News

Panasonic deepens ties with Tesla and bets big on Auto Tech

The following post was originally published on EVANNEX

As the inevitability of a major disruption in the auto industry becomes clearer, we’ve been reading (and writing) a lot about the companies that seem likely to lose out – Big Oil, incumbent automakers, some parts suppliers. But who will be the winners? Battery-makers obviously, but also providers of “auto tech.” This term includes the electronics that make electric powertrains go – motor controllers, inverters, chargers and the like – as well as self-driving hardware and software, and customer-facing components such as touchscreens, head-up displays and infotainment systems.

Tech companies are infiltrating the automotive space, making acquisitions and alliances to position themselves for profits under the new order. Last year, GM paid a billion bucks for Cruise Automation and invested half a billion in Lyft. Intel is putting its recent acquisition, Mobileye, to work in a partnership with BMW to build self-driving vehicles. Google is working with Fiat Chrysler on self-driving cars and providing display systems for Volvo. Israeli startup Otonomo is competing with Google and Apple to sell user data to Daimler and other automakers.

No company is better placed to thrive in the electric, automated future than Panasonic, which is steadily redirecting its focus from consumer electronics to auto tech. In February, Panasonic named Tom Gebhardt Chairman and CEO of its North American operations. Gebhardt’s former post was leading the company’s Automotive Systems subsidiary.

“Our business has evolved… from purely a consumer business to a B2B business,” Gebhardt recently told Business Insider. “There’s a number of reasons for that: The commoditization of consumer products [and] the unfavorability in some of the cost models led us to look for better values in in-vehicle technologies.”

Gebhardt said Panasonic is devoting more resources to digital cockpits and vehicle entertainment systems as self-driving vehicles get closer to reality. “If the scenario says the car drives itself, it’s similar to sitting in an airplane seat, because you’re no longer actively driving,” he said. “We see that as an evolution of the space that has infinite possibilities for us.”

-

-

Panasonic offered several glimpses of those possibilities at CES in January. Fiat Chrysler’s semi-autonomous Portal concept car featured a Panasonic touchscreen with facial and voice recognition. Panasonic also revealed a new system with a head-up display and augmented reality that’s designed to replace the traditional instrument cluster and many of the car’s physical controls. Some speculated that it was a preview of Model 3’s user interface. A few days later, Panasonic CEO Kazuhiro Tsuga said in an interview, “We are deeply interested in Tesla’s self-driving system. We are hoping to expand our collaboration by jointly developing devices for that, such as sensors.”

Meanwhile, Panasonic’s collaboration with Tesla on batteries gives it a large stake in the potential profits as electrification gathers momentum. Panasonic is one of the largest battery manufacturers in the world, and it plans to invest $1.6 billion in Tesla’s Gigafactory. And looking back, in 2007 Panasonic began working with Tesla on the Roadster and has established a strong track record supporting Tesla over the past decade — even investing $30 million with Tesla at a critical juncture (in 2010) in order to develop lithium-ion battery cells for its forthcoming Model S sedan.

A lot has changed since those early days. Nevertheless, global electric vehicle sales are still hovering around 1% of the market. That said, there are many reasons to expect a breakout soon. Orders for Tesla’s upcoming Model 3 keep growing, and legacy automakers from VW to BMW to Ford are responding with plans for new electric models.

“The future is definitely electric, no question in my mind,” Gebhardt said. “What is the future timeline? Is it 10 years, 15 years, 40 years? It’s just a matter of what the adoption hits at the scale that makes this a slam dunk… We’re pretty bullish on the fact that this is a space that will continue to grow and there’s value there.”

Gebhardt conceded that EV adoption is slow in the US, a trend that may continue now that the federal government has shifted from supporting electrification to trying to revive the elderly fossil fuel industries. However, he characterizes this as “a short-term problem,” and points out that it’s a very different scene in China, the world’s largest car market. “If they adopt in a big way, that changes the balance of where electric is today versus where it will be going.”

Panasonic’s increasing investment in auto tech is already paying off, according to Nikkei Asian Review. At a recent financial briefing, President Kazuhiro Tsuga said the company is expecting an increase in net profit in fiscal year 2017, its first gain in two years, largely because of strong growth in EV batteries and other auto tech-related products. “We are confident we can achieve increases both in sales and profit for the year through March 2018 and later years,” he said.

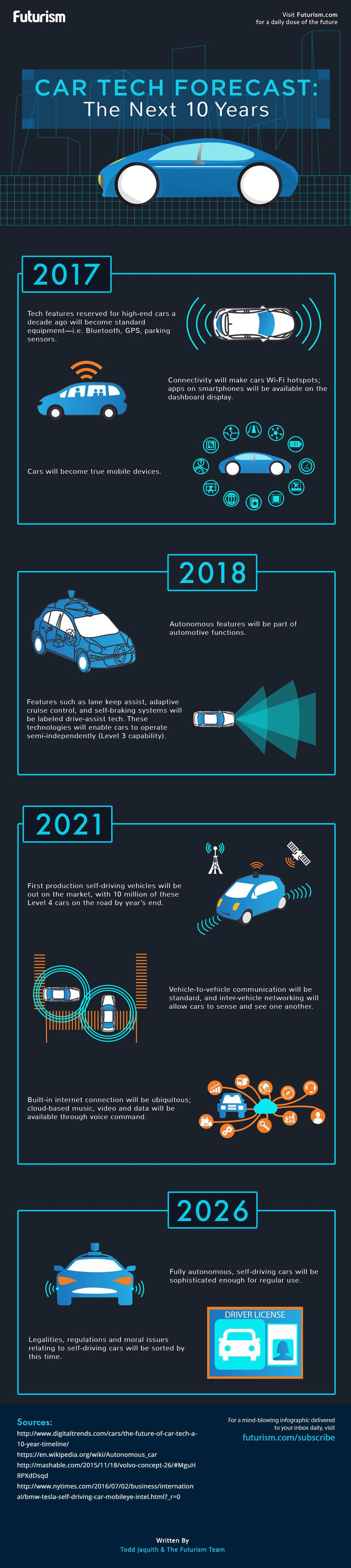

Infographic

-

What auto tech opportunities are coming in the next decade? Check out this infographic for a few possibilities…

