News

Ford’s top brass sit down with Sandy Munro to discuss the F-150 Lightning

Ford CEO Jim Farley and other company executives were interviewed by Sandy Munro earlier this week, highlighting the work done on the F-150 Lightning, its defining features, as well as Ford’s future more generally.

Sandy Munro of Munro Associates runs a YouTube channel where he and his team dive into different models of vehicles and analyze their dependability, durability, and overall engineering design work. However, Sandy and fellow Munro associate Cory Steuben got to sit down with top leaders from Ford, which included Farley, Linda Zhang, who was the Chief Engineer of the all-electric pickup, and Doug Field, the automaker’s Chief Officer of EVs. Mainly focusing on the F-150 Lightning but also talking about the brand’s future and competitors, the interview culminated as Sandy asked the executive team about possible vertical integration within their manufacturing process, possible partnerships with Tesla, and a possible switch to the Tesla connector as the US default.

The video starts with Sandy getting the keys to his new F-150 Lightning, kindly delivered in person by Jim Farley and the team. However, Sandy quickly moves to ask about the truck and its design.

While Sandy was quick to praise the EV drivetrain and the durability of design, foremost thought the interview; the executive team focused on accessory features instead. Doug Field specifically sees the onboard generator, the large frunk, and the bi-directional power (the feature that allows the truck to power the home during a blackout) as the top reasons consumers have flocked to the new truck. Farley continues by noting that, while he didn’t expect the vehicle’s features to be such a crowd pleaser, he believes that they are the reason consumers aren’t asking “why an EV,” but “why not!”

The rest of the interview generally focuses on the market and the Ford brand. The biggest question is the thought of exponential growth in the EV market. Sandy notes explicitly that the US market had recently reached a 5% market share of EVs, what he calls a “tipping point” in the market. Jim responds positively, noting that he is excited about the chance to expand so quickly, expanding older plants such as “The Rouge” and constructing new plants like their new facility in Tennessee to meet demand. Further, he notes he isn’t worried about the brand’s ability to meet demand.

Another big question on the mind of Sandy (and many others who are interested in EVs) is the question of a partnership with Tesla, as well as the executives’ thoughts on the recent proposal to make the Tesla connector the new US standard. “We consider everything,” Doug responds tritely. The team responds to a Tesla partnership, saying that Ford would need a powerful motivating idea to consider abandoning their independence and partnering with another maker, Tesla or otherwise. However, none of the team concretely answered Sandy’s question about standardizing the Tesla Connector.

The group next addresses the possibility of increased verticle integration within their manufacturing. Software, batteries, and powertrain parts were essential parts where they stated the brand would likely continue to pursue verticle integration, going as far as to call other battery makers such as CATL “competitors.” However, Farley notes that he would not compromise the user experience in efforts of verticle integration.

-

-

Sandy concludes by lamenting the lack of the $20-$25,000 EV. He mentions that the in-demand Maverick is an excellent example of a vehicle that shows affordable vehicles can still do well and prove profitable for brands like Ford. Doug responds conservatively that, while they see the segment as “very important for global competitiveness,” difficulties remain in acquiring affordable powertrain parts and batteries. And while LFP batteries may offer an avenue into that market, Ford is still in the process of “considering other options.”

Sandy’s interview shows that Ford remains quite dedicated to pursuing EV tech and why they remain ahead of previous rivals such as GM and the Chrysler family of brands. Farley is thinking ahead of many of these other legacy brands, and despite the hurdles that come with that status (cough cough dealerships cough cough), they are positioning themselves well to succeed. Ford’s sales and stock price seem to reflect this.

What do you think of the article? Do you have any comments, questions, or concerns? Shoot me an email at william@teslarati.com. You can also reach me on Twitter @WilliamWritin. If you have news tips, email us at tips@teslarati.com!

-

-

Cybertruck

Tesla Cybertruck production snaps back after ugly supplier fight

Cybertrucks are piling up again at Giga Texas after Tesla’s court win against a parts supplier.

Cybertruck production at Giga Texas is showing its first visible recovery since Tesla sued a supplier last month over withheld manufacturing tooling.

Aerial observer Joe Tegtmeyer flew over the Austin factory Wednesday morning and counted roughly 100 or more Cybertrucks filling the outbound lot, a sharp jump from the thin numbers seen in recent weeks. The flyover came a day after a judge granted Tesla a temporary restraining order against Angstrom Automotive Group, the parts supplier at the center of the dispute.

Tesla filed an emergency lawsuit in late July after Angstrom told the automaker it planned to close the Troy, Texas facility where Tesla’s die-cast tools, trim dies and other Cybertruck stamping equipment were housed. According to Tesla’s complaint, a shipment of 700 finished parts never left the building, and when Tesla sent representatives to retrieve its equipment, accompanied by law enforcement, they were turned away. Angstrom allegedly then asked for an extra $250,000 a week to keep operating, which Tesla’s filing described as holding its own property for ransom.

