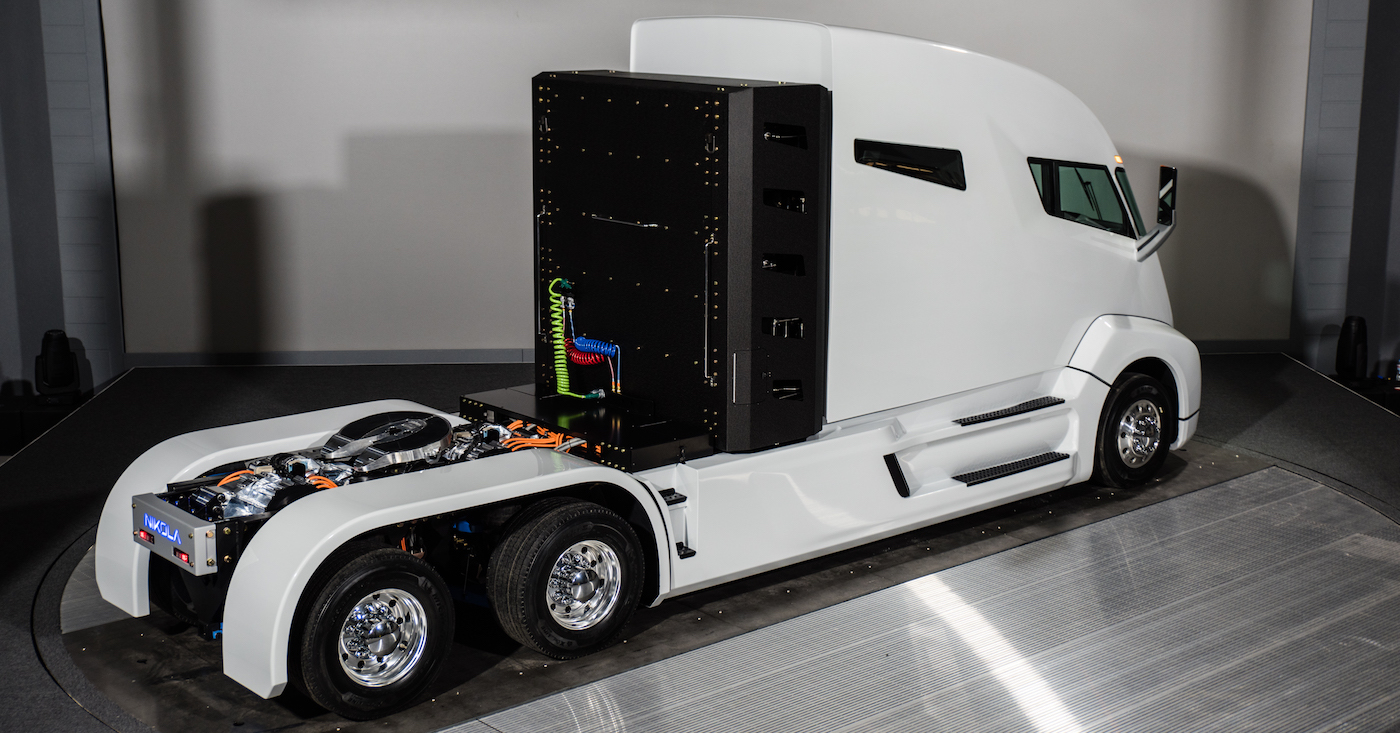

Nikola One all-electric Semi truck

In terms of cost, outside of maintenance, the most expensive items for a tractor-trailer, whether short- or long-haul, are fuel (38 percent), driver wages and benefits (34 percent), and truck-trailer lease payments and insurance (14 percent). These costs are about the same no matter what the truck is used for in most conventional operations, short-haul or long. Maintenance is about six percent higher in short-haul operations when compared to long-haul and insurance is usually a bit higher(1.5 percent), but not by so much that it can’t be averaged between them without skewing the numbers.

We can safely assume that a battery-electric semi-truck will have a higher price tag than its diesel-powered counterpart, which itself averages about $150,000 new. How much larger the electric truck would be is mostly conjecture, but we can probably be considered conservative to say it’s up-front costs will be at least 50 percent higher ($225,000) due to the expense of the batteries. Morgan Stanley’s report on electric and autonomous trucking assumed $75,000 for 500 kWh of battery storage, translating to roughly 150 or so miles of range in a fully loaded (80,000 pound) semi-truck. Given the current lithium crunch and the likelihood that economies of scale will take a lot of time to come to fruition, it’s easy to predict that more than half the Tesla Semi’s cost would be in batteries should it aim for a 250-mile range.