Sources: Business Insider, Nikkei Asian Review / Infographic: Futurism

Elon Musk

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it

The Boring Company’s new tunnel vehicle runs on Tesla Model 3 batteries and drive units.

The Boring Company just introduced a new piece of hardware, and it runs on parts pulled straight from a Tesla showroom. Liner Truck 3, unveiled in a post from the tunneling company’s official X account, is an all electric vehicle built around Tesla Model 3 battery packs and drive units, purpose built to move concrete tunnel segments to the boring machine face without a single person underground.

Introducing Liner Truck 3 — our latest fully electric tunnel vehicle.

– Tesla Model 3 battery and drive units

– Transports 22,000+ lb of concrete segments to the boring machine

– 28 miles of range

– 12 mph max operating speed

– Remotely piloted from Global OCC in Texas, with… pic.twitter.com/XB7FgSXnpy— The Boring Company (@boringcompany) August 7, 2026

The job itself is unglamorous but critical. Each precast segment run weighs more than 22,000 pounds, roughly the load of a full cement mixer, and Liner Truck 3 hauls that weight repeatedly between the surface staging area and wherever the Prufrock machine happens to be cutting.

The Boring Company said Liner Truck 3 is piloted remotely out of its Global Operations Control Center in Texas, extending the Zero-People-In-Tunnel approach the company has spent years building toward. An earlier version of a ZPIT liner truck was already tested at the company’s Bastrop, Texas research tunnels, and a factory tour released last month showed an employee flying a fully loaded liner truck with a PlayStation controller. Liner Truck 3 looks like the production version of that same idea, cleaned up and pushed into daily use.

The timing lines up with a company digging in more places than it ever has before. The Boring Company now has multiple Prufrock machines active or arriving in Nashville, where Music City Loop construction has been accelerating since February, and its Vegas Loop network keeps adding tunnel mileage on a near monthly basis. Every one of those projects depends on getting concrete segments to the cutting face fast enough to keep the boring machine from idling, which is exactly the bottleneck Liner Truck 3 is designed to remove.

-

It also reinforces something Tesla owners have watched happen gradually across Musk’s companies: passenger car hardware finding a second life in heavy equipment. Model 3 drive units already move people through the Vegas Loop, and now the same components are hauling concrete underground in Nashville and wherever The Boring Company digs next. Whether that kind of component reuse extends further into TBC’s equipment lineup, or into other Musk owned industrial hardware, is the next thing worth watching.

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

-

News

The Boring Company’s newest Vegas Station has a permit quietly waiting behind it

Sahara Las Vegas opened a new Vegas Loop station, joining an exclusive two resort transit club.

Sahara Las Vegas opened a new Vegas Loop station Thursday, giving The Boring Company’s underground transit system its northernmost stop yet on the Strip. The station sits at Sahara’s Paradise Road entrance, on the southeast corner of Las Vegas Boulevard and Sahara Avenue, and connects riders to the Las Vegas Convention Center, other Strip resorts on the network and, eventually, Harry Reid International Airport.

The addition makes Sahara the second resort, after Fontainebleau opened its own station in January, to get a stop built at street level rather than tucked into the property itself. Sahara now joins Westgate as the only two Strip resorts offering both a Vegas Loop station and a stop on the Las Vegas Monorail, giving guests two separate ways to get around without leaving the property.

The Boring Company just doubled its tunneling power in Nashville

The bigger news buried in Thursday’s announcement is what comes next. Boring Company has already secured its first permit to tunnel north of Sahara Avenue, extending the network beyond where it currently ends, even though permits to push the Loop toward downtown Las Vegas still haven’t been granted. Crews are also working on a two mile dual tunnel line running from Westgate to a planned station at 4744 Paradise Road, just north of Tropicana Avenue, that Las Vegas Convention and Visitors Authority CEO Steve Hill has said the company hopes to open in time for November’s Las Vegas Grand Prix.

Ridership has grown alongside the buildout. The Loop moved roughly 82,000 passengers during CONEXPO in early March, a total the company highlighted on its own X account at the time, and the system has now carried more than 4 million passengers through 11 open stations since it began running in 2021. The airport connector tunnels, meant to give the Loop a direct link to Harry Reid, have slipped past their original first quarter target and remain under construction, with Boring Company director Mike Baier saying that a full opening is still a few months out.

For Sahara, the calculation is straightforward. Convention traffic drives a large share of Loop ridership, and a station at the property’s front door gives conventiongoers one more reason to book rooms on the Strip’s north end instead of closer to the convention center itself.

-

Inside Tesla’s secretive $10 Billion “Project Crystal Sun” filing

The Boring Company’s newest tunnel vehicle runs on Tesla parts and no one is driving it