Investor's Corner

Tesla Model 3 production in Gigafactory 3 could ‘make a gazillion bucks:’ teardown expert

Earlier today, Tesla’s Gigafactory in China, which is expected to produce the affordable versions of the Model 3 and the Model Y, held its groundbreaking event. During the ceremony, Elon Musk was optimistic, stating that Tesla would likely start producing the electric sedan in the facility sometime before the end of the year.

If automotive veteran and teardown expert Sandy Munro’s insights are any indication, building the Model 3 in China is definitely the correct strategy for the electric car maker. In a recent appearance in YouTube’s Autoline Network channel, Munro remarked that if Tesla optimizes the Model 3’s production in China, the electric vehicle will generate a lot of profit for the company.

“When (Elon Musk) takes (the Model 3) to China, (Tesla’s) gonna make a gazillion bucks. I guarantee it,” Munro remarked.

Munro has not always been impressed with the Model 3 and its potential. Quite the contrary. When he started his teardown of an early production Model 3, Munro was aghast, comparing the build quality of the vehicle to a Kia from the 1990s and remarking that he “can’t imagine how (Tesla) released this (car).” After going through the vehicle’s panel gaps and what he believes are design flaws on the Model 3’s body, Munro summarized his observations by stating that “this thing is a miserable job.”

A few months later, Munro was singing a different tune. In a later segment on the auto-themed YouTube channel, the teardown expert noted that he had to “eat a lot of crow” when his team finished their analysis of the Model 3. Munro noted that while the vehicle’s bodywork left much to be desired, everything from the suspension of the Model 3 to its battery pack was a feat of engineering. The electric car’s batteries were top-notch, the ride was great, and the electronics were comparable to military-grade tech.

Most of all, Munro noted that the Model 3 will be profitable for Tesla, especially due to the company’s vertical integration and possible efficiencies in the vehicle’s construction. Before Munro could discuss his findings further, though, Autoline Network host John McElroy mentioned in a following episode of the program that Munro was being threatened with a lawsuit by an entity connected to his Model 3 teardown and analysis. Since then, Munro’s insights were shuttered — or so it seemed.

The automotive teardown expert finally made his return on Autoline Network in a recent episode. Returning to the show, Munro had a set of new updates and insights about his team’s Model 3 teardown. While Munro maintains that the Model 3’s body was over-engineered, he did note that “the good part is everything else.” The auto veteran pointed out that the Model 3 had the best electronics his team has ever seen, it had the lowest number of hoses, 40% less harnesses, and the electric motors are smaller, lighter, and more powerful than the competition.

“They’ve got magic. The electric motor is smaller and lighter than everybody else, but outperforms everybody,” Munro said.

With regards to Tesla’s Gigafactory 3 push and the production of the Model 3 on the site, Munro proved optimistic. The auto veteran even noted that Tesla’s Model 3 lines in China would likely be a lot more optimized than those in the United States.

“Elon made a few mistakes on that body. You think he’s gonna do it again? I don’t. You think the production lines are gonna be as bad as in California? I don’t. I think the factory in China is going to be wicked compared to what they’ve got in the States, and I think he’s going to be able to clobber everyone in China,” he said.

With Tesla accelerating the timeline for Gigafactory 3’s construction, the company can only hope that the Model 3 — its most disruptive vehicle in its lineup — could do its magic in the largest auto market in the world.

Watch Sandy Munro’s recent appearance at Autoline Network in the video below.

Elon Musk

TIME honors SpaceX’s Gwynne Shotwell: From employee No. 7 to world’s most valuable company

Time Magazine honors Gwynne Shotwell as SpaceX reaches a $1.25 trillion valuation and eyes its IPO.

