News

Tesla gets generous price target projection from ARK without several crucial factors

Tesla got a new, generous price target projection from analyst Cathie Wood and her firm ARK Invest, even though it left out several massive factors.

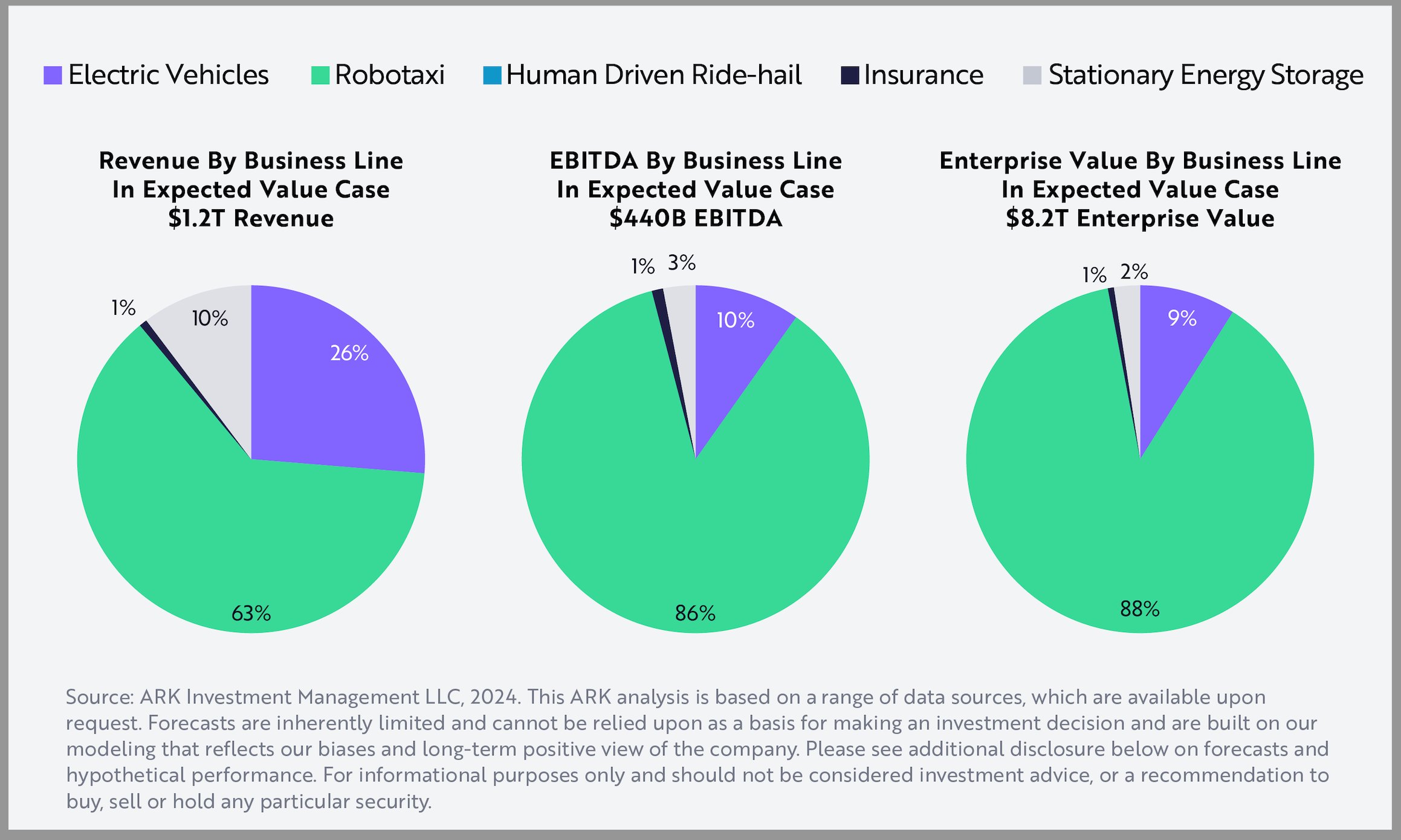

According to ARK’s latest Tesla projection report, which was released on Wednesday, the firm expects the company’s value to swell to $2,600 per share, with a bull case of potentially $3,100 and a bear case of $2,000.

“ARK estimates that nearly 90% of Tesla’s enterprise value and earnings will be attributed to the robotaxi business in 2029, as shown below. Meanwhile, electric vehicles could approximate a quarter of total sales and ~10% of Tesla’s earnings potential, as we believe the robotaxi business will have much higher margins. The charts below break down attributable revenue, EBITDA, and enterprise value by business line,” its analysis breakdown said.

