Investor's Corner

TSLA critic and ‘Shark Tank’ judge Kevin O’Leary reverses course, buys Tesla stock

Legendary Canadian businessman and longtime Shark Tank Judge Kevin O’Leary, who previously remarked that he dislikes Tesla stock (NASDAQ:TSLA), has changed his tune on the electric car maker’s shares. In an appearance on CNBC, O’Leary stated that he personally bought some Tesla shares recently, in light of the company’s capability to attract the best talent in the field.

During his segment, the veteran Shark Tank judge related his observations after attending electric vehicle races. During these events, O’Leary stated that the engineers behind these incredibly fast, high-performance EVs would flock to Tesla staff in attendance for potential jobs in the company. Regardless of where these teams originated from, the engineers reportedly showed a notable interest in Tesla, and an equally noteworthy lack of interest in other automakers.

“Colleges and universities around the world with an engineering department generally puts forward an electric Formula 1 car and engineering teams in their graduating years race these cars all over the world. I’ve been hanging out at the pits with these engineers, and I’ve learned something extraordinary. When you go to one of these races… when the race is over, the winning team — they come from anywhere on Earth — who do they want to talk to?

“They want to talk to the Tesla hiring team there; the HR people hanging around at the pits. Every one of these engineers, the smoking hot kids that sit with their cars, the men and women that sleep with them for 24 hours a day; it’s an unusual culture I’ve never seen before. They all want to work at Tesla. Why? Because the teams are six to eight people. If they go to a legacy car company, they get drowned out in the back somewhere. These smart, young, men and women make a big difference as interns. I can’t believe the access to talent they have. That’s why I bought the stock,” O’Leary said.

While a CNBC host promptly commented that the Shark Tank judge’s reason for finally supporting TSLA stock was “random,” it should be noted that O’Leary’s about-face with the electric car maker’s shares is most likely a calculated decision. O’Leary, after all, does not give his support to a stock lightly. Just last year, for example, the investor admitted that he loves his Tesla Model X (which he purchased at the behest of his wife) and he considers Elon Musk a genius, but he hates TSLA stock. With this in mind, his change of tone with regards to the company’s shares bodes well for Tesla.

Tesla shares are somewhat on familiar, volatile territory following the release of its second-quarter report and earnings call. While the company ended Q2 2019 with a record $5 billion in cash, Tesla also showed a net loss of $408 million, translating to a loss of $2.31 per share, notably lower than Wall Street’s estimates. Commenting on the steep drop, longtime TSLA bull Ban Kallo of Baird argued that the market appears to be overreacting to Tesla’s Q2 results.

“Just back to the cash flow they generated during the quarter, there’s a couple of hundred million dollars, so this idea that they don’t make money is completely wrong, and the headline needs to change. There’s $5 billion in the balance sheet. They’re not going out of business. You have other OEMs that have really hard problems and restructuring problems. And it’s not Tesla; it’s XYZ German manufacturers,” he said.

As of writing, Tesla stock is trading at +0.43% at $229.01 per share.

Disclosure: I have no ownership in shares of TSLA and have no plans to initiate any positions within 72 hours.