Over time, of course, that larger up-front price tag would be returned with fuel savings. In short-haul operations, about four years (250,000 miles) would be required to pay off $100,000 in battery premium with fuel savings. There are, however, other costs that would rise with the higher price of the rig. A higher-priced rig will have higher lease payments and higher insurance costs for replacement. This would stretch the ROI of the short-haul truck, by roughly another year, making it a five year investment return. If the truck stays in operation for the typical usage cycle in this segment, however, that would mean the truck pays for itself in about two thirds (70 percent) of its intended lifespan. Some percentage of the maintenance would also be lower in cost due to the nature of the electric truck, but much of it (tires, drivetrain, brakes, etc.) remains stagnant, further whittling at that ROI timeframe.

By and large, most forward-thinking fleet managers would jump at that. With one point of caution: by nature of their business and the long timeframes involved, most fleet managers are averse to change on a large scale. A few EV trucks here and there to prove out the technology and make the suits and ties happy are one thing. Jumping whole hog into the change is quite another. It would take some time (likely years) for fleet managers of short-haul fleets to decide that battery-electric trucks (or any type of unconventional powertrain) is a healthy decision. That, more than anything, will be the major delay towards adoption of something like a Tesla Semi.

-

Long-Haul Operations

Assuming that a Tesla Semi could be capable of hauling freight for 500-1,000 miles on a charge (the average long-haul trip is 600 miles per day), it would jump into a segment of trucking that accounts for more ton-miles than any other type of freight movement and that is growing faster than any other segment of commercial transportation in terms of both value and weight being moved. Further, the average turnover for a tractor in the long-haul business is 6.6 years (ATRI numbers) and the average mileage is over 110,000 miles per year per truck. ROI is typically faster as well, given the lower costs versus the miles driven.

Coming up with an ROI for a long-haul electric semi-truck is much trickier here and may be nearly impossible without knowing more about the EV truck to be used. At this stage, a battery-electric Tesla Semi would be nearly impossible for long-haul given the size and thus weight of the batteries required. So something involving very fast charging, battery swapping, or similar would be required. That adds costs to the equation that we cannot easily quantify without knowing what those logistics are.

What we can easily project is that the cost-benefit for a Tesla Semi in a long-haul scenario would not likely be nearly as compelling as it is for a short-haul fleet manager. A typical over-the-road truck sees about a million miles during its lifespan with a cost of about $400,000 in fuel and $100,000 in maintenance (ATRI) during that time. Most fleets own the truck for about seventy percent that time (700,000 miles), on average. So the cost of a truck, in terms of purchase price, fuel, and maintenance over its expected fleet lifespan is about half a million dollars ($280,000 fuel + $70,000 maintenance + $150,000 purchase = $500,000). This might begin to look very close to break even on a higher-priced EV truck by comparison, which would very likely save on fuel but would have higher up-front costs in balance. Further, those fuel savings might not be as good given the likelihood that logistics like battery swapping or more frequent stops for plugging in would be required.

Conclusion

A Tesla Semi would likely have a good return on investment for any fleet manager who is willing to look over the long-term and consider the cost-benefit. For the short-haul manager, however, the potential ROI is far more provocative than it would be for the long-haul manager. We can see a clear business case for a Tesla Semi for a large proportion of the short-haul industry, though we do caution that it will likely take some time for those in the industry to cast anything but a dubious eye towards an unconventional powertrain.

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

-

Cybertruck

Tesla Cybertruck production snaps back after ugly supplier fight

Cybertrucks are piling up again at Giga Texas after Tesla’s court win against a parts supplier.

Cybertruck production at Giga Texas is showing its first visible recovery since Tesla sued a supplier last month over withheld manufacturing tooling.

Aerial observer Joe Tegtmeyer flew over the Austin factory Wednesday morning and counted roughly 100 or more Cybertrucks filling the outbound lot, a sharp jump from the thin numbers seen in recent weeks. The flyover came a day after a judge granted Tesla a temporary restraining order against Angstrom Automotive Group, the parts supplier at the center of the dispute.