It is important to note ARK Invest has been particularly bullish on Tesla and its business model for some time. However, it was sure to note that in its latest projections, it did not factor in robotics, as Tesla continues to develop its Optimus Bot and recently stated it has been using it in Gigafactory Texas.

We conservatively assumed that Tesla does not sell Optimus externally in our model, and that Optimus manufacturing savings modestly impact Tesla’s costs in single digit percentages over the next five years.

— Tasha Keeney (@TashaARK) June 12, 2024

ARK broadened this idea in its report:

“We assume that Optimus will have minimal impact on our price target. Over the next decade, we expect Tesla to become a leading manufacturer and service provider of robots that move through physical space, as it will have the opportunity to leverage learnings from robotaxis as well as its in-house inference chips, training compute, and manufacturing scale. Tesla expects Optimus to be completing useful factory tasks by year end. Assuming that it were able to subsume 10-20% of Tesla’s labor hours worked with productivity equal to or twice that of its human counterparts, Optimus could save Tesla $3-4 billion, or 1-2% in manufacturing costs, in 2029.”

In fact, the largest single factor in its analysis is that of the Robotaxi, which accounts for the vast majority of the breakdowns ARK illustrated for Revenue, EBITDA, and Enterprise Value:

There are several things ARK left out of its analysts, and a few of them are arguably groundbreaking and could potentially have a major impact on Tesla’s business in the future:

- Tesla Semi – ARK does not believe the Tesla Semi will “contribute significantly” to the company’s value within the five-year investment time horizon

- Supercharging Network – Tesla Superchargers are “unlikely to generate significant revenue,” although they are essential for EVs

- FSD Licensing – Non-Tesla FSD vehicles are unlikely to debut within the five-year timeframe

- AI-As-A-Service – AI-inference-as-a-service and Dojo training-as-a-service is “probably” outside the five-year timeframe

You can read ARK’s full report here.

I’d love to hear from you! If you have any comments, concerns, or questions, please email me at joey@teslarati.com. You can also reach me on Twitter @KlenderJoey, or if you have news tips, you can email us at tips@teslarati.com.

News

These Tesla, X, and xAI engineers were just poached by OpenAI

The news is the latest in an ongoing feud between Elon Musk and the Sam Altman-run firm OpenAI.

OpenAI, the xAI competitor for which Elon Musk previously served as a boardmember and helped to co-found, has reportedly poached high-level engineers from Tesla, along with others from xAI, X, and still others.

On Tuesday, Wired reported that OpenAI hired four high-level engineers from Tesla, xAI, and X, as seen in an internal Slack message sent by co-founder Greg Brockman. The engineers include Tesla Vice President of Software Engineering David Lau, X and xAI’s head of infrastructure engineering Uday Ruddarraju, and fellow xAI infrastructure engineer Mike Dalton. The hiring spree also included Angela Fan, an AI researcher from Meta.

“We’re excited to welcome these new members to our scaling team,” said Hannah Wong, an OpenAI spokesperson. “Our approach is to continue building and bringing together world-class infrastructure, research, and product teams to accelerate our mission and deliver the benefits of AI to hundreds of millions of people.”

Lau has been in his position as Tesla’s VP of Software Engineering since 2017, after previously working for the company’s firmware, platforms, and system integration divisions.

“It has become incredibly clear to me that accelerating progress towards safe, well-aligned artificial general intelligence is the most rewarding mission I could imagine for the next chapter of my career,” Lau said in a statement to Wired.

🚨Optimistic projections point to xAI possibly attaining profitability by 2027, according to Bloomberg's sources.

If accurate, this would be quite a feat for xAI. OpenAI, its biggest rival, is still looking at 2029 as the year it could become cash flow positive.💰 https://t.co/pE5Z9daez8

— TESLARATI (@Teslarati) June 18, 2025

READ MORE ON OPENAI: Elon Musk’s OpenAI lawsuit clears hurdle as trial looms

At xAI, Ruddarraju and Dalton both played a large role in developing the Colossus supercomputer, which is comprised of over 200,000 GPUs. One of the major ongoing projects at OpenAI is the company’s Stargate program,

“Infrastructure is where research meets reality, and OpenAI has already demonstrated this successfully,” Ruddarraju told Wired in another statement. “Stargate, in particular, is an infrastructure moonshot that perfectly matches the ambitious, systems-level challenges I love taking on.”

Elon Musk is currently in the process of suing OpenAI for shifting toward a for-profit model, as well as for accepting an investment of billions of dollars from Microsoft. OpenAI retaliated with a counterlawsuit, in which it alleges that Musk is interfering with the company’s business and engaging in unfair competition practices.

Elon Musk confirms Grok 4 launch on July 9 with livestream event

News

SpaceX share sale expected to back $400 billion valuation

The new SpaceX valuation would represent yet another record-high as far as privately-held companies in the U.S. go.