TESLA: U.S. District Judge Christopher R. Wolfe of the U.S. District Court for the Western District of Texas, Waco Division granted Tesla a Temporary Restraining Order and Writ of Replevin in its dispute with Angstrom Automotive (Case No. 6:26-cv-00477).

The order authorizes… https://t.co/E1DKcQSxMn pic.twitter.com/LR8aAiV2Og

— S.E. Robinson, Jr. (@SERobinsonJr) August 5, 2026

-

The restraining order gives Tesla immediate right of entry to Angstrom’s facility to recover the tooling. It is temporary, with a fuller hearing still to come, but the speed of Wednesday’s rebound suggests the Angstrom shortage was indeed the main bottleneck limiting Cybertruck output. Outbound lot counts are an imperfect measure of actual production, since finished trucks can sit for days before shipping, but a lot that full after a lean stretch is a meaningful signal.

Cybertruck output at Giga Texas has fluctuated all year as Tesla worked through supply issues and introduced new trims, including a cheaper Dual Motor AWD version that drew strong early demand.

Elon Musk

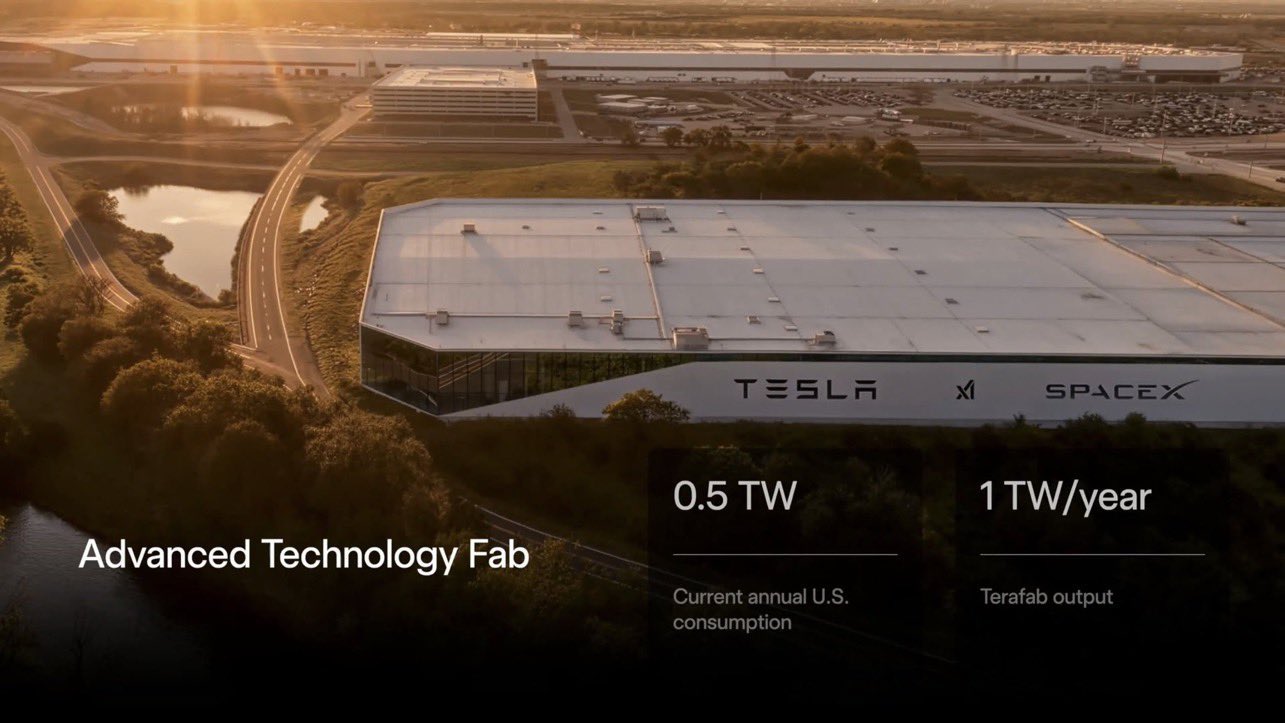

Space finally faced the people living next to its next Terafab mega-project

SpaceX confirmed Terafab’s Grimes County site is locked in, with construction starting within months.

SpaceX and Terafab representatives sat across from Grimes County residents for the first time on Wednesday, telling a packed Commissioners Court room that the $55 billion chip manufacturing project is now a done deal at the Gibbons Creek Reservoir site.

The meeting followed a $10 million check SpaceX sent the county earlier this week, satisfying a payment deadline built into the tax abatement agreement both sides signed in June. Elon Musk shared a post on X confirming the payment, and County Judge Joe Fauth told the San Antonio Express-News his office deposited the check after it beat its deadline.

Wednesday’s session, first reported by KBTX, moved the project from paperwork to construction. Terafab representative Riley Trennell told residents the JETI tax break agreements with Iola ISD and Anderson-Shiro CISD are signed and active, and that civil work and foundation prep are starting almost immediately. Renderings of the facility could be released within days, he said, with construction beginning within months.

