SpaceX

SpaceX shows off first completed Crew Dragon spaceship with new Falcon 9

New photos posted from an official tour of SpaceX’s Pad 39A launch facilities reveal that SpaceX has effectively completed integration and preflight preparations of the company’s first flightworthy Crew Dragon spacecraft, as well as the new Falcon 9 Block 5 rocket that will be tasked with launching it early next year.

Currently targeting launch no earlier than (NET) January 17th, this inaugural Crew Dragon launch – known as Demonstration Mission 1 (DM-1) – will be conducted without a crew aboard to ensure that the spacecraft’s performance and characteristics fit within design parameters, hopefully giving NASA the data it needs to certify Crew Dragon to launch astronauts as early as June 2019.

omfg @spacex just posted some absolutely stunning photos inside Pad 39A's hangar: meet the first completed Crew Dragon and its Falcon 9 Block 5 rocket (B1051) 😀 In the far left (second photo), you can also see what is probably B1047 in the midst of refurbishment. pic.twitter.com/NWULyAEhpQ

— Eric Ralph (@13ericralph31) December 18, 2018

Aside from the wonderful fact that all (or nearly all) of the hardware needed for Crew Dragon’s launch debut can be seen in the four photos posted today, this is also the first time SpaceX has ever provided a real photo of the next-gen spacecraft’s trunk-based solar array. A dramatic departure from Cargo Dragon’s more traditional duo of multi-panel solar arrays, which deploy from disposable covers and fold out like wings, SpaceX decided from the start that Crew Dragon would take a much different approach. In a move that presumably cut the risk of solar array deployment, Crew Dragon’s panels are conformally attached (i.e. curved to fit) to the disposable trunk’s rear exterior.

Incredible opportunity to see @SpaceX's Dragon 2 Capsule – an important part of the future of American human space exploration as we aim to return American astronauts to space on U.S. rockets from U.S. soil! pic.twitter.com/Pk5lkpOFEX

— Vice President Mike Pence Archived (@VP45) December 18, 2018

-

-

Rather than deploying its arrays like wings, Crew Dragon will always have its solar cells ready and waiting to generate power, simply requiring the spacecraft to face one half of its trunk towards the sun. According to a few individuals involved with the trunk, guaranteeing food fitment between individual cells and subsections and avoiding the problems caused by different thermal expansion coefficients (shrinking and expanding as the temperature changes) was no easy task and led to many, many headaches in the final weeks of integration and testing. From a less objective standpoint, Crew Dragon’s new conformal solar array is absolutely stunning, and it will be a shame to see each sculpture-like trunk relegated to a destructive atmospheric reentry after each launch.

Pragmatically speaking, it’s extremely satisfying to see all the hardware (both rocket and spacecraft) effectively under the same roof at the launch pad they will soon lift off from. Much like Falcon Heavy, NASA’s Commercial Crew Program (CCP) has been beset with the better part of two years of delays from original launch targets in 2017 for both Boeing and SpaceX. Since then, a combination of NASA bureaucracy and technical/programmatic stumbles made by both companies have conspired to almost indefinitely delay the first uncrewed and crewed trips to orbit.

-

- At long last, SpaceX’s first completed Crew Dragon has been integrated with a flightworthy trunk and is awaiting attachment to Falcon 9. (SpaceX)

-

- The first complete Crew Dragon is likely just days away from rolling out to Pad 39A atop Falcon 9. (SpaceX)

-

- The DM-1 Crew Dragon testing inside SpaceX’s anechoic chamber, May 2018. (SpaceX)

-

- SpaceX’s Demo Mission-1 Crew Dragon seen preparing for vacuum tests at a NASA-run facility, June 2018. (SpaceX)

-

- The first spaceworthy Crew Dragon capsule is already in Florida, preparing for its November 2018 launch debut. The same capsule will be refurbished and reflown as few as three months after recovery. (SpaceX)

-

- Crew Dragon arrives at ISS. (SpaceX)

-

- DM-2 astronauts Bob Behnken and Doug Hurley train for their first flight in Crew Dragon. (NASA)

SpaceX suffered catastrophic Falcon 9 failures in both 2015 and 2016 and has largely been working to ameliorate the technical and organizational flaws that allowed those anomalies to occur, while also having to convince NASA that they are ready to safeguard the lives of the space agency’s astronauts. Since SpaceX’s last known total vehicle failure in September 2016, Falcon 9 and Falcon Heavy have managed an extraordinary 37 successful launches in a row in a little more than 24 months.