A new report this week suggests that Elon Musk-led rocket company SpaceX is considering an insider share sale that would value the company at $400 billion.

SpaceX is set to launch a primary fundraising round and sell a small number of new shares to investors, according to the report from Bloomberg, which cited people familiar with the matter who asked to remain anonymous due to the information not yet being public. Additionally, the company would sell shares from employees and early investors in a follow-up round, while the primary round would determine the price for the secondary round.

The valuation would represent the largest in history from a privately-owned company in the U.S., surpassing SpaceX’s previous record of $350 billion after a share buyback in December. Rivaling company valuations include ByteDance, the parent company of TikTok, as well as OpenAI.

Bloomberg went on to say that a SpaceX representative didn’t respond to a request for comment at the time of publishing. The publication also notes that the details of such a deal could still change, especially depending on interest from the insider sellers and share buyers.

Axiom’s Ax-4 astronauts arriving to the ISS! https://t.co/WQtTODaYfj

— TESLARATI (@Teslarati) June 26, 2025

READ MORE ON SPACEX: SpaceX to decommission Dragon spacecraft in response to Pres. Trump war of words with Elon Musk

SpaceX’s valuation comes from a few different key factors, especially including the continued expansion of the company’s Starlink satellite internet company. According to the report, Starlink accounts for over half of the company’s yearly revenue. Meanwhile, the company produced its 10 millionth Starlink kit last month.

The company also continues to develop its Starship reusable rocket program, despite the company experiencing an explosion of the rocket on the test stand in Texas last month.

The company has also launched payloads for a number of companies and government contracts. In recent weeks, SpaceX launched Axiom’s Ax-4 mission, sending four astronauts to the International Space Station (ISS) for a 14-day stay to work on around 60 scientific experiments. The mission was launched using the SpaceX Falcon 9 rocket and a new Crew Dragon capsule, while the research is expected to span a range of fields including biology, material and physical sciences, and demonstrations of specialized technology.

News

Tesla Giga Texas continues to pile up with Cybercab castings

Tesla sure is gathering a lot of Cybercab components around the Giga Texas complex.

Tesla may be extremely tight-lipped about the new affordable models that it was expected to start producing in the first half of the year, but the company sure is gathering a lot of Cybercab castings around the Giga Texas complex. This is, at least, as per recent images taken of the facility.

Cybercab castings galore

As per longtime drone operator Joe Tegtmeyer, who has been chronicling the developments around the Giga Texas complex for several years now, the electric vehicle maker seems to be gathering hundreds of Cybercab castings around the factory.

Based on observations from industry watchers, the drone operator appears to have captured images of about 180 front and 180 rear Cybercab castings in his recent photos.

Considering the number of castings that were spotted around Giga Texas, it would appear that Tesla may indeed be preparing for the vehicle’s start of trial production sometime later this year. Interestingly enough, large numbers of Cybercab castings have been spotted around the Giga Texas complex in the past few months.

Cybercab production

The Cybercab is expected to be Tesla’s first vehicle that will adopt the company’s “unboxed” process. As per Tesla’s previous update letters, volume production of the Cybercab should start in 2026. So far, prototypes of the Cybercab have been spotted testing around Giga Texas, and expectations are high that the vehicle’s initial trial production should start this year.

With the start of Tesla’s dedicated Robotaxi service around Austin, it might only be a matter of time before the Cybercab starts being tested on public roads as well. When this happens, it would be very difficult to deny the fact that Tesla really does have a safe, working autonomous driving system, and it has the perfect vehicle for it, too.

These Tesla, X, and xAI engineers were just poached by OpenAI

SpaceX share sale expected to back $400 billion valuation

Tesla Giga Texas continues to pile up with Cybercab castings

-

Elon Musk1 week ago

Elon Musk1 week agoTesla investors will be shocked by Jim Cramer’s latest assessment

-

News2 weeks ago

News2 weeks agoTesla Robotaxi’s biggest challenge seems to be this one thing

-

Elon Musk1 day ago

Elon Musk1 day agoElon Musk confirms Grok 4 launch on July 9 with livestream event

-

News2 weeks ago

News2 weeks agoWatch the first true Tesla Robotaxi intervention by safety monitor

-

News5 days ago

News5 days agoTesla Model 3 ranks as the safest new car in Europe for 2025, per Euro NCAP tests

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoA Tesla just delivered itself to a customer autonomously, Elon Musk confirms

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoElon Musk confirms Tesla Optimus V3 already uses Grok voice AI

-

Elon Musk2 weeks ago

Elon Musk2 weeks agoxAI welcomes Memphis pollution results, environmental groups push back