Investor's Corner

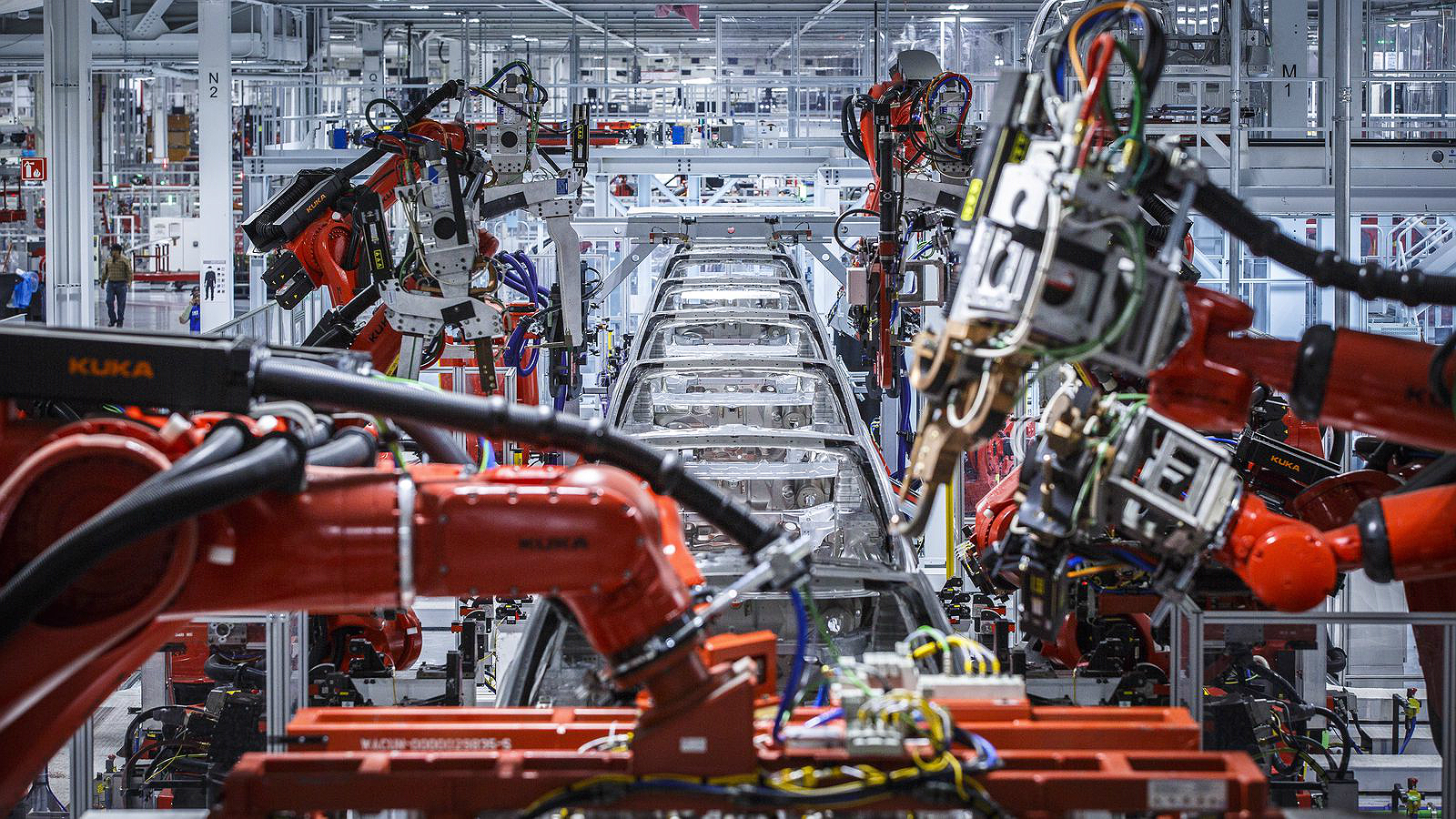

Tesla challenges startups to score a gig inside its most advanced European factory

Tesla is challenging startups to bring their best battery tech directly to Gigafactory Berlin.

Tesla has issued an open challenge to startups across Europe, inviting them to bring their best battery technology directly to the floor of Gigafactory Berlin. The program, called the JUNI x Tesla Battery Cell Giga Challenge, opened applications this month with a deadline of July 24, 2026, and is targeting startups with solutions that can make battery cell manufacturing faster, cheaper, safer, and more scalable at an industrial level.

The timing of the challenge is directly tied to Tesla’s most aggressive European battery investment yet. On May 12, 2026, Giga Berlin plant manager André Thierig announced a $250 million investment to scale the factory’s annual 4680 cell production capacity from 8 GWh to 18 GWh, more than doubling the previous target set just months earlier in December 2025. Thierig confirmed the expansion on X, saying the investment “will enable 18 GWh of annual 4680 cell production and create more than 1,500 new jobs.” Combined with a previously announced battery investment at the Grunheide site now approaches $1.2 billion.

Today, we announced a $ 250m investment for our Giga Berlin Cell factory. This will enable 18GWh of annual 4680 cell production and create more than 1500 new jobs. Good news during challenging times for the German industry. pic.twitter.com/ou4SWMfWh9

— André Thierig (@AndrThie) May 12, 2026

The challenge is looking specifically for startups with proven solutions across five categories: materials, equipment, operations, automation, and artificial intelligence. Applications are screened directly by Tesla’s cell manufacturing team in Grunheide, and the strongest submissions move through technical discussions, a pitch day in front of Tesla stakeholders, and potentially a paid pilot project with the cell team. Tesla is not looking for ideas at concept stage. The program requires applicants to demonstrate working prototypes, test data, or prior pilots before being considered.

The historical context matters here. Elon Musk first announced plans for what he called the world’s largest battery cell production facility alongside the Giga Berlin car factory back in 2020, targeting up to 250 GWh of annual capacity. Those plans were shelved in 2022 when Tesla shifted its battery investment focus to the United States to take advantage of Inflation Reduction Act incentives. The revival of cell production at Giga Berlin, now backed by over $1 billion in committed capital, represents a return to an ambition that was set aside for three years. As Teslarati has reported, the 4680 format is central to Tesla’s long-term cost reduction strategy across vehicles, energy storage, including the Tesla Semi and Cybercab.

By opening the challenge to outside startups, Tesla is acknowledging that reaching 18 GWh at Grunheide will require technology it does not currently have in-house, and it is willing to pay for the right solutions. For a startup in the battery supply chain, a paid pilot with Tesla’s European cell team is as close to a direct commercial path as the industry offers.

Investor's Corner

Tesla crushes Wall Street expectations, beats delivery estimates by over 15 percent

Tesla (NASDAQ: TSLA) beat Wall Street expectations of 406,000 vehicles delivered in Q2 by reporting 480,126 deliveries for the three months ending in June.