Tesla filed an emergency lawsuit in late July after Angstrom told the automaker it planned to close the Troy, Texas facility where Tesla’s die-cast tools, trim dies and other Cybertruck stamping equipment were housed. According to Tesla’s complaint, a shipment of 700 finished parts never left the building, and when Tesla sent representatives to retrieve its equipment, accompanied by law enforcement, they were turned away. Angstrom allegedly then asked for an extra $250,000 a week to keep operating, which Tesla’s filing described as holding its own property for ransom.

TESLA: U.S. District Judge Christopher R. Wolfe of the U.S. District Court for the Western District of Texas, Waco Division granted Tesla a Temporary Restraining Order and Writ of Replevin in its dispute with Angstrom Automotive (Case No. 6:26-cv-00477).

The order authorizes… https://t.co/E1DKcQSxMn pic.twitter.com/LR8aAiV2Og

— S.E. Robinson, Jr. (@SERobinsonJr) August 5, 2026

-

The restraining order gives Tesla immediate right of entry to Angstrom’s facility to recover the tooling. It is temporary, with a fuller hearing still to come, but the speed of Wednesday’s rebound suggests the Angstrom shortage was indeed the main bottleneck limiting Cybertruck output. Outbound lot counts are an imperfect measure of actual production, since finished trucks can sit for days before shipping, but a lot that full after a lean stretch is a meaningful signal.

Cybertruck output at Giga Texas has fluctuated all year as Tesla worked through supply issues and introduced new trims, including a cheaper Dual Motor AWD version that drew strong early demand.

Venture capitalist Chamath Palihapitiya has cautioned investors shorting SpaceX shares, drawing a direct parallel to the intense short-selling pressure Tesla faced in its early public years.

Responding to reports of elevated short interest in the newly public rocket, satellite, and AI company, Palihapitiya noted that similar dynamics played out with Tesla, where aggressive short sellers ultimately “went broke.”

SpaceX (NASDAQ: SPCX) went public on June 12, 2026, in the largest IPO on record, pricing at $135 per share. Shares quickly surged to an all-time high of $225.64 just days later, briefly implying a valuation exceeding $2 trillion. The stock has since retreated sharply amid valuation concerns, lockup expiration fears, and broader market dynamics.

By early August, it traded near $108–$125, representing a roughly 50 percent decline from the peak and bringing the market capitalization closer to the $1.5–1.7 trillion range. On August 4, shares closed up more than 9 percent at $125.33 ahead of earnings before facing pressure in after-hours and premarket trading.

Short interest has climbed dramatically. According to S3 Partners data widely cited in market reports, short positions reached approximately 219.3 million shares by late July, about 34 percent of the limited public float of roughly 640 million shares, and represented a notional value of around $24.6 billion.

Utilization of shares available to borrow hit 95 percent, with borrow fees rising. This level of shorting exceeded the dollar value of short bets against Tesla at the time and built rapidly ahead of two catalysts: the company’s first post-IPO earnings and an August 6 lockup expiration that could free up to 911.5 million additional shares.

-

CEO Elon Musk has issued warnings of his own. In mid-July, as short interest approached one-third of the float, he posted that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” reiterating his view that the company could ultimately be worth more than Earth if it achieves its goals.

On August 4, just before earnings, Musk responded to the latest short-interest data by saying, “I try to warn them, but they just double down.”

SpaceX delivered its first quarterly results as a public company after the close on August 4. Second-quarter revenue rose 92 percent year-over-year to $7.8 billion, beating consensus estimates near $6.8–6.9 billion.

The net loss narrowed to $541 million, or 9 cents per share, better than the roughly 23–24 cent loss expected. Starlink/connectivity contributed about $4.3 billion (up 66 percent), while the AI business generated $2.6 billion (up roughly 250 percent). Capital expenditures were heavy at $18.4 billion, largely tied to AI infrastructure. Management projected a $100 billion annualized revenue run rate by year-end 2026 and outlined a path toward $1 trillion in annual revenue by 2030.

The combination of Chamath’s historical reminder, Musk’s repeated alerts, and the company’s ambitious growth targets underscores the high-stakes debate surrounding SPCX. Short sellers are positioned for near-term supply pressure from the lockup, while long-term bulls point to Starlink scale, Starship progress, and AI compute expansion as reasons the bears may ultimately face the same fate as many early Tesla skeptics.

Inside Tesla’s secretive $10 Billion “Project Crystal Sun” filing

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it