SpaceX is targeting Crew Dragon’s first orbital launch sometime in January 2019, with the placeholded launch date currently sitting on January 17th, pending International Space Station (ISS) availability and NASA’s go-ahead. Given the presence of Falcon 9 B1051 in 39A’s integration hangar and the fact that SpaceX technicians already appear to be integrating the first and second stages, the company may well be ready to perform a full-up dress rehearsal – involving Falcon 9 and Crew Dragon rolling out and going vertical on Pad 39A – before 2018 is out.

For prompt updates, on-the-ground perspectives, and unique glimpses of SpaceX’s rocket recovery fleet check out our brand new LaunchPad and LandingZone newsletters!

-

SpaceX stock did the opposite of what most of Wall Street expected this week, when the day designed to be its most dangerous turned into a rally, and the rally kept going.

Thursday marked the first major lockup expiration since SpaceX’s June IPO, making roughly 911.5 million insider held shares eligible to trade for the first time, more than doubling the company’s public float. Analysts and short sellers had spent weeks bracing for a flood of selling, especially after the stock fell 13 percent following its first earnings report as a public company on Tuesday. Instead, shares rose 6.1 percent Thursday to close at $114.92, and by Friday they were trading near $129, up more than another 12 percent on the day.

SpaceX shorts get warned by Musk ally, echoing Tesla’s early struggles

The setup made the outcome notable. Short interest had climbed to roughly 34 percent of the float heading into earnings, among the highest of any large cap stock, with about 95 percent of available shares to borrow already on loan. CEO Elon Musk warned short sellers twice in the weeks before the lockup, writing on X that “the survival probability of firms who maintain a significant short position in SpaceX over time is very low,” then following up on the morning of earnings with “I try to warn them, but they just double down.”

When the newly unlocked shares hit the market and the selloff never showed up, some of that short position appears to have started unwinding. TipRanks reported that options activity shifted toward bullish strategies like put selling and risk reversals following the rally, with roughly $600 million in options premium trading Thursday alone. Retail buyers also stepped in during the earnings dip, according to Vanda Research.

The fundamentals behind the stock have not changed much in a week. SpaceX’s revenue nearly doubled year over year to $7.8 billion, with Starlink subscribers doubling to 12 million and the company’s AI segment growing 247 percent. What spooked investors on Tuesday was the spending side. Capital expenditures jumped to more than $18 billion for the quarter, up from $2.8 billion a year earlier, with AI investment alone rising from $749 million to $15.8 billion. Wall Street remains split on whether that spending is building infrastructure SpaceX needs or outrunning what the business can currently support, a debate Teslarati has tracked since shares first came under pressure.

None of that resolves the bigger question hanging over the stock. Thursday’s release was only the first of nine staggered lockup tranches, with roughly $800 billion worth of additional shares scheduled to become eligible through October, and Musk’s own stake stays locked until next June. If this week is any indication, the market is treating that supply as something it can absorb rather than something to fear, at least for now.