Tesla reported it delivered 467,762 Model 3 and Model Y units, while 12,364 Model S, Model X, and Cybertrucks switched hands during the quarter. The Model S and Model X were officially sunset this past quarter and will no longer be part of the company’s Production & Delivery reports moving forward.

🚨 BREAKING: Tesla delivered 480,126 vehicles in Q2, ANNIHILATING Wall Street expectations of 406,000. Production was reported at 451,758.

Deliveries:

Model 3/Y: 467,762

Other Models: 12,364Production:

Model 3/Y: 442,936

Other Models: 8,822 https://t.co/TTHwQAsKt8 pic.twitter.com/7qI4Zj6FE5— TESLARATI (@Teslarati) July 2, 2026

The quarter is a pleasant surprise and a good rebound from Q1, when Tesla slightly missed the Wall Street consensus of 365,645 cars by reporting 358,023 deliveries for the first three motnhs of the year.

Energy storage deployments also provided some strength in Tesla’s delivery report, hitting 13.5 GWh for Q2. This is a particular division of Tesla’s business that has been overwhelmingly robust over the past few years, truly being a strong point of the company’s overall model.

For the year, Tesla analysts still predict deliveries to trend in the 1.69 million unit region, a modest 3 to 5 percent increase from the 1.64 million cars the company delivered last year. Tesla will likely return to more sequential and noticeable year-over-year growth as the Cybercab project starts to ramp up considerably in the next few years.

Tesla has some other potential catalysts to spur vehicle deliveries, too. Not only is it expecting Cybercab to truly start making a change in the next few years, but other vehicles could be entering the company’s lineup.

Tesla sends production Cybercab with no steering wheel, pedals to on-road testing

The slightly longer Model Y L has been a highly speculated release candidate in the U.S. It has already done incredibly well in China, and U.S. buyers have been wanting slightly more interior space than the Model Y. Now that the Model X is gone, it is more needed than ever.

Q2 highlights a pretty stable automotive division within Tesla, and no true concerns arise from these figures, especially considering it managed to beat expectations convincingly.

Investor's Corner

Tesla gets its latest short from Michael Burry: ‘Happy it jumped back to this level’

Tesla short seller Michael Burry, the subject of the film “The Big Short,” where he was portrayed by Steve Carell, has revealed he has opened a new bet against the stock.

In a new update to his Substack newsletter in a post titled “Trading Post June 30, 2026,” Burry revealed a new set of bets against Tesla, Caterpillar, NVIDIA, Applied Materials Inc., and the iShares Semiconductor ETF.

In regard to Tesla, Burry wrote:

“And finally I shorted Tesla at 416.22. Happy it jumped back to this level.”

This means Burry likely opened his new short position after the company’s recent rally on Wall Street, which saw Tesla shares sink in mid-May, only to recover to well over the $400 mark. Currently, shares trade at around $427.

The company saw a big Tuesday as shares climbed considerably, over 10 percent. The size of the Tesla short was not provided, nor did Burry give any information on the position’s structure, the number of shares, dollar value, or whether options were used in the short.

The Tesla and SpaceX merger everyone is talking about is quietly building

Over the years, Burry has been one of the more vocal critics of Tesla, calling its share price “media inflated,” and saying it was “ridiculously overvalued” as recently as December.

The company has largely transitioned away from being known as an automotive company and instead is much more widely regarded as an AI play, mostly due to its Full Self-Driving efforts, Optimus robot development, and data collection related to both.

This has not pulled those skeptics away from being vocal about their distaste for how Tesla is valued, but there’s no denying that the company is a global force in many things, including sustainable energy, automotive, and AI.

Tesla flexes how it will help the blind with Cybercab

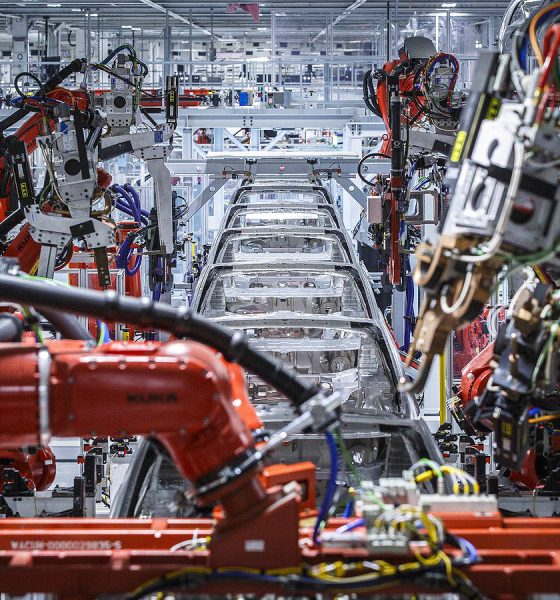

Tesla challenges startups to score a gig inside its most advanced European factory