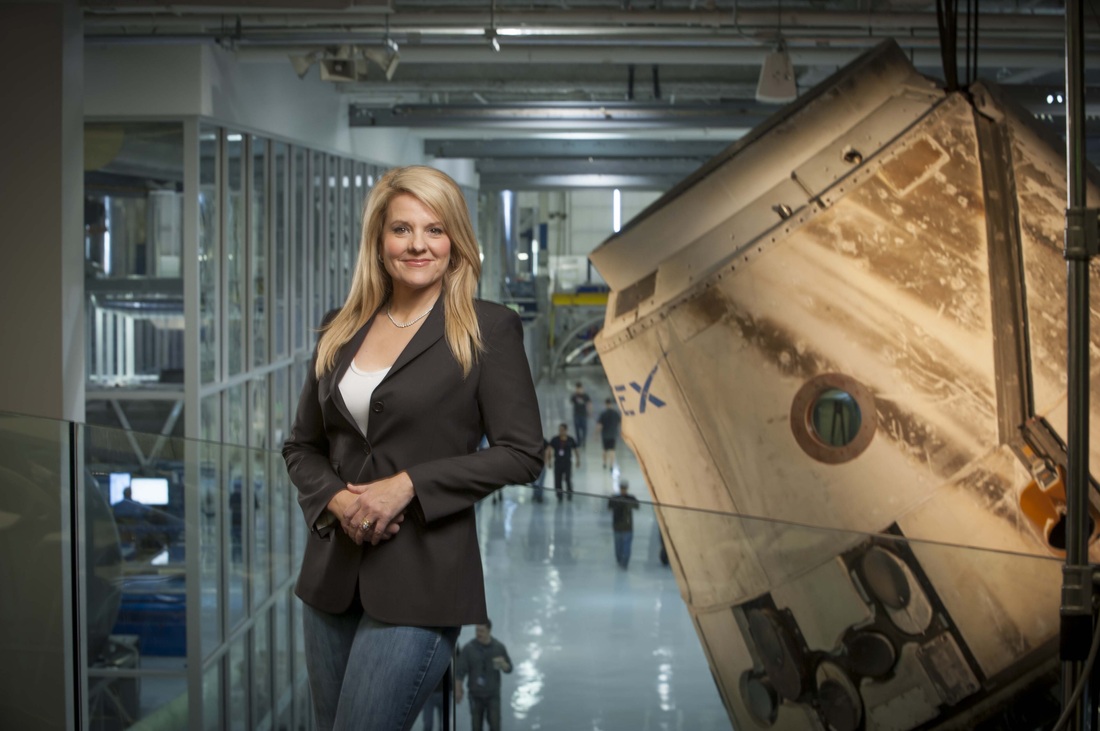

TIME Magazine has put SpaceX President and COO Gwynne Shotwell on its cover, and the timing could not be more fitting. Published today, the profile of Shotwell arrives at a moment when the company she has quietly run for more than two decades stands at the center of the most consequential developments in aerospace, artificial intelligence, and the future of human civilization.

Shotwell joined SpaceX in 2002 as its seventh employee and has never stopped expanding her role. She oversees day-to-day operations across multiple executive teams spanning Falcon, Starlink, Starship, and now xAI following SpaceX’s February 2026 merger with Elon Musk’s artificial intelligence company, a deal that made SpaceX the world’s most valuable private company at a reported valuation of $1.25 trillion. A highly anticipated IPO is expected in the second quarter of 2026.

Will Tesla join the fold? Predicting a triple merger with SpaceX and xAI

Her track record is historic. She oversaw the first landing of an orbital rocket’s first stage, the first reuse and re-landing of an orbital booster, and the first private crewed launch to Earth orbit in May 2020. She built the Falcon launch manifest from nothing to more than 170 contracted missions representing over $20 billion in business. Under her operational leadership, SpaceX completed 96 successful missions in 2023 alone and has now flown more than 20 crewed Falcon 9 missions. Starlink, which she championed as a financial pillar of the company long before it was a mainstream topic, now connects tens of millions of users worldwide and provided a critical communications lifeline to Ukraine following the 2022 invasion.

Elon Musk has never been shy about what Shotwell means to him and to SpaceX. When she shared her vision for worldwide internet connectivity through Starlink, Musk responded on X with a simple statement, “Gwynne is awesome.” It is a sentiment that has been echoed across the industry. NASA Administrator Bill Nelson once said of Musk: “One of the most important decisions he made, as a matter of fact, is he picked a president named Gwynne Shotwell. She runs SpaceX. She is excellent.”

Gwynne is awesome https://t.co/tiXtMWJmPE

— Elon Musk (@elonmusk) September 28, 2024

Now, with Starship targeting its first crewed lunar landing under the Artemis program by 2028, an xAI integration underway, and a pending IPO that could reshape capital markets, Shotwell’s mandate has never been larger. She told Time that 18 Starships are already in various stages of construction at Starbase. “By 2028,” she said, gesturing across the factory floor, “these should be long gone. They better have flown by then.” If Shotwell’s history at SpaceX is any guide, they will.

Elon Musk

SpaceX’s IPO might arrive sooner than you think

Musk has hinted for years that an eventual public offering was inevitable, though he has stressed the need to maintain operational focus. Insiders have told outlets that the CEO is pushing for a significant retail investor allocation, reportedly more than 20 percent of shares, and tighter lock-up periods to limit early selling pressure.

Elon Musk’s SpaceX is on the verge of one of the most anticipated Initial Public Offerings (IPO) in history.

However, a new report from The Information indicates the rocket and satellite giant is aiming to file its IPO prospectus with U.S. regulators as soon as this week, or early next week at the latest.

People familiar with the plans told The Information that advisers involved in the process expect the IPO could raise more than 75 billion dollars, potentially making it the largest stock market debut ever and eclipsing Saudi Aramco’s 29.4 billion dollar offering in 2019.