-

Elon Musk

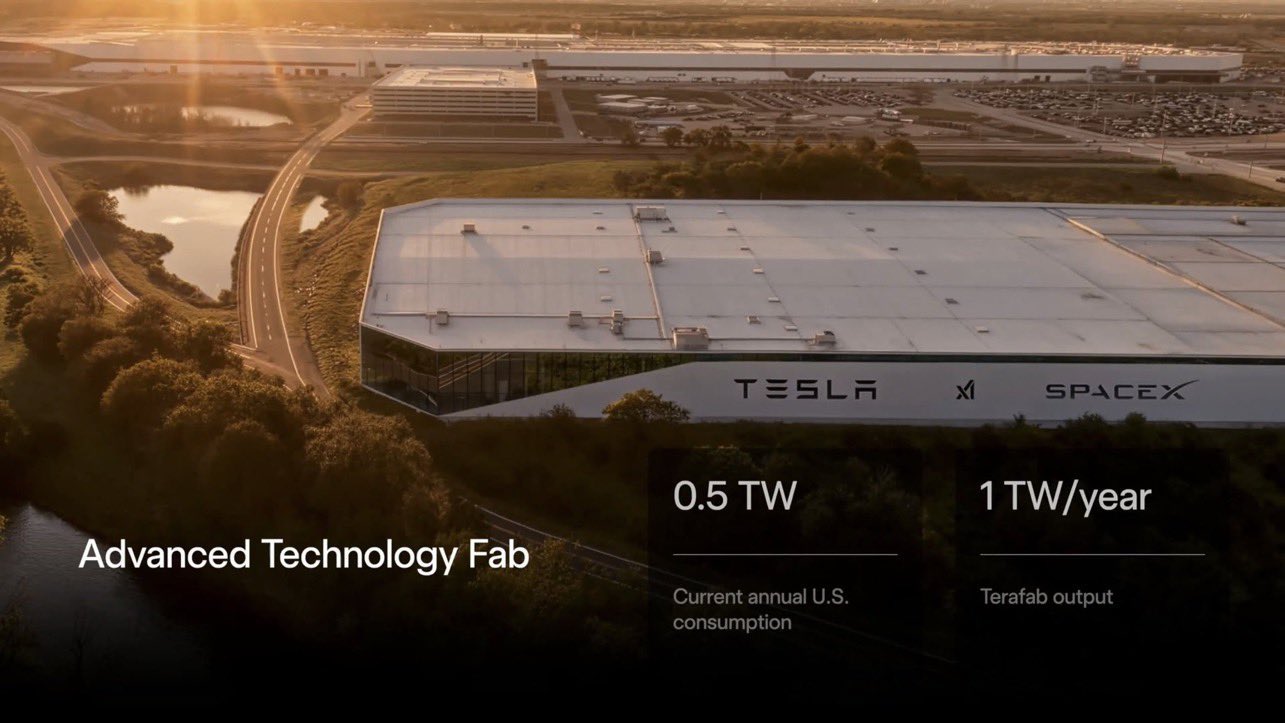

Tesla’s mysterious Robovan makes a sneak peek with Optimus in Terafab video

Elon Musk shared a new Terafab video showing Optimus, Robovans, and a stunningly futuristic campus.

Elon Musk posted a new video of Terafab on X Thursday morning, and the most eye-catching details in it were not the building itself, but two products still awaiting production: Optimus and the Robovan.

The concept render, credited to SpaceX, shows Optimus robots working the grounds of the roughly 2.5-mile-long facility planned for the Gibbons Creek site in Grimes County, while a Robovan glides along an elevated roadway cutting through the building itself, sharing the frame with a Tesla Semi and a Cybercab.

Robovan is the boxy, driverless people and cargo mover Musk unveiled alongside Cybercab at Tesla’s “We, Robot” event in October 2024. He pitched it as a way to move up to 20 passengers at once, or handle freight instead, at a target cost he claimed could fall under a dollar a mile, with no steering wheel or pedals, the same layout as Cybercab. Nearly two years later, Robovan still has no confirmed production timeline and has not shown up in any factory footage, which makes Thursday’s render one of the only recent looks at the vehicle in any form.

Terafab Texas will be the largest and most valuable building on Earth by far.

And it will be stunningly beautiful. pic.twitter.com/4NweOqTL7y

— Elon Musk (@elonmusk) August 6, 2026

Optimus has moved further along. Tesla began converting Fremont’s old Model S and Model X assembly line into a Gen 3 Optimus production line earlier this year, and Musk visited the site on July 1 to mark the changeover. A second, larger Optimus plant is under construction at Giga Texas, targeting volume production in summer 2027 and eventual capacity of 10 million units a year. Tesla AI lead Ashok Elluswamy said this month the robot has “big shoes to fill” in replacing the S and X line, while Musk has repeatedly called Optimus the company’s biggest product of any kind, with a long-term price he has pegged between $20,000 and $30,000.

-

Check out the “Robovan” from @Tesla

📸: @Teslarati pic.twitter.com/D4es2i9NUe

— TESLARATI (@Teslarati) October 11, 2024

“Terafab Texas will be the largest and most valuable building on Earth by far,” Musk wrote alongside the clip. “And it will be stunningly beautiful.”