The foundations for an exciting future are being built in Texas. Next up: Terafab → https://t.co/jGg52Zhn5I pic.twitter.com/SNfSXNr2tb

— SpaceX (@SpaceX) August 6, 2026

Elon Musk launches TERAFAB: The $25B Tesla-SpaceXAI chip factory that will rewire the AI industry

Musk first announced Terafab in March as a joint venture between Tesla, SpaceX and xAI aimed at producing over a terawatt of AI compute annually, an amount that dwarfs the roughly 20 gigawatts the entire global chip industry produces today. Intel joined as a manufacturing partner in April. Musk has said the project needed its own day in the spotlight rather than being squeezed into an earnings call, and for months the Grimes County site remained unconfirmed even as reporting pointed there.

-

SpaceX attorney Buck Brannon used Wednesday’s meeting to note that the company’s abatement is roughly 78 percent, not the 100 percent some earlier reports suggested. In exchange, SpaceX will pay Grimes County a fixed $20 million a year for 35 years, a total of $710 million, which Brannon said exceeds the $14 million Tesla paid Travis County in 2025.

SpaceX also addressed environmental concerns that have followed the project since Musk’s Terafab partnership with Intel was announced. Representatives said Terafab will not raise electric bills for other ratepayers, will not deplete local water supplies and will not draw down the Navasota River. SpaceX confirmed it owns the Navasota River pumping station, which it plans to use to divert stormwater into the Gibbons Creek Reservoir, and said it will build its own natural gas plants to power the facility rather than pulling from the ERCOT grid.

Grimes County commissioners also approved an addendum letting county employees use ten approved AI chatbots for work, including Grok.

Elon Musk has declared that SpaceX has effectively solved one of Starship’s most persistent engineering challenges: the reliability of its heat shield tiles.

During the company’s first-ever Earnings Call, the SpaceX CEO stated:

“I don’t want to jinx it or anything, but I think I would call the heat shield problem solved at this point. All indications from data and visual inspection is we have solved it. That doesn’t mean we won’t make improvements, but we do not see any technical obstacles to achieving rapid reusability at this point.”

Starship’s heat shield consists of roughly 18,000 hexagonal ceramic tiles covering the windward side of the upper stage. These tiles form the thermal protection system that shields the vehicle’s stainless-steel structure from the extreme heat of atmospheric reentry.

Elon says he believes the heat shield problem with Starship is currently solved.

He called it “arguably the single biggest problem” pic.twitter.com/eEE9vM5zlz

— TESLARATI (@Teslarati) August 4, 2026

-

During descent, atmospheric friction generates temperatures exceeding several thousand degrees Celsius and creates plasma flows capable of melting unprotected metal. The tiles absorb, radiate, and insulate against this energy, allowing the vehicle to survive and potentially fly again. Without a durable heat shield, full and rapid reusability, the cornerstone of Starship’s design for frequent launches, satellite deployments, and deep-space missions, would remain impossible.

The tiles have long been a source of difficulty. On earlier test flights, a significant number of tiles detached during ascent due to vibration, aerodynamic loads, and imperfect attachment methods using pins and adhesives. Gaps between tiles allowed hot plasma to infiltrate, causing secondary damage and hot spots on the underlying structure.

These issues echoed challenges faced by NASA’s Space Shuttle, whose ceramic tiles required extensive, labor-intensive inspections and replacements between missions, preventing rapid turnaround. SpaceX has iteratively improved materials, standardized tile shapes, refined attachment techniques, added secondary ablative layers, and tested sealing methods such as “crunch wrap” felt to close gaps.

Progress was visible across Flights 10–12, with steadily better tile retention, yet questions remained about whether the system could support the minimal-refurbishment goal of rapid reuse.

Flight 13 on July 24 provided the decisive evidence. Ship 40 flew a deliberately more demanding profile with higher dynamic pressure to stress the heat shield beyond typical operational loads. It successfully deployed 20 operational Starlink V3 satellites, the first such payload on a Starship mission, performed an in-space Raptor engine relight, and executed a controlled reentry.

Elon Musk sheds two new bits of detail on Starship after 13th test launch

Cameras on six of the satellites and onboard sensors captured extensive imagery and data of the shield throughout the flight. The ship then achieved its softest splashdown to date in the Indian Ocean, remaining intact and floating rather than breaking apart or exploding as on prior missions. This allowed drone inspections and continuous telemetry of the heat shield in near-real time.

-

Post-flight analysis showed the majority of tiles remaining attached with only minor damage and limited plasma streaking at seams. Musk noted that the mission delivered “all the heat shield data we needed and then some.” Combined with visual inspections, these results underpinned his subsequent assessment that the core technical barriers to rapid reusability have been cleared. While refinements will continue, Flight 13 marked a pivotal step toward Starship’s operational future.

Tesla Cybertruck production snaps back after ugly supplier fight

Space finally faced the people living next to its next Terafab mega-project