The filing would mark the formal start of what has long been rumored: SpaceX’s transition from a closely held private powerhouse to a publicly traded company.

The timing aligns with earlier signals.

In late February, Bloomberg reported that SpaceX was targeting a confidential IPO filing in March and a possible public listing in June, with a valuation north of 1.75 trillion dollars. At the time, the company’s private valuation hovered around 1.25 trillion dollars.

SpaceX considering confidential IPO filing this March: report

Starlink, SpaceX’s satellite internet constellation, has been the primary driver of that surge, now serving millions of customers worldwide and generating steady revenue. Recent Starship test flights and a record pace of Falcon launches have further bolstered investor confidence.

Musk has hinted for years that an eventual public offering was inevitable, though he has stressed the need to maintain operational focus. Insiders have told outlets that the CEO is pushing for a significant retail investor allocation, reportedly more than 20 percent of shares, and tighter lock-up periods to limit early selling pressure.

A June listing would give SpaceX immediate access to public capital markets at a moment when demand for space-related stocks remains high. It would also allow early employees and long-time investors to cash out portions of their stakes while giving everyday shareholders a chance to own a piece of the company behind reusable rockets, global broadband, and NASA contracts.

Of course, nothing is certain until the SEC filing appears. Market conditions, regulatory reviews, and Musk’s own schedule could still shift timelines.

Yet the latest word from The Information suggests the window has opened. If the filing lands this week, SpaceX’s roadshow could begin in earnest within weeks, setting the stage for what many analysts already call the IPO of the decade.

Investor's Corner

Tesla gets tip of the hat from major Wall Street firm on self-driving prowess

“Tesla is at the forefront of autonomous driving, supported by a camera-only approach that is technically harder but much cheaper than the multi-sensor systems widely used in the industry. This strategy should allow Tesla to scale more profitably compared to Robotaxi competitors, helped by a growing data engine from its existing fleet,” BoA wrote.

Tesla received a tip of the hat from major Wall Street firm Bank of America on Wednesday, as it reinitiated coverage on Tesla shares with a bullish stance that comes with a ‘Buy’ rating and a $460 price target.

In a new note that marks a sharp reversal from its neutral position earlier in 2025, the bank declared Tesla’s Full Self-Driving (FSD) technology the “leading consumer autonomy solution.”

Analysts highlighted Tesla’s camera-only architecture, known as Tesla Vision, as a strategic masterstroke. While technically more challenging than the multi-sensor setups favored by rivals, the vision-based approach is dramatically cheaper to produce and maintain.

This cost edge, combined with Tesla’s rapidly expanding real-world data engine, positions the company to scale robotaxis far more profitably than competitors, BofA argues in the new note:

“Tesla is at the forefront of autonomous driving, supported by a camera-only approach that is technically harder but much cheaper than the multi-sensor systems widely used in the industry. This strategy should allow Tesla to scale more profitably compared to Robotaxi competitors, helped by a growing data engine from its existing fleet.”

The bank now attributes roughly 52% of Tesla’s total valuation to its Robotaxi ambitions. It also flagged meaningful upside from the Optimus humanoid robot program and the fast-growing energy storage business, suggesting the auto segment’s recent headwinds, including expired incentives, are being eclipsed by these higher-margin opportunities.

Tesla’s own data underscores exactly why Wall Street is waking up to FSD’s potential. According to Tesla’s official safety reporting page, the FSD Supervised fleet has now surpassed 8.4 billion cumulative miles driven.

Tesla FSD (Supervised) fleet passes 8.4 billion cumulative miles

That total ballooned from just 6 million miles in 2021 to 80 million in 2022, 670 million in 2023, 2.25 billion in 2024, and a staggering 4.25 billion in 2025 alone. In the first 50 days of 2026, owners added another 1 billion miles — averaging more than 20 million miles per day.

This avalanche of real-world, camera-captured footage, much of it on complex city streets, gives Tesla an unmatched training dataset. Every mile feeds its neural networks, accelerating improvement cycles that lidar-dependent rivals simply cannot match at scale.

Tesla owners themselves will tell you the suite gets better with every release, bringing new features and improvements to its self-driving project.

The $460 target implies roughly 15 percent upside from recent trading levels around $400. While regulatory and safety hurdles remain, BofA’s endorsement signals growing institutional conviction that Tesla’s data advantage is not hype; it’s a tangible moat already delivering billions of miles of proof.

Tesla lands on Fortune’s 2026 Most Innovative Companies and the Cybercab is why

Tesla ‘Killer’ heads to the graveyard as AFEELA taps out

TIME honors SpaceX’s Gwynne Shotwell: From employee No. 7 to world’s most valuable company

Elon Musk says Tesla is developing a new vehicle: ‘Way cooler than a minivan’

What is Digital Optimus? The new Tesla and xAI project explained