One quote post summed up the reaction: “Futuristic scene with RoboVan + Cybercab + Tesla Semi + Optimus.”

Beyond the vehicles, the architecture wrapped around them stands out too. The building’s facade is canted at sharp angles, with illuminated horizontal bands running through what appears to be a multi level interior visible from outside. Below the elevated roadway, pedestrians walk along a plaza next to a reflecting pool, and the skyline behind the campus is dotted with angular spires that read more like sculpture than infrastructure, a departure from the strictly utilitarian look of Gigafactory Texas or Starbase.

The timing tracks with what Terafab representative Riley Trennell told Grimes County residents on Wednesday, when he said renderings of the facility would be released “within days.” Musk’s post followed less than 24 hours later, and Texas Governor Greg Abbott’s office sent out its own release Thursday confirming the project. As Teslarati reported this morning, Terafab’s tax abatement agreements with Grimes County are now signed and active, and SpaceX has sent the county its first $10 million payment under that deal. The dollar figure tied to this phase of construction, per Reuters, is $16.8 billion, one of the first hard capital expenditure numbers attached to Terafab since Musk unveiled the joint Tesla-SpaceX-xAI venture in March.Reaction on X ranged from enthusiastic to skeptical. “God Bless Texas! Everything is bigger and better in Texas!” one reply read. Another was more measured: “Terafab in a decade…..”

Whether the finished building matches the render is a separate question from whether Musk wanted people talking about the render itself. Less than a day after posting, the video had already crossed 5.5 million views.

-

Elon Musk

Space finally faced the people living next to its next Terafab mega-project

SpaceX confirmed Terafab’s Grimes County site is locked in, with construction starting within months.

SpaceX and Terafab representatives sat across from Grimes County residents for the first time on Wednesday, telling a packed Commissioners Court room that the $55 billion chip manufacturing project is now a done deal at the Gibbons Creek Reservoir site.

The meeting followed a $10 million check SpaceX sent the county earlier this week, satisfying a payment deadline built into the tax abatement agreement both sides signed in June. Elon Musk shared a post on X confirming the payment, and County Judge Joe Fauth told the San Antonio Express-News his office deposited the check after it beat its deadline.

Wednesday’s session, first reported by KBTX, moved the project from paperwork to construction. Terafab representative Riley Trennell told residents the JETI tax break agreements with Iola ISD and Anderson-Shiro CISD are signed and active, and that civil work and foundation prep are starting almost immediately. Renderings of the facility could be released within days, he said, with construction beginning within months.

The foundations for an exciting future are being built in Texas. Next up: Terafab → https://t.co/jGg52Zhn5I pic.twitter.com/SNfSXNr2tb

— SpaceX (@SpaceX) August 6, 2026

Elon Musk launches TERAFAB: The $25B Tesla-SpaceXAI chip factory that will rewire the AI industry

Musk first announced Terafab in March as a joint venture between Tesla, SpaceX and xAI aimed at producing over a terawatt of AI compute annually, an amount that dwarfs the roughly 20 gigawatts the entire global chip industry produces today. Intel joined as a manufacturing partner in April. Musk has said the project needed its own day in the spotlight rather than being squeezed into an earnings call, and for months the Grimes County site remained unconfirmed even as reporting pointed there.

-

SpaceX attorney Buck Brannon used Wednesday’s meeting to note that the company’s abatement is roughly 78 percent, not the 100 percent some earlier reports suggested. In exchange, SpaceX will pay Grimes County a fixed $20 million a year for 35 years, a total of $710 million, which Brannon said exceeds the $14 million Tesla paid Travis County in 2025.

SpaceX also addressed environmental concerns that have followed the project since Musk’s Terafab partnership with Intel was announced. Representatives said Terafab will not raise electric bills for other ratepayers, will not deplete local water supplies and will not draw down the Navasota River. SpaceX confirmed it owns the Navasota River pumping station, which it plans to use to divert stormwater into the Gibbons Creek Reservoir, and said it will build its own natural gas plants to power the facility rather than pulling from the ERCOT grid.

Grimes County commissioners also approved an addendum letting county employees use ten approved AI chatbots for work, including Grok.

Elon Musk and SpaceX shrugs off the trading day Wall Street feared most

The Boring Company’s newest Vegas Station has a permit quietly waiting behind it